Security shocks and the “own your keys” reminder

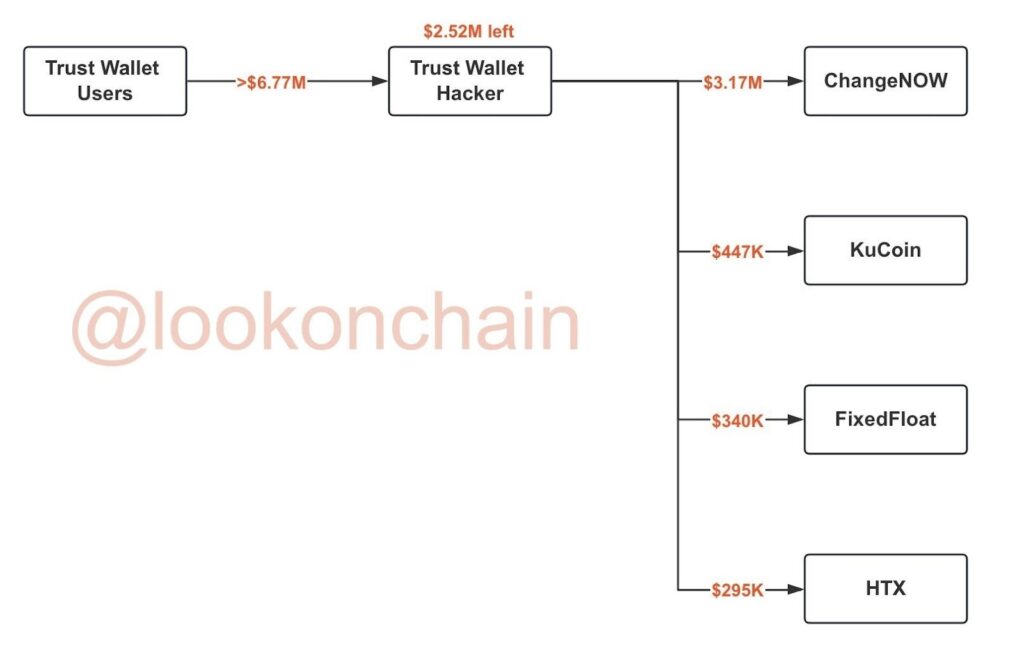

The week’s most direct warning came from Trust Wallet, after reports of a security incident that hit hundreds of users. The stolen amount was said to be over $6.77M so far, with about $4.25M already moved through venues like ChangeNOW, FixedFloat, KuCoin, and HTX. The point people kept repeating was simple: when funds move fast, the damage spreads fast too.

Trust Wallet owner, CZ’s comment mattered here because it changed the tone: he said Trust Wallet will fully compensate affected users. That does not erase the risk, but it does show how big platforms now treat security failures as an existential issue, not just “bad PR.” Alongside that, there was a practical tip: the hacker wallets were shared for tracking via Arkham / Lookonchain.

A similar theme appeared in a second story: Polymarket confirmed a security breach that affected a limited number of users, caused by a third-party authentication issue that allowed bypassing 2FA. The fix is done, but the lesson is uncomfortable: even if your security habits are good, your exposure can still depend on tools you don’t control.

Macro mood: “don’t fight liquidity” is back on the table

A lot of the week’s messaging was basically one argument told from different angles: liquidity and momentum are leaning risk-on, and fighting that trend has historically been painful.

People pointed to:

- U.S. GDP growth at the strongest pace since 2023,

- CPI surprising to the downside at 2.7%,

- talk that Trump is moving toward appointing a new Fed chair with a rate-cut leaning stance,

- oil at its lowest levels since 2021,

- 2025 equity funds pulling in $1.4T (a record),

- and Magnificent 7 AI investment said to be above $600B per year.

Whether you agree with the conclusion or not, the logic is clear: if inflation cools while growth holds, markets start to price in easier conditions later, and money tends to move earlier than headlines.

There was also a global liquidity note: Reuters was cited saying the Reserve Bank of India plans to inject $32B into the banking system. In the same breath, the U.S. was described as having ended QT, with markets thinking about possible rate cuts in 2026. Put together, the claim was simple: the “money printers” may be warming up again, slowly.

And then came the data-dependent pushback: Hammack (Fed) was quoted saying rates may stay unchanged “for some time,” which fits the idea that the Fed will want more proof before easing.

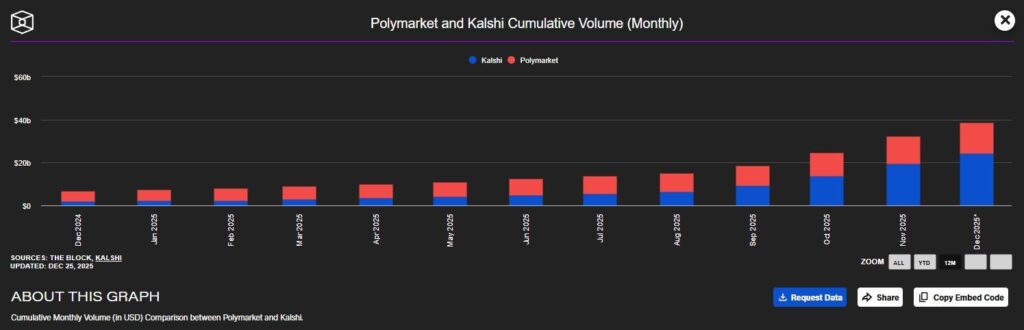

Prediction markets are growing into a real signal

One of the more interesting macro threads wasn’t a chart of CPI or GDP. It was about prediction markets.

The claim: cumulative volume of $14.12T, rising participation across Kalshi and Polymarket, and forecast error 40% lower than “consensus,” rising to 67% outperformance during high volatility. The key point wasn’t “they’re always right.” It was: when size and liquidity grow, markets can absorb information faster, with less noise. In that world, money becomes a kind of real-time poll.

That same Kalshi lens showed up elsewhere too: traders were pricing an 88% chance of no rate cut in January 2026, which is basically the market saying, “don’t rush the easing story.”

Bitcoin and crypto: price stable, but the plumbing is changing

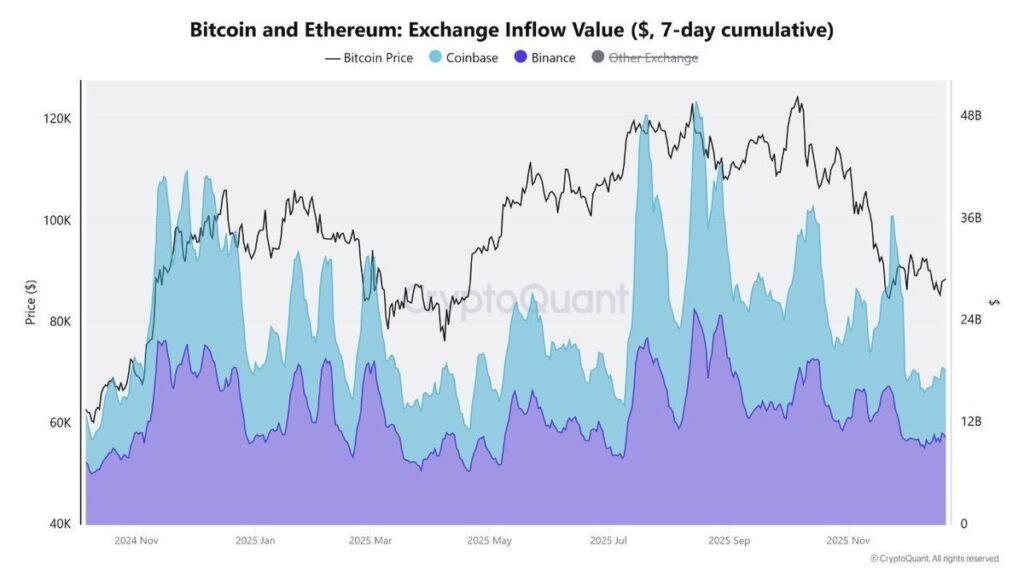

Bitcoin spending the week around $88K looked calm on the surface. Under the surface, the conversation was about flows and participation.

There is a shift: a month ago, some exchanges saw very large BTC/ETH inflows, with one alone said to have logged $21B in 7 days, often a sign of repositioning and possible sell pressure. Now, price is still near the same zone, but now inflows on those exchanges are down 60%.

The interpretation was important: if price is stable while liquidity and short-term trading shrink, it can look less like distribution and more like absorption.

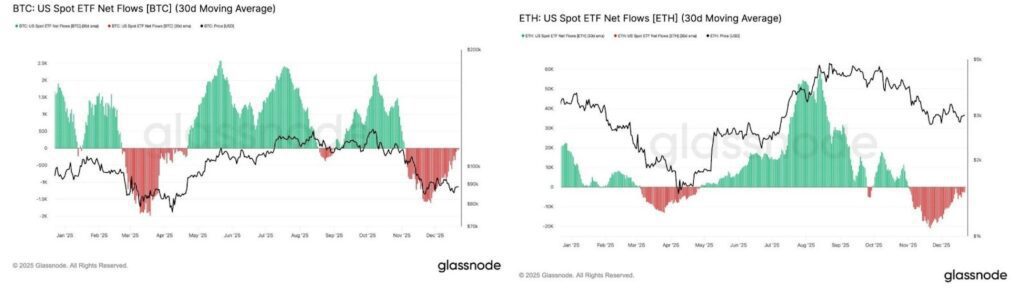

That view clashed with another institutional-demand signal: Glassnode data was cited saying BTC and ETH ETF flows have been negative since early November, implying weaker institutional participation and thinner liquidity in crypto markets. The market can hold steady even when big demand softens, but it becomes more sensitive and more “jumpy” when liquidity is thinner

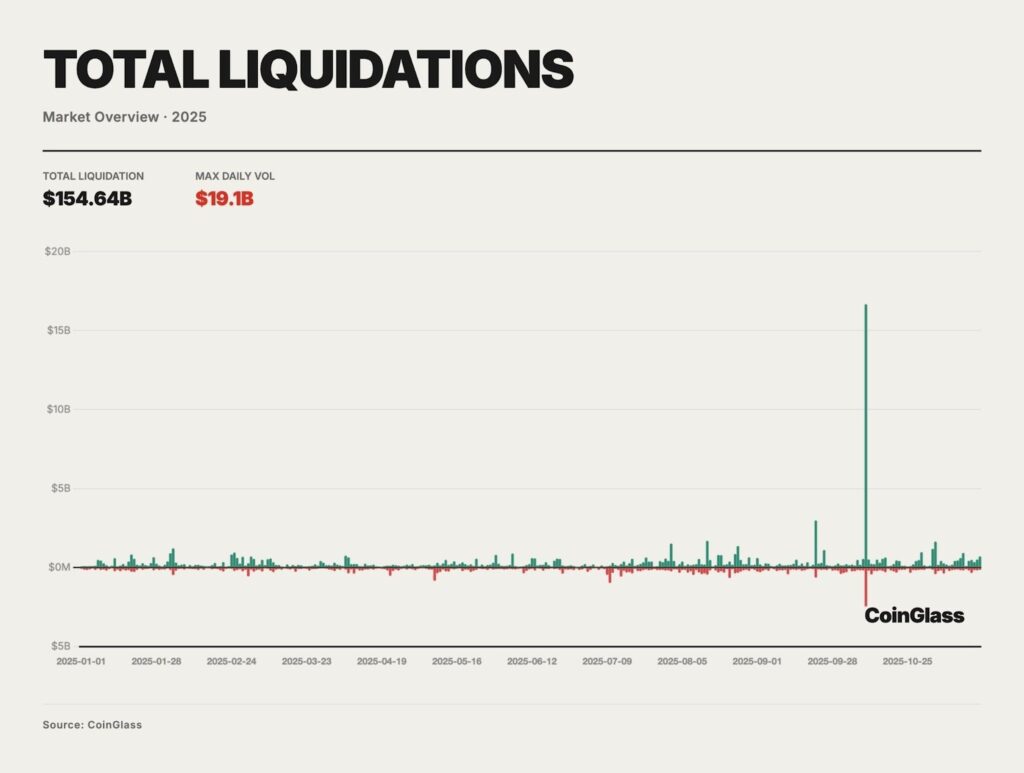

Another stat added emotional weight: around $150B in leveraged positions were said to have been liquidated since the start of the year (via Coinglass). That number matters less as a precise total and more as a reminder: leverage is still the fastest way to get wiped out in a market that doesn’t warn you.

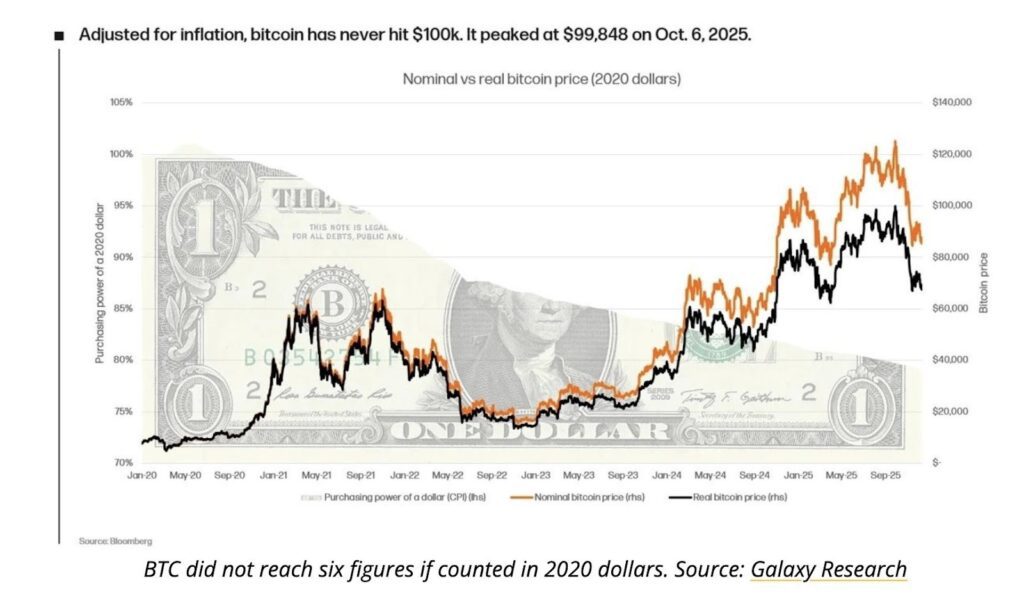

And then there was a clean “cycle debate” datapoint: Galaxy Research argued that inflation-adjusted Bitcoin never truly hit $125K, peaking at $99,848 in 2020 dollars. It’s a nerdy point, but it hits a real psychological level: nominal milestones and real purchasing-power milestones are not the same thing.

Institutional rails: ETFs booming, and crypto ETFs still pushing forward

Even in a week full of crypto-specific talk, a lot of the “big money” story was still about ETFs.

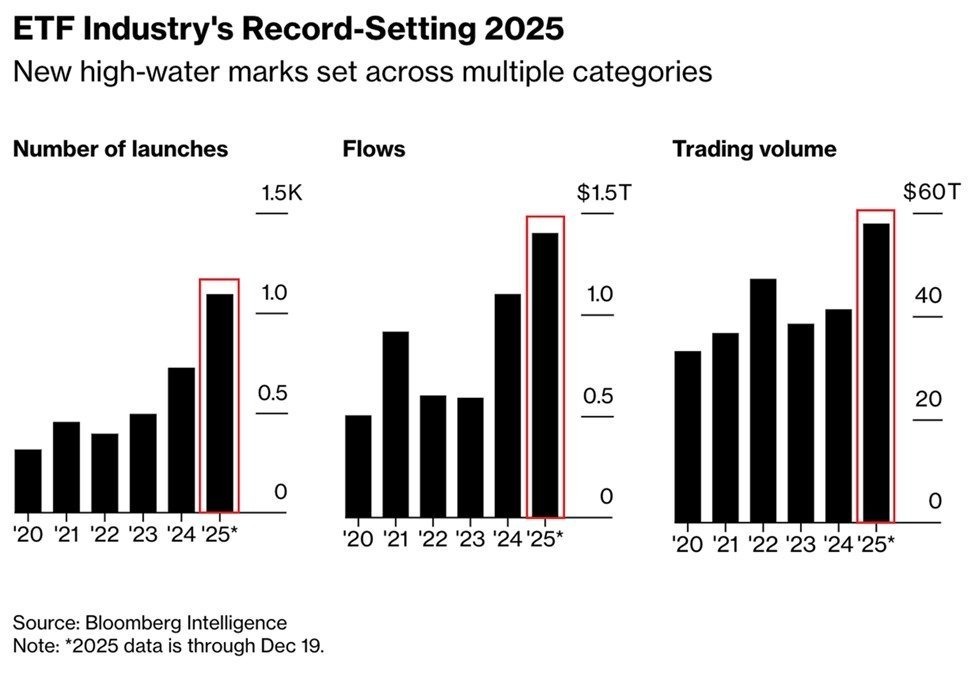

2025 was a historic U.S. ETF year:

- $1.4T net inflows (record),

- about $300B above the old annual record,

- 57.9T in trading volume,

- 1,100 ETF launches (+123% vs 2023),

- and a reminder that the last time so many indicators broke records in one year was 2021.

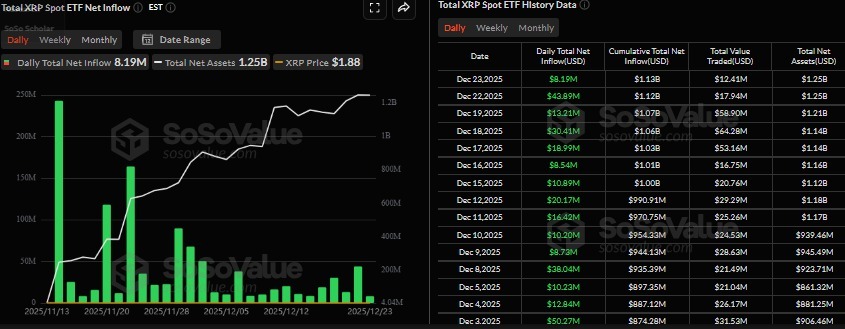

In the crypto corner of that ETF universe, XRP ETFs were said to have posted $8.19M inflows in the latest session, lifting total AUM to $1.25B. The numbers aren’t massive compared with mega funds, but they show a consistent pattern: once ETFs exist, capital uses them because they are simple to access and easy to manage.

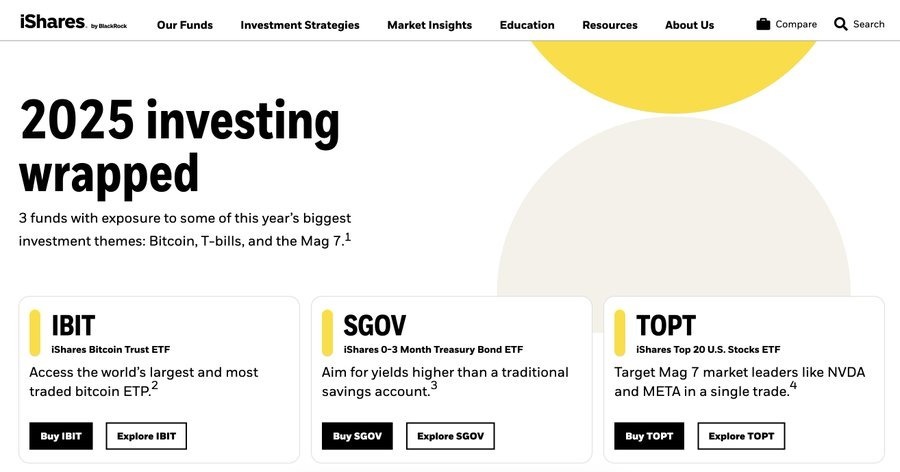

This also matches another repeated story from earlier in the week: BlackRock reportedly listed Bitcoin among its biggest investment themes for 2025, alongside U.S. T-bills and Mag 7 stocks. That exact note was shared twice in the feed, same wording, same idea, almost like people wanted to underline it: Bitcoin is being discussed in the same room as mainstream allocations now, not only as a niche bet.

Supply games: burns, buybacks, and governance as a value driver

Token supply management kept showing up as a “serious” narrative this week, less memes, more governance.

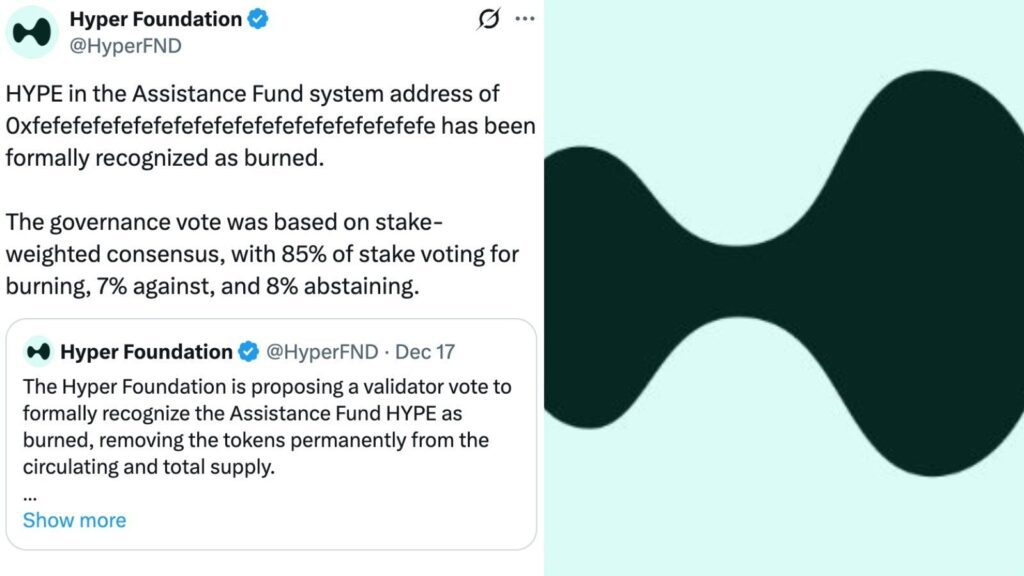

A major headline here: Hyper Foundation said the $HYPE tokens in the system support fund address (0xFEFE…FEFE) are officially recognized as burned. That is a permanent supply reduction, and it turns a technical action into a formal governance reality.

Separately, a broader supply-management roundup (via Tokenomist) listed:

- $UNI DAO vote to activate protocol fees and burn UNI, plus a retroactive burn of 100M UNI from the treasury, and a plan tying ecosystem growth under Uniswap Labs with a 20M UNI/year budget; vote ending Dec 25

- $HYPE vote on a burn proposal sized at $1B (ending Dec 24) and a scheduled unlock on Dec 29 equal to 2.59% of circulating supply (about $250M) from team allocation

- $ASTER emissions reduction starting Dec 22, phase 5 buyback program, and up to 80% of daily platform fees used to buy ASTER on-chain

- $DEGEN for one week: treasury matching burn rate for each user tip, pushing short-term supply reduction

The big picture here is not “burns pump price.” It’s that markets are watching whether governance can create credible, enforceable monetary policy inside protocols.

Regulation, politics, and the slow march toward clearer rules

Regulatory talk this week wasn’t abstract. It was specific and time-bound.

- SEC Chair Paul Atkins was quoted saying crypto market structure legislation and the CLARITY act (passed by the House) are moving toward Congress soon.

- Bank of Russia was reported to propose opening crypto access to non-qualified individuals, but under strict constraints, cautious, but still a meaningful shift.

- In the U.S. tech supply chain, there was an announcement that tariffs on Chinese semiconductors will stay at 0% until June 2027, which people framed as supportive for near-term tech conditions.

- And in Washington messaging: Hassett (White House economic advisor) said the Fed is too late to cut; Bessent (Treasury) floated reviewing the 2% inflation target into a wider band like 1.5%–2.5% or even 1%–3%. That’s a big signal: the debate is no longer just “when do we cut,” but “what rules are we even aiming for?”

Meanwhile, there was also a policy push from the industry side: 125+ crypto companies and the Blockchain Association asked the U.S. Senate Banking Committee to stop efforts to expand restrictions on stablecoin rewards to third-party platforms. It’s a reminder that stablecoins are no longer a side topic, they are now a core fight.

TradFi and DeFi are blending faster than people admit

A few stories this week made the same point in different ways: the wall between TradFi and DeFi is thinning.

- Brett Harrison (former FTX US president) raised $35M for a new perpetuals platform aimed at traditional assets like stocks. Same crypto tech, different target market.

- HashKey Capital raised $250M in a first close for a blockchain-focused multi-strategy fund (target $500M), with focus on infrastructure and real-world use cases.

- Circle said EURC circulating supply reached €300M, framing it as demand for MiCA-compliant, fully backed stablecoins usable globally.

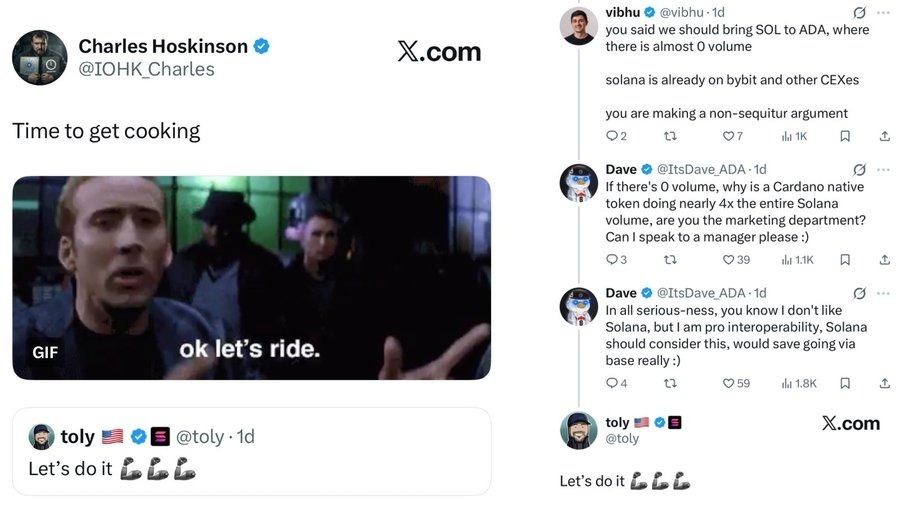

- There was also a cross-chain “maybe”: Charles Hoskinson and Anatoly Yakovenko expressed interest in building a bridge between ADA and SOL.

And one painful cautionary tale sat next to all this progress: the Axelar story. The claim was that Circle acquired the Axelar team and IP to build AI Agents infrastructure, while $AXL holders were left with only a maintenance team and no compensation. The token was said to be down 49% from a December high near $0.083. The message was harsh but important: if token value isn’t truly linked to the value being built, token holders can end up as the weakest party.

Sentiment indicators: from miner capitulation to the “Cramer signal”

A few “market psychology” notes rounded out the week:

- VanEck said a roughly 4% drop in hash rate into mid-December can be a classic contrarian buy signal, often linked with miner capitulation and later recovery windows over 90–180 days.

- Roughly 350,000 BTC was sold at a loss, framed as capitulation and a possible reset phase.

- Ki Young Ju (CryptoQuant) warned that Bitcoin network capital inflows may be slowing after ~2.5 years of growth, and that sentiment recovery could take months, more “cooldown” than “end.”

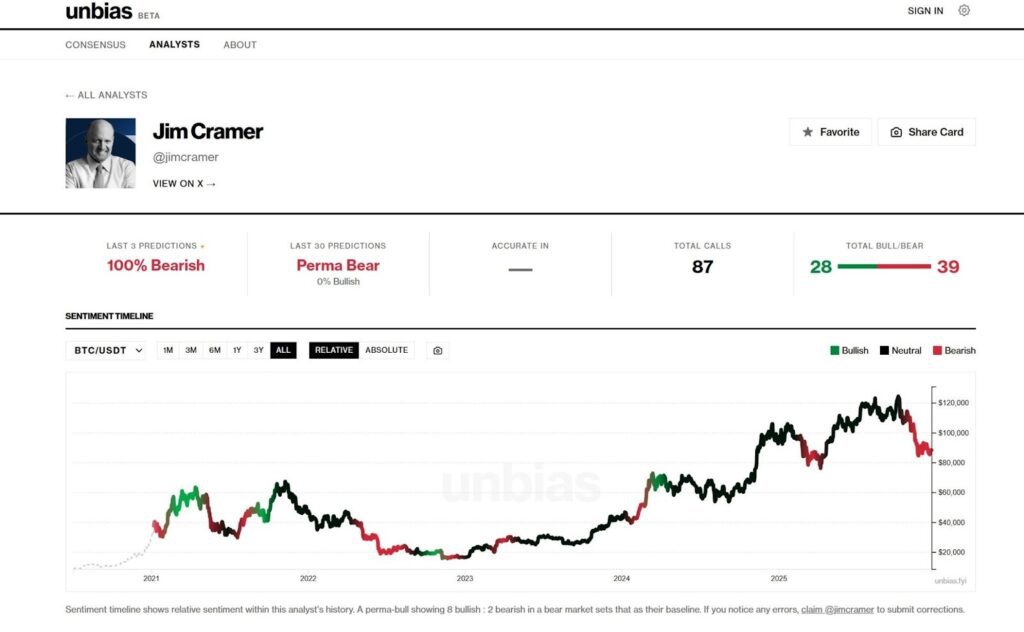

- Jim Cramer reportedly turned 100% bearish on BTC, which people treat as a meme-like contrarian signal.

- Evgeny Gaevoy (Wintermute) delivered a blunt message: people in crypto barely past 30 claiming they “left crypto” are often just giving up early; the path is long and real opportunities rarely show up at the start.

Finally, here are two “year snapshot” that frames context:

A performance table showing many assets up strongly (including gold +68%, silver +140%, etc.) while Bitcoin +10.44% was behind the pack, raising the question: is it lagging, or is the cycle different?

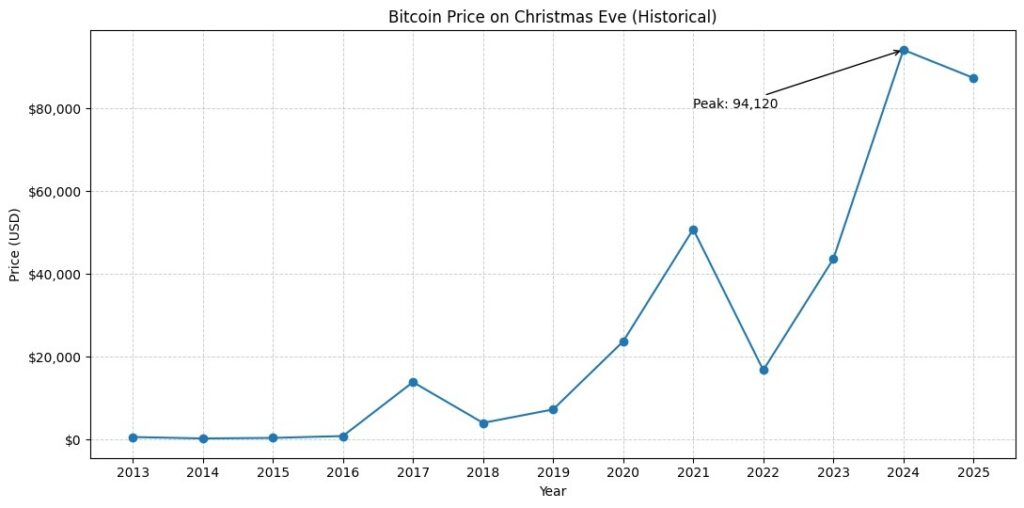

And a simple Christmas Eve Bitcoin history list from 2013 to 2025, ending with 2025: $87,340, a reminder that Bitcoin’s “holiday price” has basically become its own tradition.

This article is shared for general information only. It is not financial advice, and it should not be taken as a recommendation to buy, sell, or hold any asset. Crypto markets are risky and can move fast.

Always do your own research and double-check information from primary sources. For more educational reads and market explainers, visit blog.millionero.com.

And when you feel ready, you can explore Spot and Futures markets on Millionero.