A tense weekend set the tone

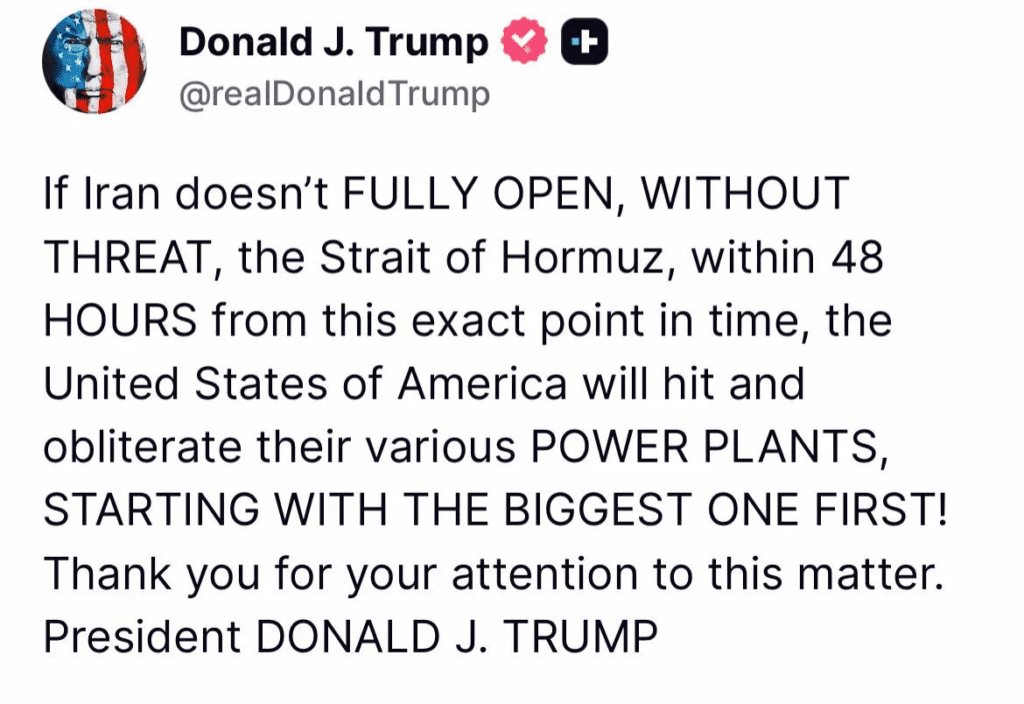

The weekend was dominated by a sharp rise in geopolitical risk. The biggest trigger was President Trump’s 48-hour deadline for Iran to fully reopen the Strait of Hormuz without threat, with a warning that the United States would otherwise begin striking Iranian power stations, starting with the largest ones. That message quickly changed the mood across markets because Hormuz is not just another waterway. It is one of the most important oil routes in the world, so any threat around it immediately hits oil, equities, bonds, and crypto at the same time. The reaction was not only financial. There was also growing concern about the humanitarian side of the escalation, especially after warnings that attacks on power infrastructure could leave millions without electricity.

Energy risk moved to the center

That tension grew further after reports of a major strike on Tehran’s electrical network, with widespread blackouts across the capital. At the same time, an Iranian military source warned Washington that any attack on Khark Island would bring a “surprise” response. That warning carried extra weight because roughly 90% of Iran’s oil exports pass through Khark Island. In other words, over the weekend the story was no longer only about military headlines. It became a story about energy security, shipping risk, and the possibility of another step higher in global economic stress.

The diplomatic angle also mattered

There was also a diplomatic development that mattered. More than 20 countries signed a joint statement condemning Iranian attacks on commercial shipping and the closure of the Strait of Hormuz, while also saying they were ready to help support safe passage through the strait. That matters because it shows the pressure on Iran is no longer only coming from Washington. It is becoming a wider international issue, and markets usually react more seriously when military risk begins to gain broader diplomatic backing.

Crypto reaction and market sentiment

Bitcoin reacted like a risk asset

Crypto reacted fast to the geopolitical shock. Bitcoin fell toward and then below $68,000 after Trump’s warning, showing that even though BTC often trades as an independent asset, it still behaves like a risk asset when global fear rises quickly. The drop was not happening in isolation either. It came during a broader market move where futures weakened and traders began preparing for a very unstable start to the week.

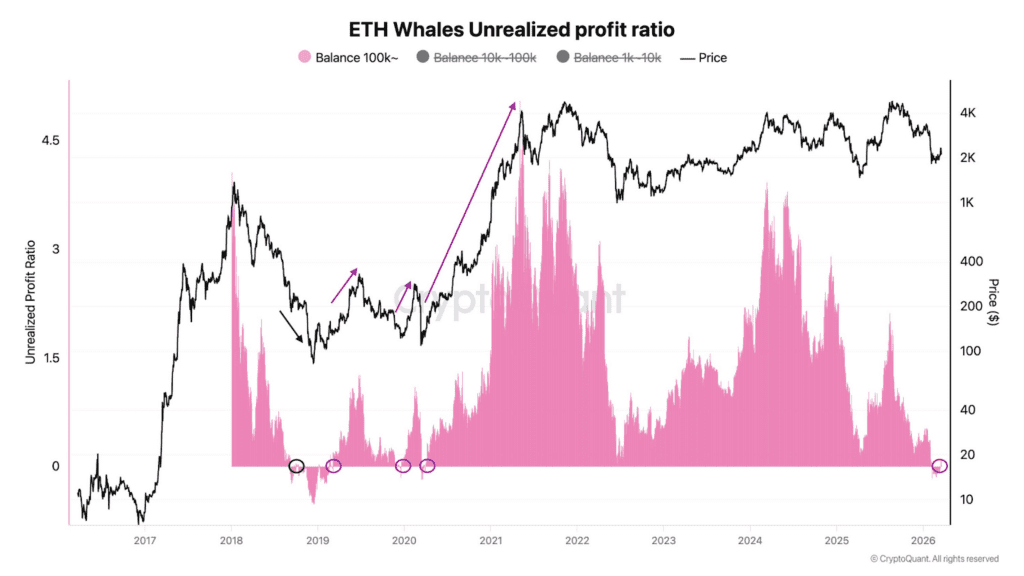

Ethereum still showed a stronger internal signal

At the same time, there were still some crypto-specific signals that prevented the picture from becoming fully bearish. One of the more notable ones was on Ethereum. Wallets holding more than 100,000 ETH moved back into positive unrealized profit territory. Historically, that shift has often been followed by gains over the next few months, and in some past cases even much larger upside over a year. That does not guarantee anything now, but it does suggest that large holders are no longer sitting in the kind of underwater position that usually limits confidence.

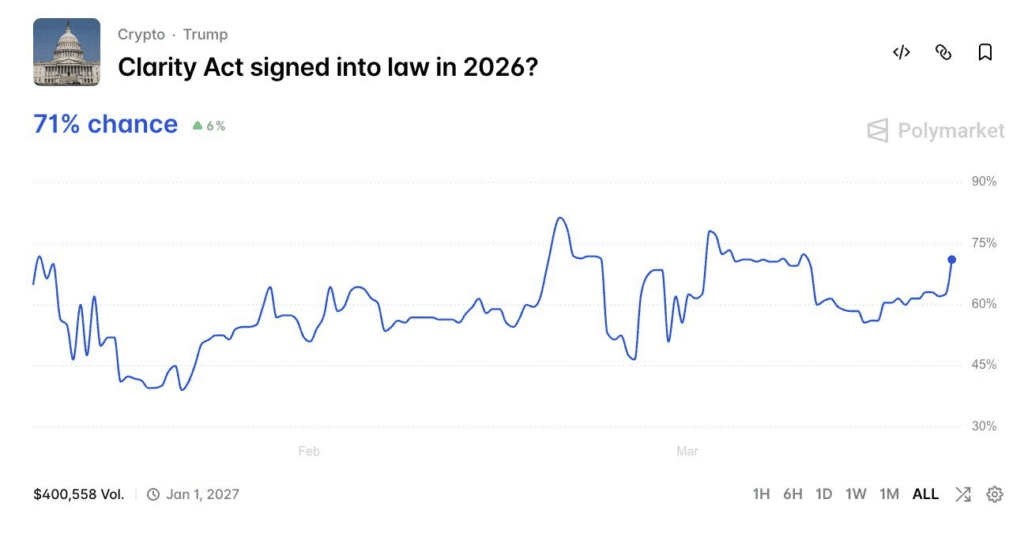

Regulation stayed in the background

There was also a legal and policy angle. Polymarket traders pushed the probability of the Clarity Act being signed in 2026 up to 71%. That does not directly move prices today, but it shows that part of the market is still looking beyond the war headlines and toward a friendlier US crypto policy environment later this year.

The industry still looks under pressure

Still, the industry also saw a more uncomfortable side over the weekend. Crypto.com, Algorand, Gemini, Messari, and OP Labs were all mentioned in a fresh wave of layoffs, in some cases cutting teams by as much as 30%. The two reasons highlighted were falling crypto prices hurting revenues and AI replacing roles that used to require full human teams. That is an important signal because it shows that even while the market talks about long-term adoption and regulation, many firms are still being forced to cut costs in the short term.

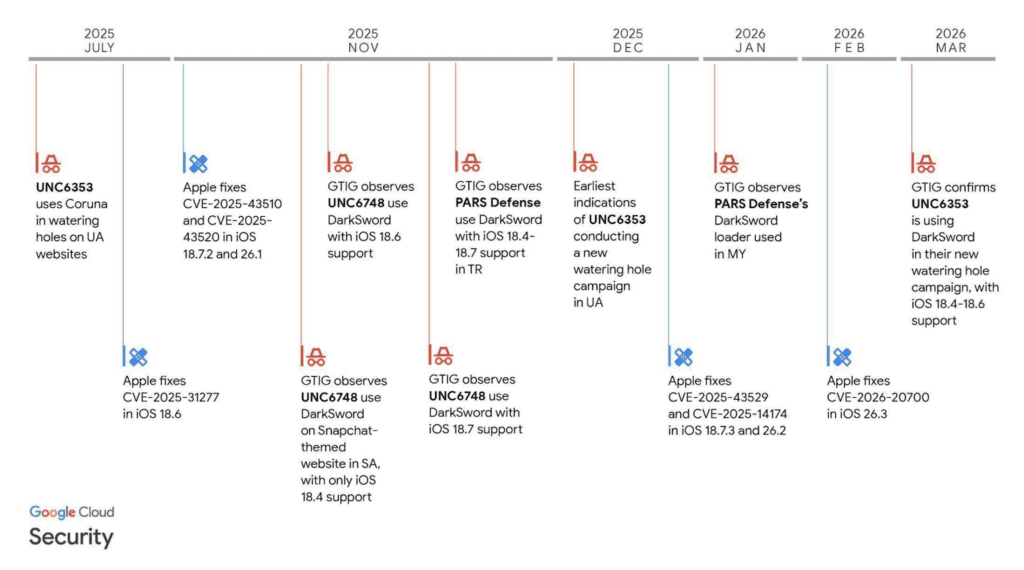

Security risk is also back in focus

Another issue traders will keep watching is security. A warning tied to Google highlighted a serious iPhone exploit called “DarkSword,” described as capable of silently stealing wallet data, passwords, and credentials simply through a malicious website. MetaMask, Phantom, Coinbase Wallet, and similar crypto wallet users were mentioned as direct targets. For the market, this is not just a tech story. It is another reminder that in stressed periods, security risk becomes even more dangerous because people are already distracted by volatility.

Monday’s open and cross-market stress

The first reaction was classic fear

As markets reopened, the first reaction was classic risk-off. US stock futures opened lower, Bitcoin extended losses, WTI crude oil jumped, Brent moved higher, and traders watched the Trump deadline count down. But what made the move strange was that gold fell instead of rising. Usually, a war headline of this scale helps gold. This time, gold dropped sharply, which made the whole market move feel unusual from the start.

Gold did not behave the way traders expected

Soon after, Gold fell below $4,350 per ounce, and within a few hours gold and silver together erased about $2 trillion in market cap. The discussion around this move centered on the possibility that a large player may have been liquidated, while rising yields, market fatigue, and pockets of illiquidity were making price gaps much bigger in both directions. By the start of the week, gold had officially entered a bear market, down 22% from its record high.

Asia felt the energy shock quickly

Asian markets reflected how serious the energy angle had become. Japan’s stock market (Nikkei) fell more than 4% on the day, and South Korea’s fell more than 6%, both linked to the worsening energy crisis. These moves matter because they show this is no longer only a US-Iran headline. It is now feeding directly into regional equity stress in Asia.

Bonds, rates, and the Fed

Bonds may matter more than oil now

One of the most important points going into this week is that oil may no longer be the only market to watch. The 10-year US Treasury yield has risen about 45 basis points since the war began on February 28, reaching 4.40%. The argument being made is simple: if the 10-year pushes back into the 4.50% to 4.60% area, that could become the real pressure point for policy and markets, just like it did during the tariff stress in April 2025.

Why this matters for the Fed

This matters for the Fed too. Higher yields tighten financial conditions on their own, even without another rate hike. So this week’s US data will not be read in a vacuum. Markets will compare every number against two things at once: first, whether the economy is slowing enough to justify future cuts, and second, whether war-driven inflation risk and rising yields keep the Fed cautious for longer.

The week ahead in US macro

What matters most this week

- Growth data

- Labor signals

- Consumer confidence

Tuesday: PMI and manufacturing data

This week starts with markets reacting to the war escalation and with attention on the CERAWeek energy conference. After that, Tuesday brings manufacturing and services PMI data along with the Richmond manufacturing survey. If PMI numbers come in strong, that could support the view that the economy is still holding up, which usually reduces the urgency for Fed cuts. But if prices stay high because of war and energy stress, strong activity data could also keep yields elevated. On the other hand, weak PMI data would support the slowdown narrative and could help revive cut expectations, though the Fed would still have to balance that against inflation risk from oil and supply disruption.

Wednesday to Friday: earnings, claims, and confidence

Wednesday brings major company earnings, which will matter because they can show whether corporate America is absorbing the pressure or starting to crack under higher costs and uncertainty. Thursday then brings jobless claims and a G7 ministers meeting. Claims are important because labor market weakness is one of the clearest ways to increase pressure for Fed easing. But again, if inflation fears remain sticky, weaker jobs data does not automatically mean faster cuts. Friday ends the week with consumer confidence. In the current environment, confidence matters because it can show whether households are being shaken more by war headlines, market volatility, or higher prices.

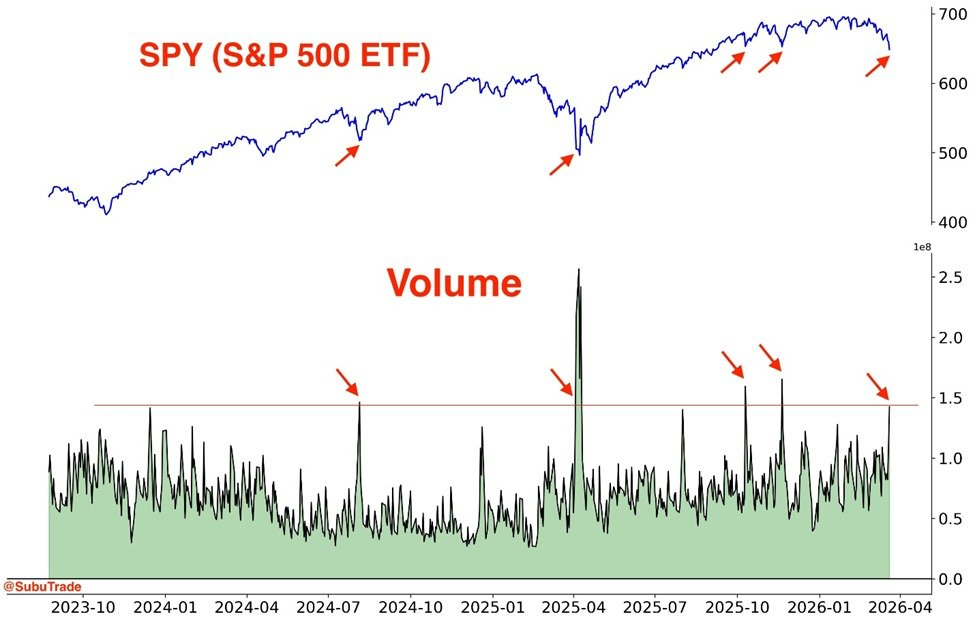

Positioning is already stretched

Another reason this week could stay volatile is positioning. SPY trading volume rose to its highest daily total of 2026 on Friday, and the session also included the biggest March triple-witching options expiry in at least 30 years, with about $5.7 trillion in options tied to US stocks, indexes, and ETFs expiring. That released a huge amount of capital back into the system. In plain terms, that means markets may now move more freely and more violently because a major options pin has just been removed.

Token unlocks

SOSO (SOSO)

Date: Mar 24

Unlock Value: 5.41M USD

% of Circulating Supply: 4.6%

Number of Tokens: 13.33M SOSO

Monad (MON)

Date: Mar 24

Unlock Value: 3.74M USD

% of Circulating Supply: 0.3%

Number of Tokens: 170M MON

Humanity (H)

Date: Mar 24

Unlock Value: 10.01M USD

% of Circulating Supply: 4.2%

Number of Tokens: 110M H

Plasma (XPL)

Date: Mar 25

Unlock Value: 8.56M USD

% of Circulating Supply: 4.0%

Number of Tokens: 89.17M XPL

Aerodrome (AERO)

Date: Mar 25

Unlock Value: 1.21M USD

% of Circulating Supply: 0.3%

Number of Tokens: 3.77M AERO

Fetch.ai (FET)

Date: Mar 27

Unlock Value: 0.72M USD

% of Circulating Supply: 0.2%

Number of Tokens: 3.20M FET

Jupiter (JUP)

Date: Mar 27

Unlock Value: 8.50M USD

% of Circulating Supply: 1.6%

Number of Tokens: 53.46M JUP

PARTI (PARTI)

Date: Mar 23 – Mar 30

Unlock Value: 8.33M USD

% of Adjusted Released Supply: 19.86%

Number of Tokens: 89.30M PARTI

RAIN (RAIN)

Date: Mar 23 – Mar 30

Unlock Value: 80.56M USD

% of Circulating Supply: 1.98%

Number of Tokens: 9.47B RAIN

SOL (SOL)

Date: Mar 23 – Mar 30

Unlock Value: 40.97M USD

% of Circulating Supply: 0.08%

Number of Tokens: 471.22K SOL

CC (CC)

Date: Mar 23 – Mar 30

Unlock Value: 27.79M USD

% of Circulating Supply: 0.50%

Number of Tokens: 191.71M CC

TRUMP (TRUMP)

Date: Mar 23 – Mar 30

Unlock Value: 20.25M USD

% of Circulating Supply: 2.72%

Number of Tokens: 6.33M TRUMP

WLD (WLD)

Date: Mar 23 – Mar 30

Unlock Value: 11.55M USD

% of Circulating Supply: 1.25%

Number of Tokens: 37.23M WLD

DOGE (DOGE)

Date: Mar 23 – Mar 30

Unlock Value: 8.76M USD

% of Circulating Supply: 0.06%

Number of Tokens: 96.56M DOGE

Final view

Where the market stands now

The weekend pushed markets into a very fragile setup. War risk is higher, oil and shipping remain central, bond yields are rising, gold is behaving in a very unusual way, Asian equities are already under pressure, and crypto is caught between macro fear and a few still-bullish internal signals. This week’s US numbers now matter even more because traders are not just asking whether growth is slowing. They are asking whether the Fed can afford to think about cuts at a time when yields, energy risk, and geopolitical stress are all rising together.

This article is for informational purposes only and does not constitute financial advice. Always do your own research before making any investment decisions. Read more market updates on the Millionero blog and trade on Millionero.