This week did not have one “mega” headline. Instead, it had many moves like trump deal that, together, show a market preparing for its next leg.

Macro and policy set the stage

The Federal Reserve cut rates by 0.25% and said QT ends on December 1. Powell also warned the next cut is not guaranteed. The message is mixed: a nod to easing, but not a green light. Meanwhile, signs of a weaker U.S. job market grew.Amazon plans to lay off 30,000 administrative staff, which adds pressure on the Fed to keep easing.

Politics and trade move from talk to signals

Donald Trump attacked Democrats over the shutdown and said the government lacks authority to pay SNAP benefits during it. He also said tariffs on China will drop (including fentanyl to 10%), hinted at talks on chips and rare metals, and teased a meeting with Xi. If the mood turns into an actual U.S.–China trade deal, global liquidity could improve, which usually helps risk assets, including crypto.

Institutional adoption: from pilots to plumbing

The week was stacked with “TradFi plugs into crypto” stories:

- JPMorgan is building Kinexys Fund Flow to tokenize private investment funds on its own chain. Jamie Dimon even admitted he was wrong about crypto and said it’s “real” and people will use it.

- Visa expanded digital-asset settlement to Ethereum, Solana, Avalanche, Stellar.

- Western Union said Solana is the right network for its needs and started stablecoin remittance tests.

- DBS and Goldman Sachs executed the first bank-to-bank crypto options trade.

- Ondo brought tokenized securities to BNB Chain.

- Circle launched the ARC test network with more than 100 big partners (Visa, BlackRock, HSBC, Anthropic, AWS).

- SoFi plans a crypto trading service this year and a SoFi USD stablecoin in H1 2026.

- Coinbase Prime and Figment expanded institutional custody; $DBR (deBridge) moved onto Coinbase’s listing roadmap.

- Standard Chartered sees US$2T in RWA by 2028, mostly on Ethereum.

This is not hype; it is infrastructure.

Market structure and flows: pressure building

The market is tense. Liquidations topped $820M in 24 hours (about $242M in four hours), mostly on longs. If BTC ~US$112,600 hits, shorts face >$3B in liquidations. We also saw October turn red for the first time since 2018.

On-chain and treasury moves were loud:

- MicroStrategy shifted 22,704 BTC (~$2.45B) across wallets in nine hours, likely custody or strategy prep. Separately, Saylor bought about 390 BTC at ~$111,053 each; holdings now 640,808 BTC at a ~$74,032 average; YTD up 26%.

- Odds rose that MSTR enters the S&P 500, which would pipe Bitcoin exposure into a core U.S. index.

- Bitmine bought 44,036 ETH (~$166M), and also disclosed treasury holdings above 3.3M ETH (> $13B).

- SharpLink ended a month of silence by buying 19,271 ETH (~$78.3M).

- Whales accumulated LINK: 39 fresh wallets pulled 9.94M LINK (~$188M) from Binance after the Oct-10 washout.

- Mt. Gox repayments moved to Oct 2026; reserve shows 34,689 BTC still parked.

ETF datapoints kept rolling. First-day volumes: $BSOL 56M, $HBR 8M, $LTCC 1M. 21Shares filed for a $HYPE ETF tracking Hyperliquid; custodians would be Coinbase Custody and BitGo. On fees, HyperliquidX led all networks in the last 24h, with edgeX second and Tron third.

Is this a bear market? Both sides have data

Bear case: fear is high (e.g., Santiment), some days showed negative ETF flows, BTC dominance rose (risk-off), whales moved coins to exchanges, and the global economy looks slow even after Fed cuts.

Bull case: strong institutional inflows at times, exchange reserves are low, developer and active address metrics are steady, and price holds long-term supports (e.g., above the 200-week). Ending QT is usually a positive early signal. Also, a major U.S.–China deal, if it happens, would lift liquidity.

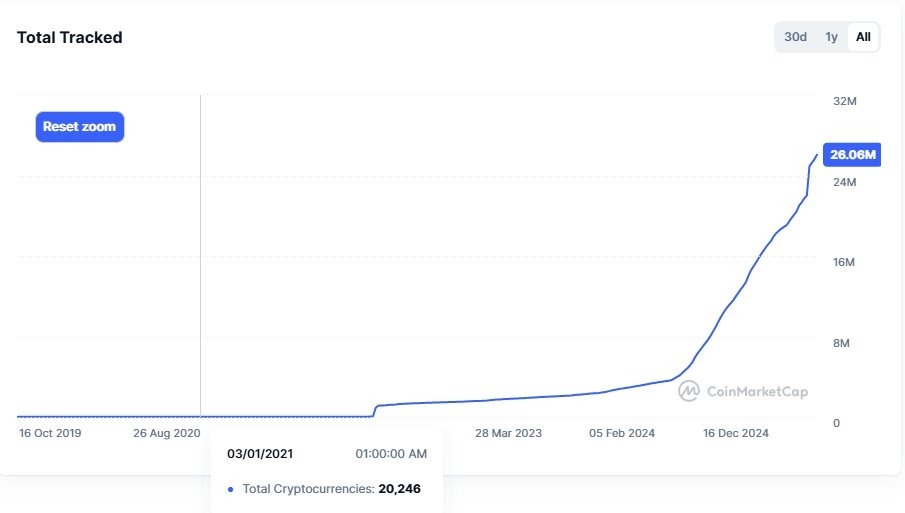

One more hard truth: in 2017 there were a few hundred coins. In 2021, ~20k. In 2025, >26 million. Liquidity grew, but supply of tokens exploded far faster. This cycle looks selective. Institutions will concentrate flows in fewer names. An “altseason” may come, but likely not for every alt.

Privacy returns to the front: Zcash wakes up

Zcash (ZEC) saw a clear privacy demand spike. >5M ZEC (~30% of supply) now sit in shielded pools, and price ran from $50 to $355 after a four-year downtrend break. The drivers are simple: a coming halving, fear of surveillance, and better UX for shielded use. The theme is selective privacy, not chaos, users want financial privacy tools that still fit real life.

Ecosystem: rails, volumes, and experiments

- Sui DEX volume over $1.06B in two days.

- Aptos had $545.7M positive stablecoin flows in 24h.

- OceanPal raised $120M to build a NEAR treasury aiming at up to 10% of total supply.

- Pavel Durov unveiled Cocoon on TON: a private, decentralized AI compute network.

- World Liberty Financial will distribute 8.4M $WLFI to early USD1 users.

- A Hyperliquid theme kept building: the network topped fee charts and got ETF attention.

Governance and controversy

- A proposed Bitcoin soft-fork used language threatening “legal and moral” consequences for dissenters, which set the community on fire. People saw it as a break from Bitcoin’s open culture.

- The FET / Ocean rift escalated with claims about hidden transactions and governance control.

- A Senator plans a bill to ban presidents and elected officials from owning or creating crypto, to avoid conflicts of interest. That will spark a big D.C. debate.

Culture, media, and market mood

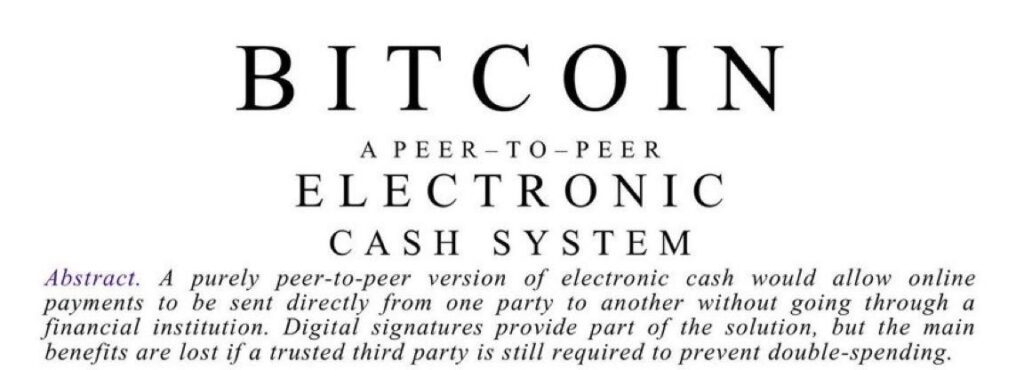

- Bitcoin turned 17 since the 2008 whitepaper. From a short PDF to a global money system, that arc is real.

- Jim Cramer said we should “wait until Monday for a market bounce,” which some took as dark humor; the “Cramer effect” memes rolled.

- SBF’s circle claimed FTX was never insolvent, even when lawyers filed for bankruptcy. This will keep regulators and courts busy.

Perps, liquidations, and network leadership

- Total liquidations surged, with longs hit the most, leverage cuts both ways.

- HyperliquidX led networks by fees, showing heavy demand for on-chain perps. EdgeX and Tron followed.

- A new $HYPE ETF filing by 21Shares pushed that narrative further.

One line on sentiment

The board is set, but not decided. Macro is tilting toward easier policy, yet not fully. Politics point to a possible trade thaw. Institutions are laying real rails. Privacy is back. The market is crowded with tokens, so selection matters more than ever.

What to watch next

- BTC trigger levels (e.g., that short-liquidation wall near $112,600).

- December: the first month post-QT.

- U.S.–China: do tariff cuts and chip talks become a deal?

- Flows: ETF nets, exchange reserves, and whale moves.

- Governance: Bitcoin soft-fork tone, and the FET/Ocean dispute outcome.

This article is informational and not financial advice. For more analysis, visit blog.millionero.com. Trade spot and perpetuals responsibly on Millionero.