This past week felt like two timelines running at the same time. In one timeline, AI and big tech moved at full speed. In the other, politics, central banks, and crypto markets stayed tense, slow, and cautious.

“Musk Industries” and the new AI hardware stack

The week started with a strong signal from the “Musk empire.”

The idea of “Musk Industries” became real as SpaceX, Tesla and xAI moved closer under one roof in terms of vision and branding.

Rockets, cars, and AI will not be separate stories. They will sit on top of one industrial platform, sharing data, chips, and robotics.

At the same time, there was a strange “AI meme → real world” link. A “clawdbot” idea exploded online and triggered what people jokingly called a “bank run on Mac minis,” as everyone rushed to buy cheap compute. Then Anthropic simply released its own version, turning a social hype moment into a proper product race.

Tesla added even more fuel. The company said it will halt production of Model S and Model X so it can focus on scaling 1 million Optimus humanoid robots this year. That is a radical shift: from selling luxury cars to turning robots into the main product line. Whether they hit 1 million units or not, the signal is that humanoid robots are no longer a side project.

China vs Google: video-to-code and “world models”

On the model side, China dropped a bomb: the Kimi K2.5 model. It can take video and turn it into production-ready apps. In other words, “show, don’t tell” becomes an actual coding interface.

On the same day, Google pushed a new Gemini update that can do the same kind of video-to-app transformation. It looked like a direct reply: “you are not alone in this feature.”

Google did not stop there:

- It launched Genie, described as a leading world model that can understand and simulate environments.

- It switched on Gemini for 3.8 billion Chrome users, quietly putting an AI layer in the default browser for most of the planet.

- It released an alpha genome model that can “one-shot” 1 million DNA base pairs, giving 3,000 researchers across 160 countries a new tool for biology and medicine.

- It also teased a new Veo model, keeping the pipeline full for the coming months.

This is what AI platform lock-in looks like: browser, biology, video, and simulation models all tied into one system.

Big tech earnings, mega-rounds, and the chip race

Microsoft crushed earnings and launched a new AI chip, but the stock still fell around 10% because revenue “only” grew 39%. The market reaction shows how high expectations already are for AI leaders. “Very strong” is now sometimes treated as “not enough.”

On the funding side:

- Anthropic’s new round was reportedly 2x oversubscribed, and the target size rose to 20 billion dollars.

- OpenAI is said to be raising up to 100 billion dollars, at a possible 750 billion valuation.

This is not normal startup funding anymore. These are central-bank-scale balance sheets being built inside private AI labs.

In hardware, Intel was reported to be preparing to help produce Nvidia’s next-gen Feynman GPUs, which would make Intel look like “America’s TSMC” in this cycle. If that happens, U.S. chip production becomes more domestic and less dependent on overseas manufacturing.

On the robotics side, a humanoid robot built by Figure AI washed dishes with zero human interaction. It sounds small, but full, unscripted autonomy on a boring house task is exactly the kind of step that can make robots feel “ready for real life” instead of just demos.

And in consumer hardware, Apple reportedly bought a stealth startup for 2 billion dollars that can lip-read. The plan is to integrate that tech into new AI AirPods with cameras and mics, turning simple earbuds into a full sensing device. At the same time, Demis Hassabis confirmed a Google Glass 2.0-style product coming this summer.

So we now have: robots doing dishes, AirPods that can read lips, and AR glasses coming back. AI is escaping the screen.

Government funding: a deal, a fight, and a “technical” shutdown

In Washington, the week started with a major funding package passing the United States Senate: 71–29, keeping most of the government funded until 30 September 2026.

But funding for the Department of Homeland Security United States Department of Homeland Security was carved out and only extended for two weeks. The reason: a political fight over immigration enforcement, after two U.S. citizens in Minneapolis were killed during federal operations.

Senate Democrats, led by Chuck Schumer, demanded reforms to ICE U.S. Immigration and Customs Enforcement and Border Patrol United States Border Patrol, including:

- mandatory body cameras,

- tighter warrant rules,

- limits on “roving patrols” and masked agents,

- and stronger independent oversight.

Schumer’s line was simple: “No real change, no Democratic votes.”

Because the United States House of Representatives was in recess, it could not vote in time. So at 12:00 a.m. on January 31, the U.S. government entered a technical, partial shutdown. Some agencies paused operations; non-essential staff faced furloughs.

The White House framed it as a procedural issue that should be brief, but the market is now watching two things:

- How long the shutdown lasts, and

- Whether DHS funding will only return together with deep reforms.

Earlier in the week, odds of a shutdown reached record levels on prediction markets, and that fear has now turned into reality, even if the baseline expectation is still “short and limited.”

Trump, the Fed, metals, and the dollar

Monetary policy took another sharp turn. Donald Trump officially chose Kevin Warsh as the next Chair of the Federal Reserve. Before the announcement, prediction markets put his odds as high as 93%, so the choice did not surprise traders, but it still matters.

Warsh is seen as more hawkish on inflation and more friendly to Bitcoin than many other names. When news of his selection spread, gold and silver sold off hard, and the U.S. dollar rallied. Markets quickly unwound “debasement hedges.”

The question now is simple: if metals lose some shine because policy might turn tighter, does part of that capital rotate into Bitcoin instead of just going back to cash?

This comes on top of a strange communication gap:

- Trump said the U.S. dollar is “doing great.”

- Jerome Powell said the gold rally “doesn’t mean much macroeconomically.”

But the raw numbers look different: the dollar index is down about 11% over 12 months, and gold is up over $1,000 per ounce in 28 days. The market hears the data, not just the words.

The FOMC meeting this week held rates steady, as expected. The real focus was on Powell’s tone and press conference. Key signals were:

- Policy is in “wait and see” mode, meeting by meeting.

- The Fed thinks tariff-driven inflation may peak then fade later this year.

- Risks to jobs and inflation have both cooled somewhat.

- The door to future rate cuts is open, but timing is not fixed.

At the same time, Rick Rieder argued that cutting rates mainly helps the housing market (by lowering mortgage costs) and does not necessarily re-ignite inflation. His view lines up with the current administration’s wish for lower rates to ease the housing crisis.

On the other side, Warren Buffett gave a blunt warning: “We don’t want to own anything denominated in a currency that’s going to hell.” He said governments naturally weaken their currencies over time, which is exactly the fear that pushes some investors toward gold, Bitcoin, and other alternatives.

A famous analyst said: if you told someone a year ago that in 2026 we would have a weaker dollar, lower rates, a new Fed chair, rising global liquidity, fiat losing value, and both stocks and metals at record highs, they would probably assume Bitcoin is at $150,000. But it isn’t. Either the market is mispricing Bitcoin, or something more structural has changed in how risk is priced.

Macro, geopolitics, and the “risk plumbing”

The macro picture stayed noisy:

- Trump repeated his demand for much lower rates, even talking about a 1% Fed funds rate as a goal.

- Geopolitically, a U.S. aircraft carrier and a large strike group moved into the Middle East, near Iran, adding a new layer of risk.

Standard Chartered warned that stablecoins could pull up to $500 billion from U.S. bank deposits by 2028, as more people hold digital dollars instead of traditional cash in banks. That is a direct threat to the funding model of many banks.

All of this means the “infrastructure” of the financial system, rates, reserves, and deposits, is shifting at the same time as politics and war risks are rising.

Commodities and safe havens: metals, XAUT, and hash-rate

Commodities reacted strongly to these shifts. Along with the big drop in gold and silver after the Warsh news, the Shanghai Futures Exchange changed trading limits and margin rules for silver, tin, and copper contracts. When an exchange tightens rules, it usually means volatility has already spiked or is about to rise.

Whales also moved into XAUT (a token backed by gold). One large player withdrew 392 XAUT (about $2 million) from Centralized crypto exchanges. That points to more demand for tokenized gold as a digital safe haven.

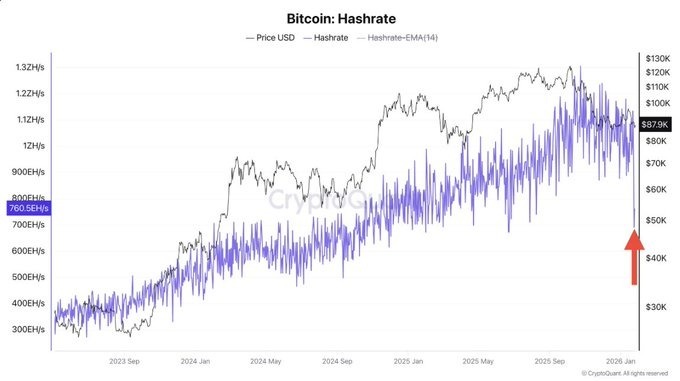

In Bitcoin mining, a major cold wave in the United States led miners to switch off some machines. The hash-rate dropped, which is normally a sign that high energy costs and grid stress are forcing miners to pause. Historically, these drops are temporary; hash-rate tends to bounce back as weather and prices normalize.

So you had metals whipsawing, tokenized gold drawing in whales, and Bitcoin’s physical infrastructure bending under weather and power costs, but not breaking.

Crypto markets: low volume, high liquidations

The actual trading environment for crypto stayed weak and jumpy at the same time.

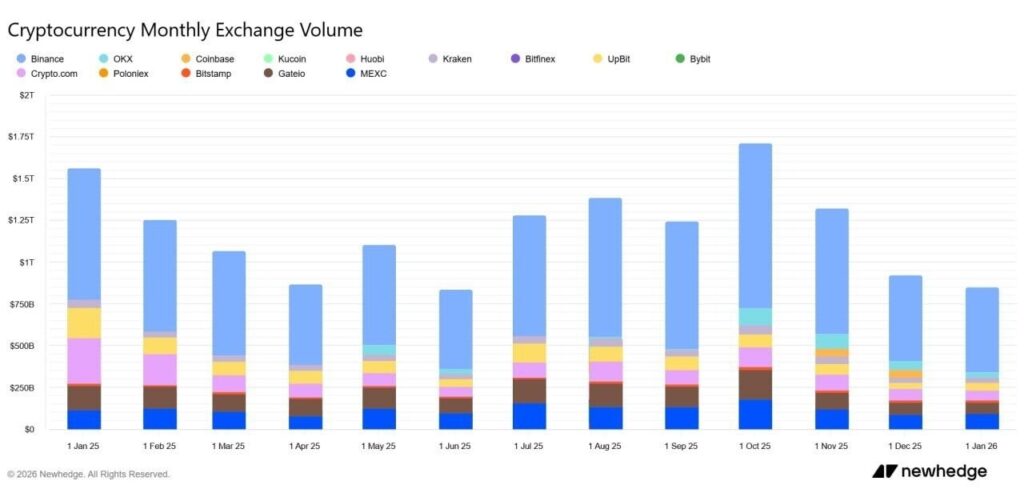

- Spot volume on centralized exchanges was about $1.1 trillion in January, which may be the lowest since July 2025. That shows a clear drop in speculative activity and risk appetite.

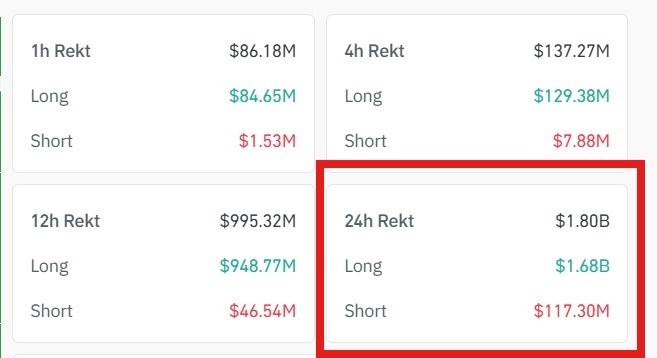

- In the last 24 hours of the week, liquidations topped $1.8 billion, and most of them were longs. Traders are still betting on upside with high leverage, and the market is punishing that optimism.

One day saw a clean example of altcoin fragility:

- Three early investors sold 36.36 million 1INCH, worth about $5 million, into thin order books.

- Price fell roughly 20% in hours, even though there was no protocol bug.

Fundamentals are one thing, but liquidity structure is another. When supply hits a shallow market, price can move violently.

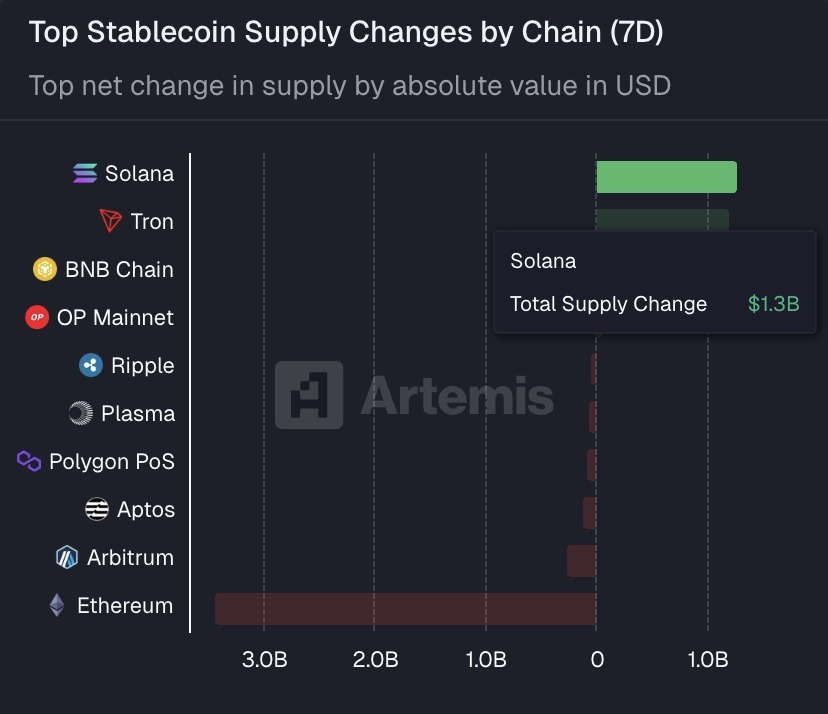

Meanwhile, stablecoin flows between networks shifted hard. Data showed that Solana saw more than $1.3 billion of stablecoin inflows in seven days, while Ethereum lost more than $3.4 billion in stablecoin supply over the same period. That is a big sign that users are increasingly comfortable moving liquidity to faster, cheaper chains for trading and DeFi.

Regulation and legal clarity: SEC rules, CLARITY Act, and Russia

Regulation was another major theme.

The U.S. SEC U.S. Securities and Exchange Commission issued new guidance on tokenized securities. It clarified how existing securities laws apply when assets are turned into tokens, and it drew a line between models where:

- the issuer itself runs the tokenization process, and

- models where third parties create token wrappers.

This moves tokenization from a “gray zone” toward a more defined legal framework, which is important for banks and big institutions.

In Congress, the CLARITY Act, a key bill that would define who regulates which parts of the crypto market (SEC vs CFTC), was supposed to get a Senate vote, but a heavy snowstorm in Washington delayed the vote to Thursday. That sounds trivial, but this law is seen as a turning point for the entire market. Legal clarity usually means easier institutional entry and better infrastructure. Even a weather delay becomes market news.

The White House is also planning a meeting on Monday with banking leaders and crypto executives to talk about this stalled crypto law. It looks like an attempt to break the deadlock and rebuild momentum.

Outside the U.S., Russia announced plans to open its crypto market in stages. A new regulatory framework should be put forward in July 2026, with full effect from July 2027, allowing legal trading for both “qualified” and retail investors. That is a clear move from ban-style thinking to “controlled opening.”

In the U.S. states, Rhode Island proposed a new bill to set up an official commission to study Bitcoin and blockchain. It is a small state, but it shows how crypto is now part of normal legislative work, not just an experiment on the side.

Banks, tokens, and the Ethereum vs Solana story

Several signals showed how traditional finance is moving deeper into crypto rails:

- A report from River said that 60% of the biggest 25 U.S. banks now have a positive stance toward Bitcoin. Not all of them are offering trading, but sentiment has clearly changed.

- Standard Chartered warned again that stablecoins could drain as much as $500 billion from U.S. bank deposits by 2028, as people shift into tokenized dollars.

- BlackRock argued that Ethereum is the main winner from global tokenization, since many tokenized assets and stablecoins already use its network as base infrastructure.

At the same time, Coinbase integrated Jupiter directly into its on-chain trading stack. That means:

- Millions of Solana-based tokens can now be traded through Coinbase,

- without each token going through traditional order-book listings,

- while users still use their normal Coinbase balances and payment methods.

Under the hood, it uses a self-custodial on-chain wallet, but the front-end experience stays close to a centralized exchange. It is a structural shift: a big CEX quietly becoming an on-chain router.

Put together with Solana’s stablecoin inflows and Ethereum’s role in tokenization, the picture is not “one winner, one loser.” It is more like Ethereum as base settlement and tokenization layer, and Solana as a high-speed trading and consumer layer, with big exchanges connecting both.

Corporates and institutions: stacking sats and rotating to ETH + AI

On the corporate side, the Bitcoin treasury story kept building:

- American Bitcoin, backed by the Trump family, added 416 BTC, bringing its holdings to 5,843 BTC.

- Metaplanet reported around $680 million in paper losses on its Bitcoin holdings for 2025, but still raised its profit guidance, because its Bitcoin-linked income business is growing.

- Michael Saylor’s firm, often referred to in this context as Strategy, bought 2,932 BTC for about $264.1 million at an average price of $90,061 per coin. At the same time, its mNAV fell to 0.86x, meaning the stock trades at a discount to its underlying asset value.

So you have companies facing big accounting losses but doubling down on accumulation, and the market sometimes still pricing them below asset value.

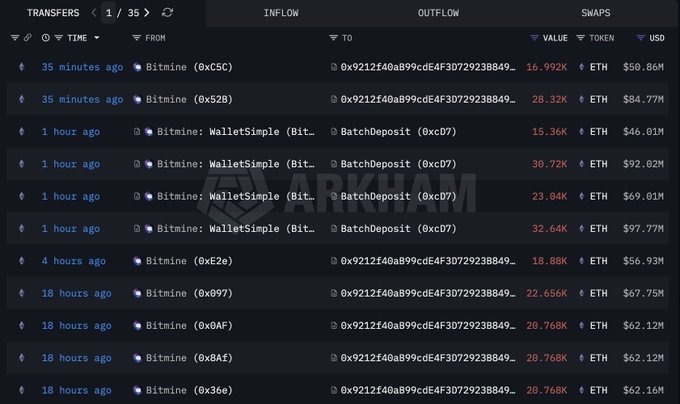

On the Ethereum side, BitMine, connected to investor Tom Lee, staked another 250,912 ETH (about $745 million). Total staked ETH by the firm is now roughly 2,582,963 ETH, worth around $7.67 billion, representing 61% of its total holdings. That is a huge bet on staking yield and Ethereum’s base-layer role.

At the same time, Bit Digital Bit Digital decided to exit Bitcoin mining and pivot toward Ethereum and AI infrastructure, via a stake in WhiteFiber WhiteFiber. The CEO said Bitcoin mining used to be efficient but now looks like a less effective use of capital compared with AI and Ethereum-linked infrastructure.

In the broader ecosystem:

- TRON DAO TRON DAO, led by Justin Sun, plans to increase its Bitcoin holdings, again showing how Bitcoin is becoming a reserve asset even inside other blockchain systems.

The pattern is clear: Bitcoin is the treasury and geopolitical asset; Ethereum is the tokenization and yield infrastructure; and some miners are now moving from pure hash-rate to broader AI + crypto compute plays.

Public voices: from TV studios to exchange CEOs

Several public figures helped shape the narrative this week:

- Tucker Carlson said Bitcoin could become the world’s reserve currency, replacing the dollar. That pushes Bitcoin deeper into the conversation about state power and monetary sovereignty.

- Brian Armstrong repeated his view that “even the haters will use crypto every day without knowing it.” His point: crypto will win not because everyone loves it, but because it becomes invisible infrastructure.

- A Goldman Sachs Goldman Sachs leader, Rob Kaplan, argued that investors are not fleeing the U.S. despite a weaker dollar; they are buying hedges like gold and alternative assets as risk management, not panic.

- Scott Bessent noted that markets now listen more to what is unsaid than what is in official speeches. With a new Fed chair, a weak dollar, and strong gold, traders are reading between the lines, not just the press release.

All of this shows that crypto has fully entered the mainstream debate on inflation, reserve currencies, and the future of money.

Trade, tariffs, and tax ideas

On the trade side, the office of the president in Seoul, South Korea said it received no prior notice about the tariff increases announced by Trump. That hints at stressed communication channels and rising trade tensions in Asia.

Trump also floated a very bold idea: a future where Americans pay no income tax, and the government is funded instead by tariffs and other revenue sources. It is only a statement for now, but if taken seriously, it would mean a complete redesign of U.S. fiscal policy and trade strategy.

For markets, that kind of talk is another reminder: policy risk is not just about rates or regulation; it is also about how governments choose to fund themselves.

Where does all this leave crypto right now?

To close the week:

- AI and big tech moved at extreme speed: mega-mergers in the Musk universe, new frontier models from China and Google, chips and GPUs lining up, humanoid robots doing housework, and new AR and audio hardware on the way.

- Washington passed a big funding bill, but let a DHS fight push the government into a technical shutdown, while a snowstorm delayed a key crypto law.

- A new Fed chair (Warsh), a weaker dollar, and wild moves in gold and silver showed how sensitive markets are to even small shifts in the rate story.

- Crypto markets themselves were oddly quiet on the surface, low volumes, high liquidations, lots of waiting, while under the surface:

- companies and states stacked Bitcoin and Ethereum,

- stablecoins and tokenization kept moving forward,

- and large players rotated between metals, tokenized gold, and BTC.

It was a week where AI and hardware clearly moved into a new phase, while crypto and macro stayed in a holding pattern, waiting for clearer signals from the Fed, Congress, and the shutdown talks.

The tension between those two timelines, the fast AI world and the slow political world, is exactly what will shape risk, liquidity, and narrative in the weeks ahead.

Note

This article is for information only. It is not financial advice.

Markets move fast, and there is always risk when you trade or invest.

Please do your own research (DYOR) before making any decision.

If you want to learn more, you can read guides and market explainers on blog.millionero.com.

When you feel ready and understand the risks, you can trade spot and futures on Millionero in your own way and at your own pace.