Market Wrap: This week was defined by rate cuts, Japan’s surprise tightening, and US–China signals. On Sep 17, the US Federal Reserve cut rates by 25 bps, its first cut of 2025, with the statement tilting toward rising labor-market risks. The dot plot implied ~50 bps more easing this year, though six officials saw no further cuts in 2025, while nine projected two additional cuts next year. Notably, new Fed governor Stephen Miran, confirmed by the Senate the day before, dissented for a 50 bps cut now.

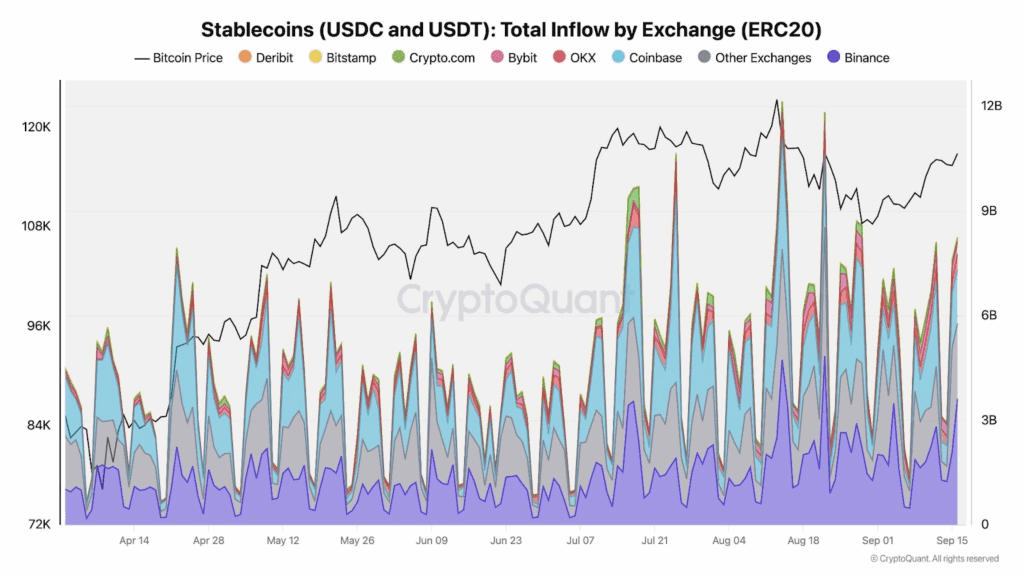

After the decision, stablecoin data showed >$2.1B of USDT/USDC flowed into exchanges, and average whale deposits jumped to $214k versus $63k in July.

Japan pulled in the other direction: the Bank of Japan voted to sell about ¥335B (~$2.4B) per year of ETFs and J-REITs. Stocks fell on the headline, and risk assets, including crypto, closed the week softer. Separately, Japan cut crypto taxes from 55% to 20%, aligning gains with stock treatment and potentially making the country a friendlier hub for digital assets.

US – China, big tech, and geopolitics

US President Trump said “stocks will perform better over time,” then added that he had a “very productive call” with China President Xi and plans reciprocal visits. Earlier in the week, reports signaled a framework agreement around TikTok talks and a broad agenda with China.

At the same time, China news was mixed: Beijing reportedly dropped an antitrust probe into Google during trade talks, but barred domestic firms from buying Nvidia chips, a move that could ripple through global AI projects.

Regulation and legislation

Market plumbing kept evolving. The SEC approved general listing standards for commodity and digital-asset ETFs, removing some case-by-case friction. It also delayed Truth Social’s BTC and ETH ETFs to Oct 8, while other products (e.g., SOL, XRP) remain under extended review.

In Congress, the House combined an anti-CBDC bill with the CLARITY market-structure bill, bundling crypto oversight and a ban on a Fed CBDC into one package headed to the Senate. Coinbase’s CEO said a comprehensive market-structure bill has a good shot after visible bipartisan backing.

In the UK, the Bank of England floated a £10k–£20k cap on individual stablecoin holdings, citing systemic risk, an approach critics see as restrictive.

Institutions, ETFs, and banks

Grayscale launched the Grayscale CoinDesk Crypto 5 ETF (ex-GDLC) one day after SEC sign-off, unusually fast versus the typical 3–6 months, offering exposure to BTC, ETH, SOL, XRP, ADA.

In Europe, Santander’s Openbank rolled out crypto trading in Germany (BTC, ETH, LTC, POL, ADA). In the Middle East, Saudi Awwal Bank partnered with Chainlink (CCIP + Runtime Environment) to accelerate on-chain finance. And MoneyGram prepared a USDC-backed app with blockchain settlement.

Corporate treasuries, government holdings, and flows

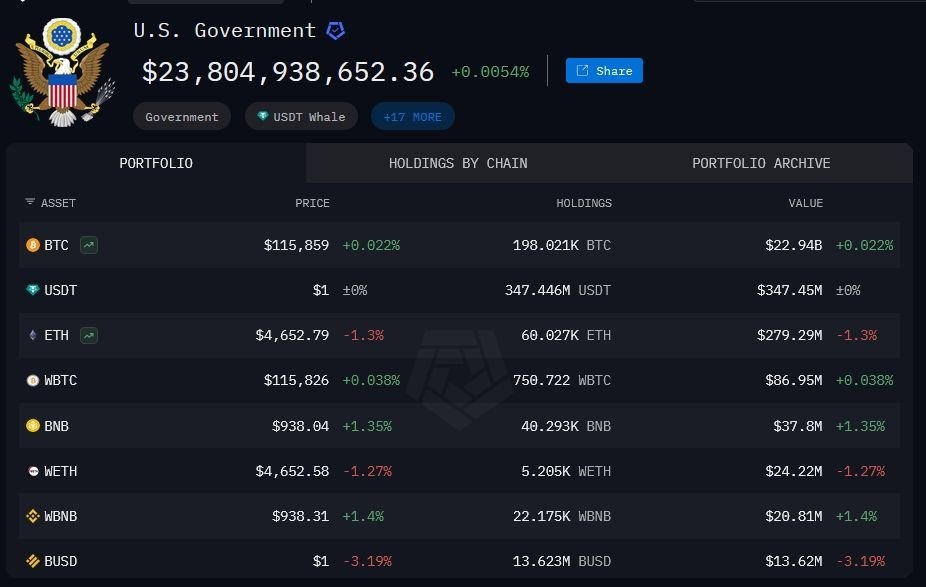

Corporate allocation kept climbing: from February to September, ETH in company treasuries surged, BTC grew steadily, and SOL saw a strong rise, clear signs of diversification beyond bitcoin. Meanwhile, US government wallets surfaced as major holders, $23.8B total, including 198,021 BTC (~$22.94B), 60,027 ETH (~$279M), 347M USDT, 750 WBTC, and 40k BNB, plus other assets.

Even so, most BTC supply still sits with private holders, keeping market power with individuals and long-term HODLers. After the Fed cut, stablecoin inflows to Exchanges and larger whale deposit sizes pointed to near-term risk appetite.

Networks, exchanges, and products

Activity across chains and venues stayed hot. Hyperliquid posted its highest daily revenue of September, and Tron led 24-hour network revenue at $1.42M.

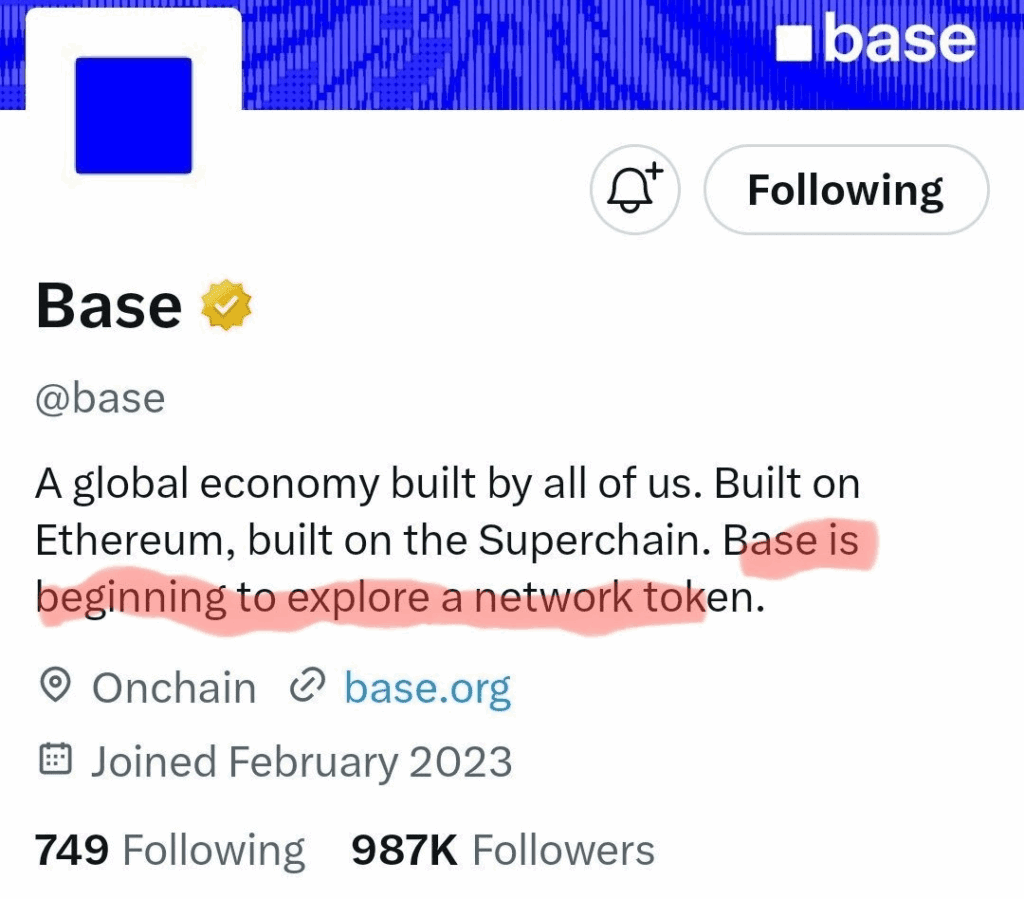

Base said it’s exploring a network token (no timeline yet). MetaMask surprised by launching mUSD, a dollar-backed stablecoin integrated into the wallet. And BNB broke $1,000, a symbolic threshold for Binance’s ecosystem coin.

On-chain metrics and usage

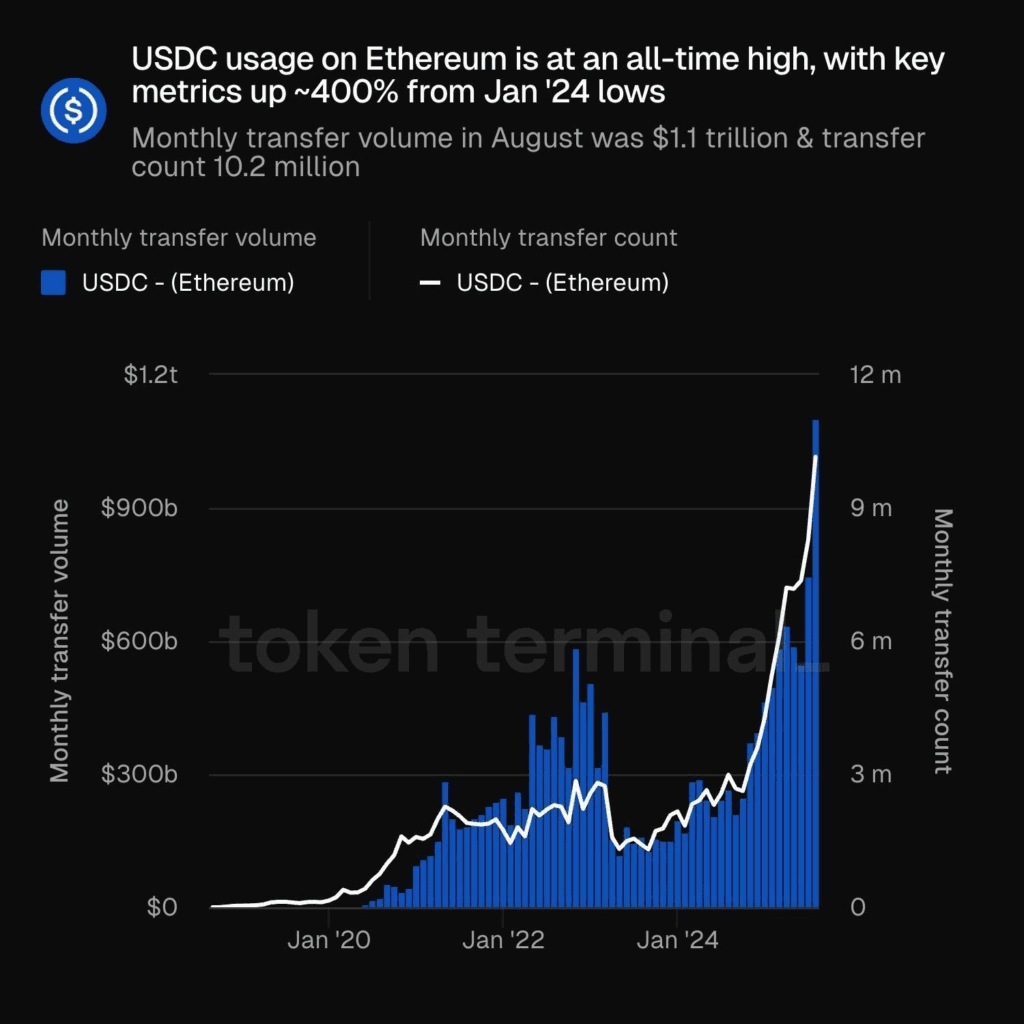

Several data points reinforced the maturing cycle. USDC usage on Ethereum hit all-time highs; since January 2024, key metrics are up ~400%, with August transfer volume at $1.1T across 10.2M transfers, quietly making USDC a key driver of Ethereum activity.

Bitcoin’s illiquid supply reached a record, with more coins moving to long-term holders. Bitcoin whales’ holdings also hit a record high.

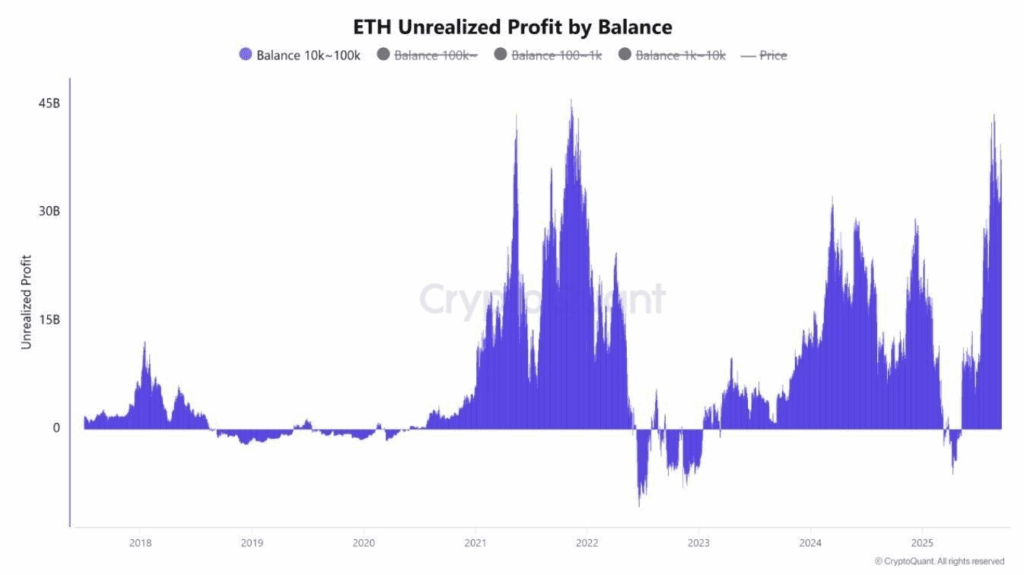

On Ethereum, medium-size whale unrealized profits climbed to levels last seen in the November 2021 peak.

Bridge flows (7d) showed inflows to Ethereum, Solana, and Base, while Arbitrum and BNB Chain saw outflows.

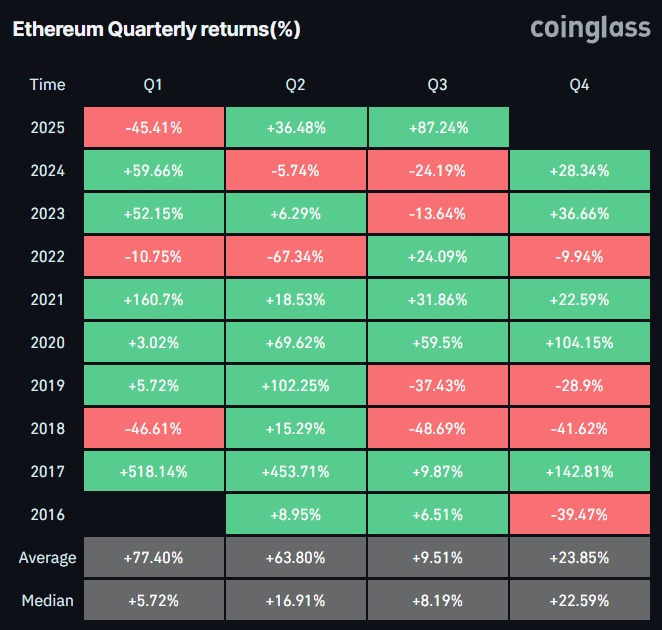

Looking broader, Ethereum appeared on track for its strongest Q3 ever, powered by network activity, staking/un-staking demand, DeFi momentum, and stablecoin growth.

Fundraising, hacks, and recoveries

Funding and risk shared the stage. FTX Recovery Trust said it’s set to disburse $1.6B by month-end, with 123–138% recovery rates for some, money that could rotate back into crypto and add Q4 liquidity.

BIO Protocol raised $6.9M led by Arthur Hayes and Maelstrom.

On Solana, Helius reportedly raised >$500M from Pantera and Summer Capital to launch a Solana-focused treasury company.

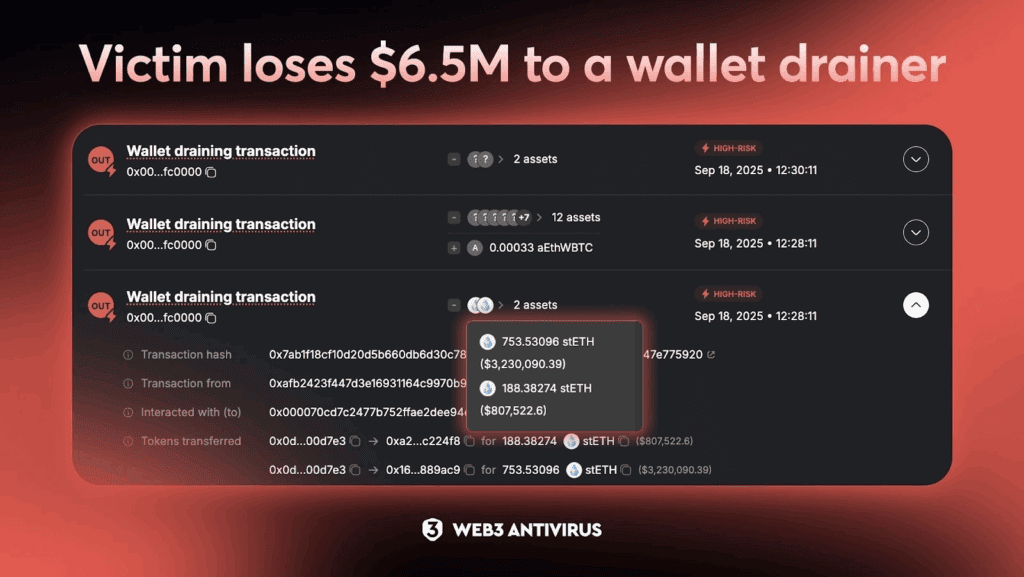

Security was a sober counterpoint: a seasoned DeFi user’s wallet was drained of ~$6.5M (including >$4M stETH), a reminder that even veterans need pre-sign protections and careful key hygiene.

Quick hits

- Trump–Xi: Trump plans to visit China, with Xi to visit the US following a “very productive call.”

- TikTok: Officials indicated a framework is in place as part of broader US–China talks.

- Nvidia: China’s ban on domestic purchases of Nvidia chips underscores tech decoupling risk.

- Market tone: Risk assets softened after the BoJ plan; crypto closed the week mixed-to-red.

Why this all matters

The net picture is a liquidity tug-of-war. The Fed started cutting into a softening labor market, while Japan is withdrawing ETF support. At the same time, USDC throughput, long-term BTC holding, and new ETF rails suggest deeper institutional and retail integration. Add in corporate diversification into ETH and SOL, government mega-wallets, and exchange/network revenue strength, and you get a market that looks structurally stronger, even as policy and geopolitics can swing week-to-week sentiment.

This content is for informational purposes only and does not constitute financial advice. Always do your own research before making any investment decisions. For more insights and analysis, visit blog.millionero.com. When you’re ready to trade, explore spot and perpetual futures on Millionero.