Markets spent the weekend trying to price something that looks geopolitical, but behaves like an energy-and-liquidity story: the US military operation in Venezuela and the capture of Nicolás Maduro and his wife, followed by statements from US President Trump about the US “running” Venezuela for a period and pushing to “get the oil flowing.”

That is why the social feeds kept repeating the same framing: Venezuela is not only politics, it is a balance sheet of hard assets (oil, gas, metals, freshwater, and “strategic minerals”), and whoever controls the direction of that supply can move energy, risk sentiment, and the “what does the US want?” narrative at the same time. The “Venezuela as a strategic US asset” line is basically this idea in one sentence.

The other piece that came through clearly: this weekend didn’t stay inside Venezuela. China publicly pushed back, warning against countries acting like a “world judge,” and called the seizure a violation of sovereignty. That matters because Venezuela’s oil flows in recent years leaned heavily toward China, and a forced re-routing would not just be about barrels, it would be about influence.

Risk-on crypto… at the same time as war headlines?

One of the most interesting “weekend tells” was that risky assets didn’t automatically collapse. After the Venzuela situation, crypto became deep green across the board, with a +$90B jump in total crypto market cap in 24 hours, and the idea is that US markets could open green.

In crypto itself, the price action was framed as a classic liquidation-driven squeeze: Bitcoin ripping toward $93,000 while roughly $75 million of leveraged shorts got wiped out in about an hour, and BTC jumping about $5,000 from the Friday-night low that formed soon after the Venezuela strikes began.

That kind of move often feels “too fast” because it’s not only spot buying, it’s forced buying from traders getting liquidated, plus hedges flipping.

The “energy paradox”: why oil and gas fell instead of spiking

Normally, escalation involving an oil producer pushes crude and gas up on fear of disruption. But the opposite happened: natural gas quickly came down around 6% after futures opened, and oil slipped back below ~$57, because traders saw the Venezuela event as supply-additive (more future supply) rather than supply-destructive (less near-term supply).

That core logic matches what analysts were telling mainstream outlets: if Venezuela transitions in a way that ultimately raises production over time, it can weigh on longer-dated oil prices, even if the short-term is noisy. And on trade flows, a faster change could be where the oil goes: a re-route away from China and back toward US Gulf Coast refineries that are built to handle heavier crude grades.

This is also where the “Chevron up big in overnight trading” claim fits emotionally: the market instinct is to ask, “Who wins if Venezuela oil is ‘back in play’ under US influence?” Even when the exact % move is debated in real time, the directional idea is clear: US-linked operators and refiners are the obvious first suspects.

Safe-haven didn’t disappear: it just showed up in metals

While crypto looked risk-on, the weekend also produced a classic safe-haven response: gold and silver surged. Silver moving above ~$75/oz (up roughly 4%) was not just a random spike, it was part of a broader “metals were already hot” tape coming out of 2025, then getting a geopolitical catalyst.

There also is a very “2026” behavioral signal: a whale selling ETH after a large loss (about $18.8M over two weeks) and rotating into tokenized gold (XAUT), buying 3,299 XAUT around a ~$4,421 average, tracked via Arkham. That’s basically a clean story of risk fatigue: even big players sometimes decide they want something that behaves more like a hedge.

Crypto internals: whales, protocol economics, and a reminder on security

A few crypto-native signals this weekend were worth noting because they’re not price charts, they’re positioning:

- Solana whale accumulation as a trend: Santiment-based behavior indicators hitting ~70%, which was presented as “big wallets are buying” and potentially an early confidence/turn signal.

- Anatoly Yakovenko’s protocol-profit idea: Solana co-founder shared a proposal that reads like a “DeFi meets corporate finance” model, storing protocol profits as future-claimable protocol assets, offering a one-year lock option, and paying yield in a token as a reward for long-term commitment, discussed in the Solana/Jupiter orbit.

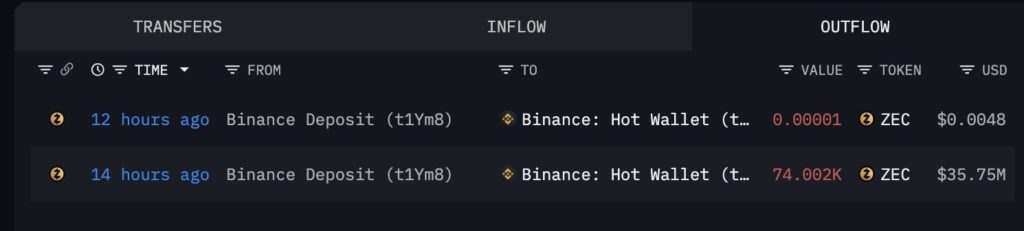

- ZEC whale move: 74,002 ZEC (about $35.75M in the post) deposited to exchanges, the kind of transfer people watch because it can precede selling, collateral usage, or internal reshuffling.

On the security side, there was also a “good news / bad news” pair: phishing losses allegedly fell ~83% across 2025, but wallet drainers stayed active, and one malicious permit signature reportedly cost a user ~$1.08M (aEthLBTC).

Fewer people may be falling for basic phishing, but signature traps and approvals are still doing real damage.

TradFi keeps moving onto-chain: JPMorgan + BlackRock’s messaging

Two institutional updates pointed in the same direction:

- JPMorgan tokenized money market fund on Ethereum: framed as a major bank pushing tokenization on a public chain, reinforcing the “tokenization is becoming infrastructure” narrative.

- Larry Fink / BlackRock tone: tokenization reduces friction and broadens access, is essentially the “why this matters” pitch for RWAs becoming a core layer in future markets.

Even if crypto prices swing, this angle keeps returning: large institutions want faster settlement, programmable ownership, and broader distribution rails.

Politics spreads: Colombia comments and “second strike” language

US President Trump also commented sharply about Colombia and an implied openness to an “operation,” plus separate messaging that the US was prepared for a second Venezuela strike if needed. Those aren’t market micro-details, they shape whether traders treat this as a contained event or the start of a wider regional risk premium.

Coming up this week: US data that can move Fed expectations (and liquidity talk)

A practical setup for the week: a heavy calendar where each print can shift the market’s guess about rate cuts vs. holding steady, and whether the next big liquidity story is loosening (and eventually, if things get extreme, QE-like conditions).

Two key context points first:

- The Fed’s policy rate is currently 3.50%–3.75% (set in December 2025).

- On the balance sheet side, the Fed recently stopped runoff and began Treasury-bill purchases for reserve management, explicitly framed as market-functioning operations rather than “QE.” Still, liquidity-sensitive markets tend to react to the flow even when the Fed says “this is not QE.”

This Week’s Events:

- ISM Manufacturing (Monday): If it weakens, it supports the “growth is cooling” argument and can increase the market’s comfort with future cuts. If it firms up, it can push the “no rush to cut” camp.

- ADP + JOLTS + ISM Services (midweek): Together, these are a labor-demand temperature check. Hot openings/strong hiring can keep the Fed cautious; cooling demand makes cuts easier to justify.

- Weekly Jobless Claims (Thursday): Markets treat this as the fast weekly pulse. A trend higher can quickly revive “Fed will need to support” thinking.

- Jobs Report (Friday): The big one. A weak payroll print tends to pull rate expectations down (more cuts priced), and a strong one tends to push them up (cuts delayed).

- Consumer Confidence / Sentiment (Friday): The widely watched Friday release that week is University of Michigan consumer sentiment; Conference Board consumer confidence is later in the month. Either way, softer confidence + softer jobs tends to push markets toward “easier policy.”

Finally, Truflation-style “real-time inflation” readings below 2% (CPI/core near ~1.93, PCE ~1.85). If markets buy that story and official data also cools, it strengthens the chain reaction: cuts become more plausible, liquidity conditions can loosen, and the loudest bullish narratives start using the word “QE” again, even if the Fed itself would resist that label.

This Week’s Major Token Unlocks

Hyperliquid (HYPE)

Date: January 6, 2025

Unlock Value: 313M USDT

% of Circulating supply: 3.61%

Number of Tokens: 12.46M HYPE

Ethena (ENA)

Date: January 5, 2025

Unlock Value: 42M USDT

% of Circulating supply: 2.37%

Number of Tokens: 171M ENA

Linea (LINEA)

Date: January 10, 2025

Unlock Value: 9.8M USDT

% of Circulating supply: 6.34%

Number of Tokens: 1.38B LINEA

Movement (MOVE)

Date: January 9, 2025

Unlock Value: 6.1M USDT

% of Circulating supply: 5.77%

Number of Tokens: 164M MOVE

Aptos (APT)

Date: January 11, 2025

Unlock Value: 21.6M USDT

% of Circulating supply: 0.7%

Number of Tokens: 11.31M APT

This weekly recap is for general information only and is not financial advice. Always do your own research and manage risk. If you want more market explainers and deep dives, check blog.millionero.com, and trade on Millionero only when you’re ready.