The new week opens with markets under pressure from several directions at once. Over the weekend, the focus quickly moved from US-China trade developments to rising geopolitical tension around war, a sharp jump in oil prices, stress in the US bond market, and a sudden fall in Bitcoin.

This creates a difficult setup for the coming days. Investors are now watching trade policy, inflation risk, Federal Reserve expectations, Nvidia earnings, US economic data, and major crypto token unlocks at the same time.

Weekend Developments: US-China Trade Talks Bring Several Major Announcements

New Trade Deals After the Trump-Xi Meeting

The White House announced several US-China trade deals and developments after US President Trump’s meeting with China’s President Xi. The details included a set of agreements across critical minerals, aircraft, agriculture, beef, and poultry.

China will address US concerns about supply chain shortages related to rare earths and other critical minerals. This matters because rare earths are important for technology, defense, manufacturing, and clean energy supply chains. Any improvement in this area could reduce pressure on companies that depend on these materials.

China also approved an initial purchase of 200 American-made Boeing aircraft for Chinese airlines. This is a major development for US manufacturing and could support sentiment around industrial and aerospace stocks.

In agriculture, China will purchase at least $17 billion per year of US agricultural products in 2026, 2027, and 2028. China also restored market access for US beef by renewing expired listings of more than 400 US beef facilities and adding new listings. It also resumed imports of poultry from US states determined by the USDA to be free of highly pathogenic avian influenza.

Xi is expected to visit the White House this fall, which means trade relations may remain an active market topic over the coming months.

US-China Boards of Trade and Investment

The White House also announced the establishment of the US-China Boards of Trade and Investment to “optimize the bilateral economic relationship” between the two countries.

The Board of Trade will allow the US Government and China to manage bilateral trade across non-sensitive goods. The Board of Investment will create a government-to-government forum for discussing investment-related issues.

This announcement came only days after the US-China summit. For markets, the key point is that trade talks are moving into a more formal structure. That may reduce some uncertainty, but it also keeps US-China relations at the center of global economic attention.

Geopolitical Risk Returns as Iran Tensions Rise

While trade news gave markets one major story, geopolitical risk quickly became the more urgent concern. Tensions around Iran escalated again after US and Israeli warnings about a possible return to military operations.

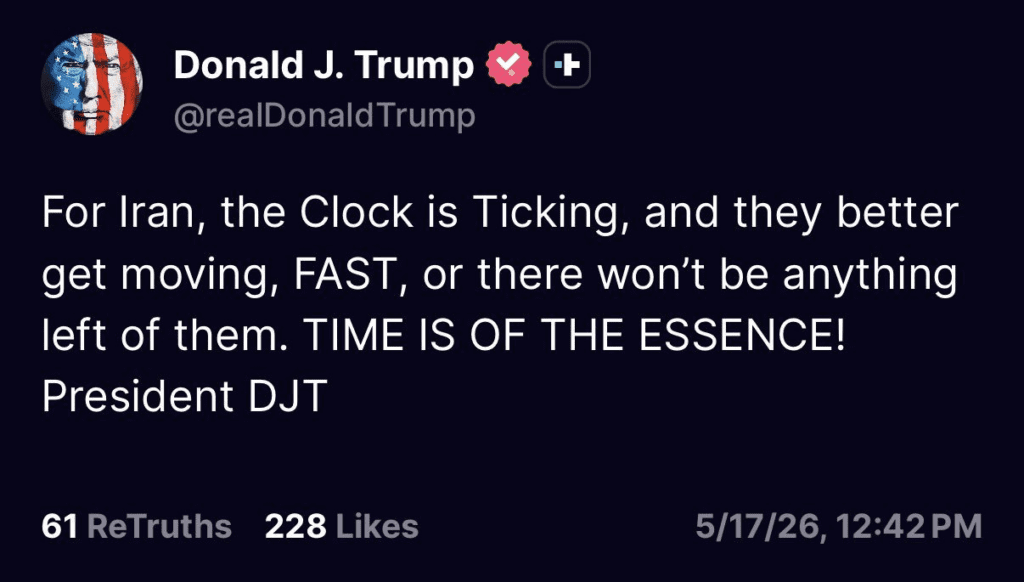

Trump warned: “The Iranians need to beware of me.” An Israeli official said Washington and Tel Aviv had raised alert levels because of the possibility of resumed fighting. Reports also pointed to the potential for joint attacks if Trump gives the green light.

Trump is seeking a deal to end the war, but Iran’s failure to offer concessions could bring the military option back to the table. In his latest remarks, Trump said Iran “must move quickly or there will be nothing left of them.”

Oil Surges Above $107 as the “Clock Is Ticking”

The clearest market reaction came from oil. Oil prices surged above $107/barrel after Trump told Iran that the “clock is ticking.”

Higher oil prices can feed directly into inflation. If energy prices stay high, headline inflation may rise again, household costs may increase, and the Federal Reserve may have less room to cut rates.

That is why oil is now connected to almost every major market question this week. A high oil price does not only affect energy stocks. It also affects inflation expectations, bond yields, consumer confidence, and the path of future Federal Reserve policy.

Bond Market Stress Deepens as the 10Y Yield Hits 4.63%

The US bond market also moved sharply. On Sunday night, the US 10Y Note Yield reached 4.63%, its highest level since February 2025.

This level is especially important because it is now around 4 basis points above the high that prompted Trump’s “90-day tariff pause” in April 2025. The 10Y Note Yield is now up +70 basis points since the Iran War, while US mortgage rates are nearing 7.00%+.

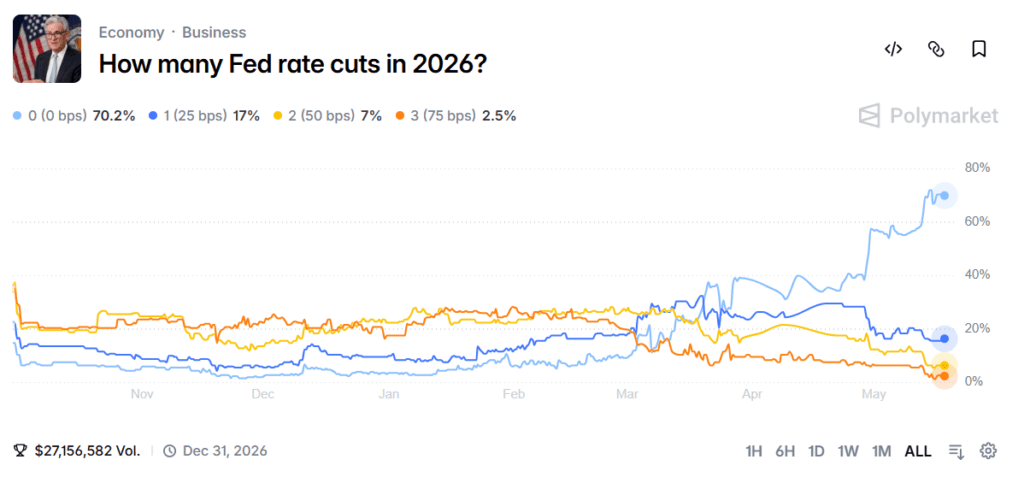

At the same time, the odds of rate cuts have collapsed to 17% this year, while US inflation is nearing 4%+. This creates a very tight situation for markets. Higher yields make borrowing more expensive, pressure housing, reduce the appeal of risk assets, and signal that investors are demanding more return to hold US debt.

Inflation fear and geopolitical risk are making rate cuts harder to expect.

Bitcoin Falls Below $77,000 After a Major Long Squeeze

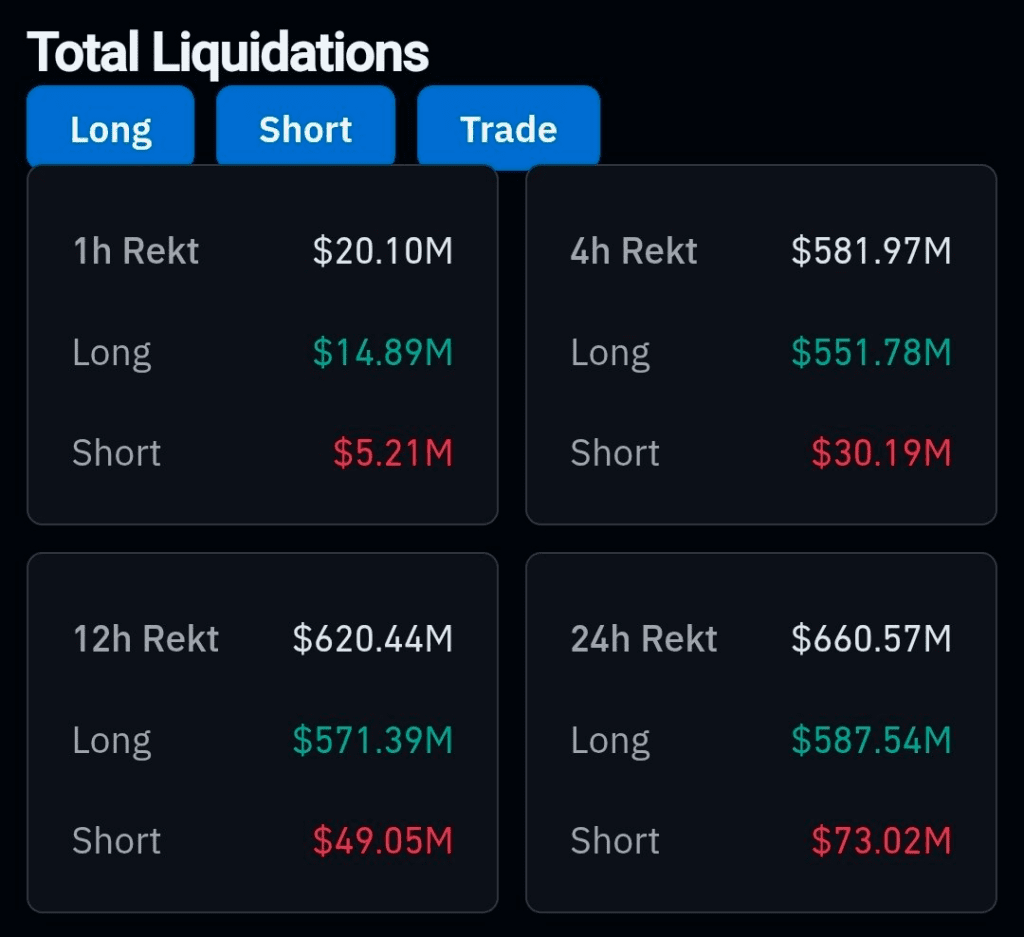

Bitcoin also came under heavy pressure. Bitcoin fell below $77,000 as more than $500 million worth of levered long positions were liquidated in just 60 minutes.

A separate market status update pointed to a strong technical rejection from Bitcoin’s 200 Day MA line, described as a pivotal point. The selling wave was also linked to institutions, especially BlackRock, and to Trump’s recent statements about the possibility of war returning. These comments spooked markets at a time when traders were already sensitive to risk.

The liquidation event reached $650 million in the last 24 hours, with most of it coming from longs. This is a classic Long Squeeze: too many traders are positioned in the same direction, price moves against them, liquidations trigger more forced selling, and the move becomes sharper.

The current expectation is for Bitcoin to visit the bottom of the ascending channel as the first target. After that, the market can reassess. By that point, Bitcoin dominance may rise, which would usually be negative for altcoins.

Markets hate uncertainty. With war risk, oil pressure, rising yields, and weak crypto technicals all happening together, traders may stay defensive until the picture becomes clearer.

Upcoming Events This Week

The week ahead is packed, but the main focus is clear. Markets will watch Federal Reserve signals, Nvidia earnings, housing data, manufacturing data, and consumer sentiment. These events matter more than usual because the market is already dealing with high oil prices, rising bond yields, inflation near 4%+, and collapsed rate cut expectations. Any strong inflation signal or strong economic number could support the idea that rates may stay higher for longer.

The most important event is Wednesday’s U.S. Federal Reserve Meeting Minutes, because traders want to know how seriously the Fed is treating inflation and whether rate cuts are still realistic this year. The second major event is $NVDA Company Results, also on Wednesday, because Nvidia is currently one of the most influential companies for AI, tech stocks, and broader risk sentiment.

Key events this week:

- Tuesday: April Pending Home Sales Data

- Wednesday: U.S. Federal Reserve Meeting Minutes

- Wednesday: $NVDA Company Results, The Biggest Earnings Event This Quarter

- Thursday: May Philadelphia Industrial Index

- Friday: University of Michigan Consumer Confidence Data

- Friday: May Consumer Expectations

Crypto Token Unlocks This Week

Token unlocks will also be watched closely, especially with Bitcoin already under pressure and Bitcoin dominance expected to rise. In this kind of market, large unlocks can matter more because liquidity is weaker and altcoins may already be vulnerable.

Pyth Network (PYTH)

Date: May 19, 2026

Unlock Value: 95.5M USDT

% of Circulating supply: 36.96%

Number of Tokens: 2.13B PYTH

LayerZero (ZRO)

Date: May 20, 2026

Unlock Value: 33.4M USDT

% of Circulating supply: 5.07%

Number of Tokens: 25.71M ZRO

MBG by Multibank Group (MBG)

Date: May 22, 2026

Unlock Value: 8.7M USDT

% of Circulating supply: 8.09%

Number of Tokens: 27.15M MBG

KAITO (KAITO)

Date: May 20, 2026

Unlock Value: 7.9M USDT

% of Circulating supply: 4.7%

Number of Tokens: 17.6M KAITO

YZY (YZY)

Date: May 18, 2026

Unlock Value: 6.2M USDT

% of Circulating supply: 4.46%

Number of Tokens: 20.83M YZY

SoSoValue (SOSO)

Date: May 22, 2026

Unlock Value: 5M USDT

% of Circulating supply: 4.17%

Number of Tokens: 13.32M SOSO

The Main Market Question This Week

This week begins with a market that is already tense. US-China trade news may help sentiment in some sectors, but rising Iran risk, oil above $107/barrel, the 10Y yield at 4.63%, mortgage rates near 7.00%+, inflation near 4%+, and rate cut odds at only 2% this year all point to a harder macro environment.

For crypto, the pressure is already visible. Bitcoin lost the $77,000 level, long liquidations passed $500 million in 60 minutes, and the 24-hour Long Squeeze reached $650 million. If Bitcoin moves toward the bottom of its ascending channel and dominance rises, altcoins may face more pressure, especially during a week with several unlocks.

The coming days will show whether markets can absorb the shock or whether higher oil, higher yields, and weaker risk appetite continue to control the direction.

This week’s market setup shows why traders need to stay careful, follow the data, and manage risk with discipline. Macro pressure, geopolitical tension, rate expectations, and crypto-specific events can all move prices quickly. Always DYOR, trade responsibly, and use proper risk management before making any decision. You can explore markets on Millionero Exchange and keep learning through the Millionero Blog.