A week that started with relief and ended with strain

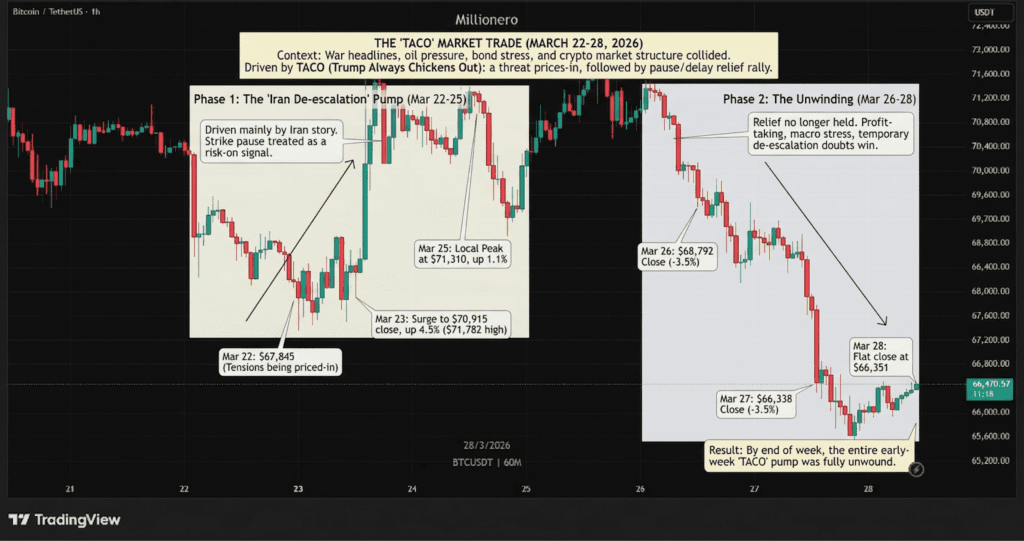

This was a week where war headlines, oil pressure, bond stress, and crypto market structure all kept colliding. At the center of it was the idea traders kept calling TACO, short for “Trump Always Chickens Out.” The logic was simple: a major threat gets priced in, risk assets fall, then a pause or delay brings a fast relief rally. That is exactly how the week began. It is also why the week felt so unstable by the end.

Bitcoin came into Sunday, March 22 at $67,845, down 1.5%, already sitting below $70,000 as Iran tensions were being priced in. On Monday, March 23, after a pause in threatened strikes on Iran’s energy and power infrastructure, Bitcoin surged to a $70,915 close, up 4.5%, with a high of $71,782. Tuesday, March 24 brought a mild cooldown, with Bitcoin closing at $70,518, down 0.6%. Wednesday, March 25 became the local peak at $71,310, up 1.1%, as the de-escalation story was still holding.

Then the move broke. Thursday, March 26, Bitcoin closed at $68,792, down 3.5%. Friday, March 27, it fell again to $66,338, another 3.5% drop. By Saturday, March 28, it was almost flat at $66,351, but the message was clear: the entire early-week TACO pump had been unwound.

Early in the week, this price action was driven mainly by the Iran story. The market treated the strike pause as a risk-on signal, and Bitcoin responded fast. But by the second half of the week, that relief no longer held. Profit-taking, broader macro stress, and the feeling that the de-escalation might only be temporary started to win.

War developments kept driving the tone

The conflict reached a new symbolic point

One of the clearest markers of the week was that the Iran war officially reached its one-month mark. That alone gave the market a sense that this was no longer a short shock. It had become a continuing risk with regional and global consequences.

The danger around energy routes stayed central. There was a warning that Yemen’s Houthi group was ready to intervene if new allies joined the US and Israel or if the Red Sea was used to launch attacks on Iran. That mattered because of geography: the Bab al-Mandab Strait controls more than 6 million barrels of daily oil supply, and if both Hormuz and Bab al-Mandab were disrupted, total offline capacity could approach 25 million barrels per day, or roughly 25% of global supply. That is the kind of number that changes how markets think about war.

Earlier in the week, there had already been a grave warning from Iran that any attack on Khark Island would be met with an unexpected response. That island is not a minor target. Around 90% of Iranian oil exports pass through it. Even before the week’s main moves began, that made clear how sensitive the oil market had become.

Strikes, threats, and changing alliances

The military picture also escalated sharply. There were reports that US and Israeli forces struck Iran’s energy system and hit a major gas pipeline feeding a power plant in Khorramshahr. Oil reacted immediately, with prices jumping by almost 4% in a very short time. There was also a major strike on Tehran’s electrical grid, causing widespread blackouts and showing that the conflict was moving deeper into critical infrastructure.

At the same time, the regional political map looked like it was shifting. One major development suggested that Saudi Arabia and the UAE were moving closer to direct involvement in the conflict. Saudi Arabia was said to have approved American use of King Fahd Air Base, and the idea that Saudi entry into the war had become only a matter of time gave the whole situation a much heavier feel. That was reinforced by a striking political speech in which the Saudi crown prince compared Iran’s supreme leader to Hitler, warning about expansion and saying he did not want the region to wait until it was too late.

The wider international tone also hardened. North Korea’s leader officially labeled the United States a terrorist state, adding yet another layer of geopolitical tension during an already fragile week.

Negotiation talk kept colliding with escalation talk

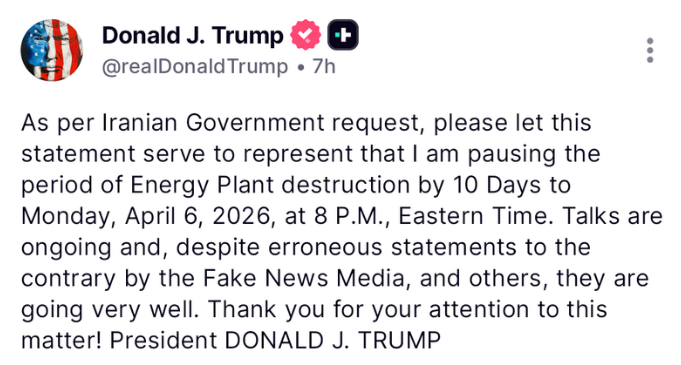

The strange thing about this week was that de-escalation headlines and escalation headlines kept arriving side by side. On one hand, there were reports of productive and constructive talks between the US and Iran, and because of that, Trump ordered a five-day delay on strikes targeting Iranian infrastructure. That pause was the spark for the early Bitcoin rally.

But the pause always looked fragile. It came with conditions, and later in the week it was extended by 10 more days, pushing the new deadline to Monday, April 6, 2026 at 8:00 PM New York time. Trump described negotiations as going very well. At the same time, though, his language turned more aggressive, with claims that Iranian negotiators were “begging” for a deal while only publicly saying they were studying the proposal. He also warned that if Iran did not get serious soon, there would be no turning back and the result would not be pretty.

Even more striking were the stated political goals around Iran. Trump spoke openly about Hormuz reopening under joint management, possibly joint leadership, and he also spoke in unusually direct terms about regime change, even suggesting that a new leader might be found, as happened in Venezuela. That made it harder for markets to fully trust the pause story.

Iran’s own reported conditions for a ceasefire also showed how far apart both sides still looked. The conditions included lifting all US sanctions, war compensation, greater influence over the Strait of Hormuz, no restrictions on the ballistic missile program, and guarantees against another American military attack.

The war’s effects spread beyond Iran

The conflict did not stay limited to the Gulf. One update showed Ukraine striking Russia’s largest oil export terminal on the Baltic Sea for the third straight night, focusing attention on Ust-Luga and Primorsk, both important for Russian oil exports. Russia had been expected to benefit most from an Iran-related oil shock, but this pressure on its own export infrastructure complicated that picture.

There was also a report that Iran granted Spain safe passage through Hormuz because Madrid had opposed supporting US military operations. That detail mattered because it showed how shipping risk was becoming political, not just military.

At the same time, the energy shock was said to be spreading into daily life elsewhere. Reports pointed to a gas shortage in the Philippines severe enough that some people were walking to work because of rising costs or lack of fuel.

Bonds, oil, and macro pressure started to dominate

Oil stayed high while the bond market sent a warning

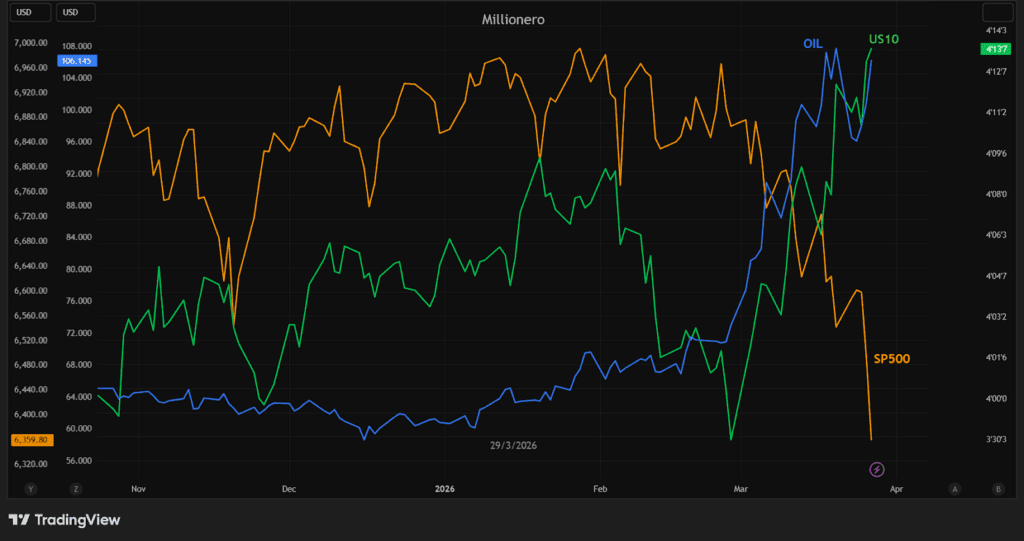

By the end of the week, the mood had clearly shifted from relief to strain. US oil was at $101 per barrel, the S&P 500 was at a 232-day low, and the US 10-year Treasury yield stood at 4.44%. The next 50 hours before futures reopened on Sunday were described as especially important, with growing pressure on Trump and Treasury Secretary Bessent to contain the bond market before it got worse.

This concern was not just about yields drifting higher. One of the most alarming macro updates of the week was a $69 billion US Treasury auction described as catastrophic. The bid-to-cover ratio was the weakest since May 2024, and banks took the largest share since October 2022. The deeper message was simple: when the market’s so-called safest asset struggles to attract real buyers, confidence is no longer normal.

War stress was already hitting equities too. At one point, US markets were said to have lost more than $1 trillion in a single day.

Debt, inflation, and global pressure added to the stress

Another major macro warning came from the IMF, which said global public debt is nearing the size of the entire world economy, at its highest level since World War II. That added a bigger background problem to a week already full of immediate shocks.

From Japan came a different signal. Inflation fell to 1.3%, the lowest in four years, which helped support the market idea that softer global inflation could lead central banks to slow rate hikes, compress bond yields, and help risk assets like crypto. But even that story came with a major warning attached: oil above $114 and an active Middle East war could quickly undo this softer-inflation setup.

In Europe, rising oil costs were already shaping positioning. UBS cut Eurozone equities to a defensive stance, arguing that even a region not joining the war was still paying for it economically.

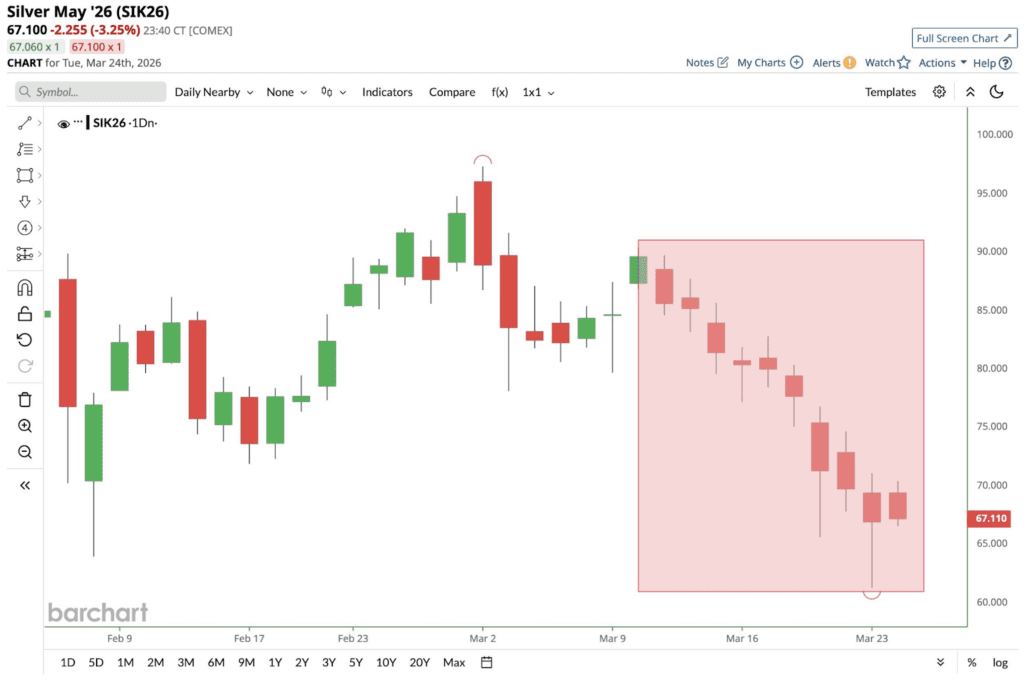

Other market signals pointed to stress too. Silver headed for a tenth straight red close, its longest losing streak since April-May 2022.

Crypto held up in some places and cracked in others

Bitcoin ETFs, treasuries, and miner flows sent mixed signals

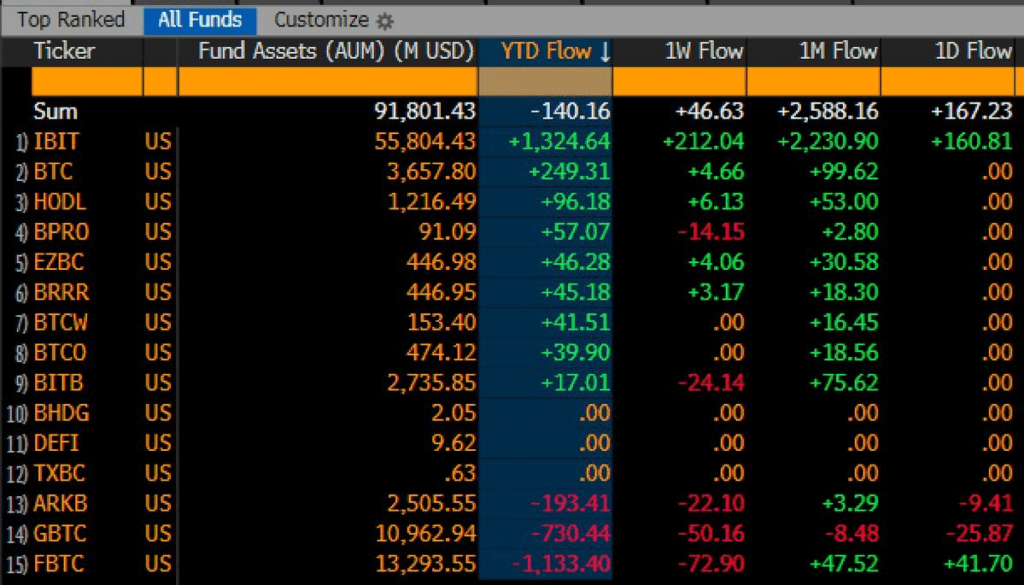

Crypto was not a simple risk-off story this week. Even while Bitcoin lost its early bounce, some structural data still looked strong. One update said Bitcoin ETFs took in $2.5 billion this month alone, with IBIT ranking in the top 2% of all ETFs by flows. That came despite Bitcoin being down 40% over six months, which was presented as a sign of unusually persistent demand. The comparison was sharp: when gold suffered a similar drop a decade ago, about one-third of investors left.

But that was not the whole picture. Later in the week, US Bitcoin ETFs saw their biggest outflows in three weeks, and Ark Invest cut its holdings in its own Bitcoin fund. So the week showed both things at once: deeper capital still present in the space, but short-term pressure clearly rising again.

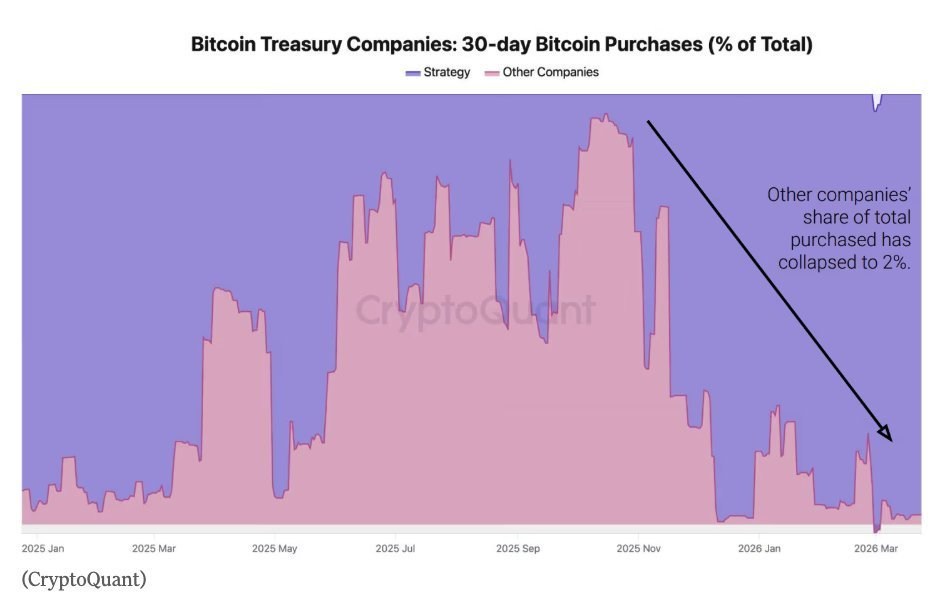

Corporate Bitcoin also stayed concentrated. Strategy now holds 76% of all corporate Bitcoin, and it bought nearly 45,000 BTC in 30 days, the fastest pace since April 2025. At the same time, the collapse from $110,000 to below $70,000 was said to have pushed many institutional buyers underwater.

Miners added pressure too. Marathon Digital sold 15,133 BTC worth more than $1 billion, one of the largest miner sales seen in a long time.

Stablecoins, tokenization, and crypto payments kept moving forward

Even in a rough macro week, crypto infrastructure kept advancing.

One important stablecoin development was that USDT moved toward a more formal audit structure, bringing in KPMG as its official auditor and PwC as part of preparation for a funding round and broader US expansion. In the context of new stablecoin legislation, that pushed the conversation further toward transparency and institutional acceptability.

At the same time, there was another fight over stablecoin design. Coinbase pushed back against the latest Clarity Act draft, arguing that the proposed rules could restrict how stablecoin yields are structured. The key issue was that the draft would ban passive yield while still allowing activity-based rewards under an “economic equivalence” standard.

Tokenization also stayed near the front of the week’s narrative. There was growing expectation that a Tokenization Innovation Exemption from the SEC could arrive within weeks. If it does, it could make it easier to launch tokenized financial products, reduce some barriers around innovation, and invite stronger institutional participation.

That theme was echoed by the view that tokenization could change finance the way the internet changed everything in 1996, according to Larry Fink, Dangerously powerful man, CEO of Blackrock. It was also linked to another broader idea: that Bitcoin and crypto may become native money for AI agents, making digital money and artificial intelligence look less like separate trends and more like a future merger.

Payments, mortgages, and machine-to-machine finance expanded

The idea of crypto being used in everyday systems also advanced this week.

Fannie Mae, which manages $4.3 trillion in assets, was said to be accepting crypto-backed mortgages, marking a notable shift in how digital assets are treated inside the US housing finance system.

On the payments side, Solana moved deeper into machine-to-machine commerce. It officially supported the MPP protocol from Stripe and Tempo, allowing stablecoin payments for APIs built on the MPP SDK. The simple version is that machines and software can now pay each other directly over blockchain rails.

Related to that, the Solana Foundation prepared the launch of the X402 Base Agentic Payments Gateway, aimed at smart applications and designed to let merchants accept stablecoins without needing complicated technical integration.

There was also a smaller but still telling retail-facing update: Metaplanet announced a shareholder card for the summer, with 1.6% of each purchase returned in Bitcoin.

And on the Ethereum side, Tom Lee (Bitmine) bought about 67,111 ETH worth $144.8 million, using two separate addresses in a Tuesday transaction. He has been an aggressive buyer since the last pico-top of Ethereum to this day.

DeFi risk and odd political side stories stayed in the background

Not all crypto news was constructive. One of the week’s sharpest failures came from Resolv Labs, where the USR stablecoin collapsed 80% after a serious exploit. Attackers reportedly used compromised private keys to mint 80 million unbacked USR and steal $23 million in cash, setting off broader losses across DeFi vaults. It was framed as the third such incident in a few weeks, following problems involving Aave and Tornado Cash. The lesson was familiar: in DeFi, broken key security can do systemic damage very quickly.

There was also a more unusual political-crypto crossover when Senator Elizabeth Warren said she had questions for MrBeast’s crypto plans after his acquisition of a banking app.

The week closed with more questions than answers

The cleanest way to describe this week is that it began with a pause-driven relief rally and ended with the market no longer trusting the pause. Bitcoin’s move from $67,845 to $71,310 and back down to $66,351 captured that perfectly. The early story was that a delay in strikes had reduced risk. The late-week story was that the war still looked open, oil was still high, bond stress was still building, and even a truce extension did not remove the deeper fear.

At the same time, crypto itself kept showing two faces. One face was fragile: ETF outflows, miner selling, a stablecoin collapse, and a failed relief rally. The other face was still building: institutional ETF demand over the month, tokenization momentum, crypto-backed mortgages, stablecoin payment infrastructure, AI-and-Bitcoin narratives, and continued corporate treasury concentration.

That is what made this week feel so heavy. Nothing fully broke, but nothing fully settled either. The war widened, the bond market flashed warning signs, oil stayed dangerous, and crypto spent the week moving between structural progress and immediate pressure.

This article is for informational purposes only and should not be considered financial advice. Always do your own research before making any investment decisions.

For more market breakdowns, explainers, and weekly recaps, visit blog.millionero.com.

You can also trade spot and perpetuals on Millionero.