The week started with a market that went through a sharp risk swing over the weekend and then stabilized with a firmer tone. Bitcoin (BTC) had a volatile but strongly bullish UTC session on March 30. It quickly dropped to a daily low of $65,812, then reversed hard and climbed to a daily high in the $67,640-$67,722 area. By around 7:05-7:08 AM UTC, it was sitting near $67,200-$67,215.

That move happened while broader risk sentiment also improved at the margin. S&P 500 futures erased all losses and turned green, which showed that markets were still willing to buy risk even with the geopolitical backdrop getting heavier. The key point from the weekend is that price action stayed very reactive, but the recovery in Bitcoin and the rebound in equity futures suggested that traders were still leaning toward buying dips rather than staying fully defensive.

Geopolitics Drove the Weekend Narrative

US-Iran tensions moved to the center again

The biggest driver over the weekend was the continued rise in headlines tied to Iran, the United States, and the wider regional spillover risk.

US President Trump said,

That statement came after another series of reports pointing to a more serious phase of the conflict.

At the same time, there was a report that Trump is weighing a military operation to extract nearly 1,000 pounds of uranium from Iran. The details were significant. The mission was described as complex and risky, and it would likely place American forces inside Iran for days or longer. It was also presented as part of Trump’s central objective of preventing Iran from ever making a nuclear weapon. Alongside that, he reportedly encouraged advisers to pressure Iran into surrendering the material as a condition for ending the war. Even with that pressure building, US and Iran have not yet entered direct negotiations to end the war. Taken together, that pointed to another sign of possible US ground operations in Iran.

Another development pushed the same idea further. Tehran accused Washington of deception. Iran’s Speaker of Parliament said the United States is speaking publicly about negotiations while secretly planning a ground attack, and Iranian forces were said to be at maximum readiness to receive any American ground landing. That message followed a separate report that the Pentagon is planning ground operations lasting for weeks inside Iran, while US forces have already started repositioning for rapid deployment. Oil markets were described as watching each new development very closely.

The troop picture remained central

The military balance was also part of the weekend discussion. The United States is now reported to have more than 50,000 troops deployed in the Middle East. At the same time, there was also a blunt point made about the scale problem: Iran has 93 million people, is close to a third of the size of the continental United States, and taking or holding a country of that size, complexity, and military capability with 50,000 troops was described as not doable.

That did not reduce the seriousness of the situation. It simply showed that the market is now dealing not only with escalation risk, but also with uncertainty around what an actual operation could look like and how far it could realistically go.

Oil became a direct policy topic

The weekend also brought a very direct and aggressive statement on energy. Trump said he wants to “take the oil in Iran” and could seize the export hub of Kharg Island. He added that taking Iran’s oil is his preferred option and dismissed domestic criticism of that idea. That comment mattered because it turned the oil market from a secondary consequence of the conflict into a more explicit part of the political discussion itself.

Energy Shock Spread Across Regions

Brent moved above $105 and Asia felt the pressure

The oil move became one of the clearest market signals of the weekend. Brent crude officially surged above $105 per barrel, and that was presented as further proof that Asia’s energy crisis is intensifying.

Japan’s stock market then fell nearly -5%, another sign that the rise in energy stress was not staying isolated to commodities. It was moving directly into equities and broader regional risk pricing.

Maritime pressure widened beyond Hormuz

The pressure on global trade routes also increased. The Houthis in Yemen threatened to close the Bab el-Mandeb Strait. That matters because the strait handles 12% of global trade volume, making it the second major maritime route under threat after Hormuz. In practical terms, that means the market is no longer looking only at one chokepoint. It is now looking at a second major shipping corridor entering the danger zone.

Political Cross-Currents Added to Market Confusion

Conflicting alignments and policy reversals stacked up quickly

One of the strangest parts of the weekend was how many conflicting geopolitical and market signals appeared at once.

The situation was framed this way:

- Iran is providing investment advice to US traders and calling pre-market news a reverse indicator.

- The United States is removing sanctions on Russian crude oil.

- Russia is assisting Iran with intelligence and strikes on US bases.

- China is actively calling for an immediate end to the Iran war.

- Spain has banned the United States from using its military bases for strikes on Iran.

- President Trump is saying the US no longer needs NATO.

Each one of those points matters on its own, but together they showed how fragmented and unstable the geopolitical map has become. Markets are not just pricing one war headline. They are pricing a rapidly shifting set of energy, military, alliance, and policy relationships.

Even the rhetoric toward traders changed

Another unusual development came from Iran’s Speaker of Parliament, who gave direct trading advice to investors in US markets. His message was that pre-market so-called “news” or “Truth” is often just a setup for profit-taking and should be treated as a reverse indicator. The advice was simple: if they pump it, short it; if they dump it, go long. That stood out because the conflict is now producing not only military and commodity headlines, but also direct public attempts to shape trader behavior.

Japan and the Yen Became Another Pressure Point

Tokyo signaled that intervention risk is rising again

Away from the Middle East, Japan issued its strongest warning yet on the yen. The deputy finance minister signaled that “decisive action” could come soon, which is the same language that came before direct intervention in 2022 and 2024.

The yen opened at 160.30, its weakest level since 2024. At the same time, the Bank of Japan was described as unable to raise rates above 0.75% because doing so during the Iran war could overwhelm the economy. That left direct dollar selling as the only practical tool still available to the government.

YEN/USD

The intervention signals continued to build. The finance minister used the phrase “bold action.” The central bank governor was questioned in parliament about whether raising rates could address yen weakness. Japan was also said to be exploring intervention in the oil futures market to reduce the pressure that higher crude prices are putting on the currency. The verbal warnings have now been delivered, and the message from the weekend was that the next move may be a real one in the market.

Other Weekend Developments in Crypto and Market Structure

Tokenized stocks crossed a new threshold

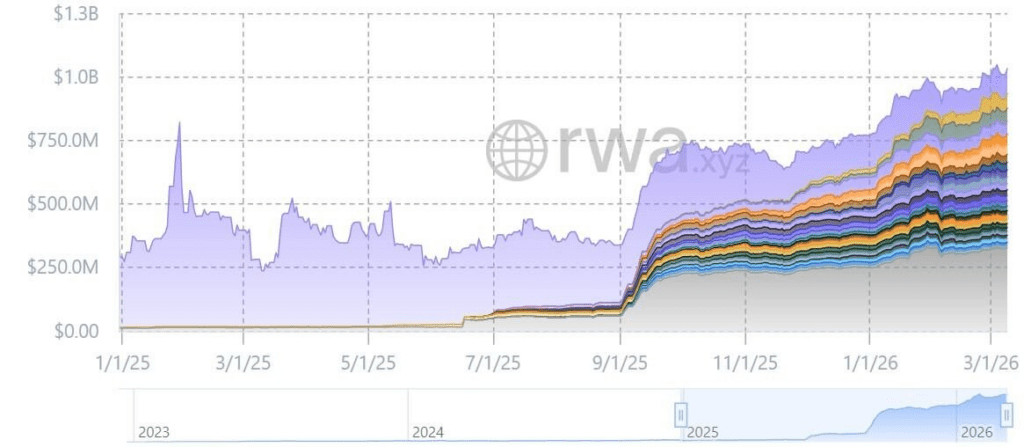

Another market update over the weekend was that tokenized stocks surpassed $1 billion in total value on blockchain. That is a separate theme from the geopolitical risk story, but it still fits into the broader market picture because it shows continued growth in tokenized financial exposure even while macro conditions remain unstable.

A quiet weekend was itself treated as a signal

There was also a notable observation that this weekend felt eerily quiet. For the first time since the Iran war began, Trump was described as unusually silent for part of the weekend, with no fresh headlines, no more aggressive strikes, and no comment on the bond market situation. In a setting where escalation risks are already high, that silence itself was treated as meaningful.

The US Week Ahead: Powell, Labor Data, and Rate Expectations

Monday: Powell

The US calendar begins with a speech from Federal Reserve Chair Powell. In the current environment, that matters because markets are trying to understand how the Fed reads a very difficult mix: geopolitical stress, higher energy prices, unstable risk sentiment, and an important week for labor data.

If Powell sounds focused on inflation risks, especially with oil rising sharply, markets may assume the Fed still wants to stay cautious on rate cuts. If he sounds more balanced and puts more weight on slowing activity or rising uncertainty, traders may lean back toward easier policy expectations later on. Right now, tone matters almost as much as data.

Tuesday: Consumer Confidence and JOLTS

Tuesday brings Consumer Confidence and JOLTS job openings. These two reports help show how strong demand and hiring conditions still are beneath the headline volatility.

Consumer confidence gives a read on how households feel about the economy. If confidence weakens, it can point to softer spending ahead. If it stays firm, it suggests consumers are still holding up despite war headlines and energy pressure.

JOLTS matters because it gives another look at labor demand. A high number of job openings would suggest the labor market is still tight, which can keep wage pressure and inflation concerns alive. A softer number would support the idea that labor demand is cooling, which is more consistent with a Fed that could eventually move toward cuts.

Thursday: Jobless Claims and Trade Balance

Thursday brings Initial Jobless Claims and the Trade Balance.

Jobless claims are one of the quickest reads on labor market stress. If claims remain low, the labor market still looks durable. If claims start rising, that can be an early sign that conditions are loosening. For the Fed, that distinction matters. A still-tight labor market can delay rate cuts. A softer labor picture can bring them back into discussion.

The trade balance is not usually the first market driver in a week like this, but it still matters because it helps show the shape of demand, imports, exports, and broader growth conditions. In a week already shaped by energy stress and geopolitical risk, it gives more context for how the US economy is absorbing external shocks.

Friday: NFP

Friday is the main event with Non-Farm Payrolls (NFP). This is the number the market will likely treat as the most important scheduled release of the week.

NFP will shape the conversation around the labor market more than any other report this week. A strong payroll number would suggest hiring is still solid, which would support the idea that the economy remains resilient. But in the current setting, strong labor data can also make it harder for the Fed to cut rates quickly, especially if inflation risks are being pushed up again by oil.

A weak NFP number would do the opposite. It would raise concerns about labor softness and growth, but it could also strengthen expectations for future Fed easing. That is why this week feels so important. The market is not just asking whether the economy is strong or weak. It is asking whether the economy is cooling enough to change the rate path, while inflation risks remain alive in the background.

Why This Week Matters for Inflation, Labor, and the Fed

The core issue this week is simple. The market is balancing two forces at the same time.

On one side, higher oil prices, Middle East escalation, and supply route threats keep inflation risk in view. If energy stays elevated, it can make inflation harder to bring down and make the Fed more cautious.

On the other side, the market is watching whether the labor market is still tight or finally starting to cool in a clearer way. If labor data softens, that could open more room for future rate cuts. If labor data stays strong, the Fed may have less reason to move soon.

That is why Powell, JOLTS, jobless claims, and NFP all matter so much together. They are not isolated numbers this week. They are all feeding into one question: does the Fed need to stay patient because inflation risk is not finished, or is the economy cooling enough to justify a softer policy path later on?

Token Unlocks

OP (OP)

Date: March 31, 2026

Unlock Value: $3.19M

% of Circulating Supply: 1.55%

Number of Tokens: 31.27M OP

DYDX (DYDX)

Date: April 1, 2026

Unlock Value: $392.43K

% of Circulating Supply: 0.55%

Number of Tokens: 4.17M DYDX

IOTA (IOTA)

Date: April 1, 2026

Unlock Value: $662.06K

% of Circulating Supply: 0.32%

Number of Tokens: 12.26M IOTA

DICE (DICE)

Date: April 1, 2026

Unlock Value: $11.02K

% of Circulating Supply: 1.80%

Number of Tokens: 12.54M DICE

Sui (SUI)

Date: April 1, 2026

Unlock Value: $36.36M

% of Circulating Supply: 1.10%

Number of Tokens: 42.9M SUI

EIGEN (EIGEN)

Date: April 1, 2026

Unlock Value: $6.16M

% of Circulating Supply: 7.54%

Number of Tokens: 36.89M EIGEN

AERO (AERO)

Date: April 2, 2026

Unlock Value: $6.31

% of Circulating Supply: <0.01%

Number of Tokens: 20.03 AERO

Wormhole (W)

Date: April 3, 2026

Unlock Value: $736.58K

% of Circulating Supply: 0.90%

Number of Tokens: 49.11M W

Gunz (GUN)

Date: March 31, 2026

Unlock Value: $5.59M

% of Circulating Supply: 20.48%

Number of Tokens: 354M GUN

Ethena (ENA)

Date: April 5, 2026

Unlock Value: $15.58M

% of Circulating Supply: 2.18%

Number of Tokens: 171.88M ENA

Closing View

The week opens with Bitcoin recovering strongly, equity futures stabilizing, and macro risk still dominated by war, oil, and policy uncertainty. The weekend brought rising concern about possible US ground involvement in Iran, more stress on energy markets, direct pressure on the yen, and fresh signs that shipping routes and alliances are becoming part of the market story.

Now the focus shifts to the United States. Powell speaks first, but the real test will come from labor and confidence data through the week, ending with NFP. If the numbers stay firm, markets may price a more patient Fed. If they weaken, rate-cut expectations may build again. For now, the market is moving through a week where geopolitics and macro data are fully connected, and both sides of that story matter at the same time.

Crypto markets can move quickly, and every trader’s goals and risk tolerance are different. This content is for general information only and should not be treated as financial advice. If you want more market context, read our blog, and if you choose to take action, trade responsibly on Millionero.