Meteora is a DeFi platform on Solana that tries to be the “smart liquidity layer” for the whole ecosystem. It runs advanced liquidity pools called DLMMs (Dynamic Liquidity Market Makers) that:

- focus liquidity in active price ranges

- adjust fees when volatility changes

This design makes trading more efficient and helps liquidity providers (LPs) earn more from the same amount of capital. On top of that, Meteora has Dynamic Vaults that lend idle assets to lending protocols like Solend or Marginfi to earn extra yield. It also offers anti-bot tools and launch features for new tokens, which turned it into a key venue for memecoins and new projects on Solana.

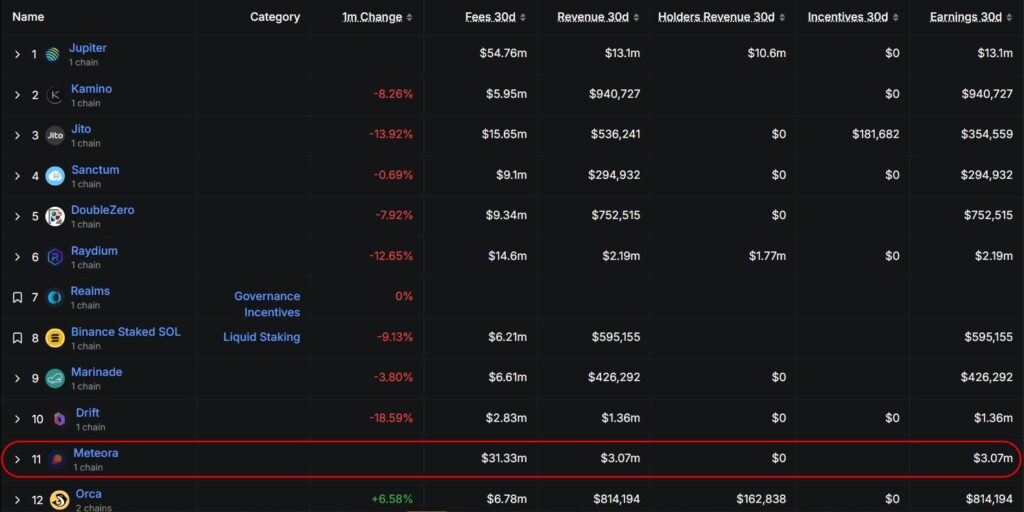

By December 2025, Meteora had processed over $200 billion in volume and held around $620 million in TVL, with strong integration into Jupiter, Solana’s main swap aggregator.

On the product side, Meteora looks strong. The problem has been the MET token.

A Fair Launch… With a Heavy Hangover

The MET token launched in late October 2025 with a clear “community-first” story:

- 1 billion total supply

- 48% released to the community at TGE (airdrops, LP rewards, etc.)

- 52% locked with long-term vesting

- 18% to the team vesting linearly over 6 years

- No new inflation or emissions. Value was supposed to come from real protocol fees, not token printing.

On paper, this looked fair. In practice, the market reacted differently.

MET briefly hit an all-time high around $0.62 on the first day of listing, then slid more than 66% and moved near all-time lows around $0.2 by mid-December 2025. Why?

- Massive upfront supply

Almost half the supply hit the market at once. Many people who got airdrops (for example, old Mercurial Finance holders and LPs) took profit. That created strong sell pressure from day one, while ~22 million MET per quarter kept unlocking from team and reserves. - Weak value link at first

The idea was “fees will support MET,” but for a long time MET holders did not see clear, direct yield or fee sharing. That made it hard to justify holding the token on fundamentals instead of just speculation. - History and trust

Meteora is the successor to Mercurial, which was hit hard by the FTX collapse. Some investors still carried that memory and stayed cautious about the new token.

So you ended up with high supply, weak early utility, and serious competition for capital inside Solana DeFi. Unsurprisingly, price suffered.

The “Met Dhabi” Turn: Points and Buybacks

At the Met Dhabi event on December 10, 2025, Meteora’s team tried to fix the MET story with a major tokenomics update. Two new pillars were announced: Comet Points and aggressive buybacks.

1. Comet Points. A Loyalty Layer

Comet Points are non-tradable reward points you earn by:

- staking MET

- using Meteora’s products

These points can be used for future perks, such as:

- access to airdrops and presales

- merch and a rewards store

- paying for LP coaching and other services

The goal is to build a “consumer economy” around Meteora: if you are a loyal user and holder, you get special treatment and ongoing benefits. Over time, the team plans to expand what Comet Points can do, based on community feedback.

In theory, this can:

- push more people to stake MET

- reduce circulating supply

- keep users active on the platform

But the hard truth is that point systems have not usually driven big price moves in crypto unless the perks are extremely valuable and very clear. They help with engagement, not necessarily with valuation.

2. $10 Million Buybacks. Real Money on the Table

The second move is much more direct: revenue-funded buybacks.

- In Q4 2025, Meteora spent $10 million USDC, about 88% of that quarter’s revenue, to buy MET from the open market.

- This removed about 2.3% of total supply in one quarter.

The plan is to keep doing discretionary buybacks from a public wallet, depending on revenues and business needs. At current unlock rates, that 2.3% per quarter roughly matches the tokens that vest each quarter, so net supply may stay flat instead of growing.

This is a big shift in message: Meteora is clearly saying, “We will use real protocol income to support the token.”

However, there are two important caveats:

- The buyback size is not guaranteed; it’s discretionary, not coded into the protocol.

- A flat supply is healthier than rising supply, but it does not automatically create scarcity or a big re-rating. For that, revenues (and thus buybacks) must grow a lot, or more demand must appear.

Is This Enough to Save MET?

Taken together, Comet Points and buybacks are strong improvements versus the original token design:

- holders now see active steps to tie MET to real usage and cash flow

- the team is clearly willing to spend serious money (88% of quarterly revenue) to support the token

Still, the effect will likely be gradual, not explosive.

- Comet Points are good for long-term community building, but they are indirect. Their impact depends on how valuable the perks become in practice.

- Buybacks are the more powerful tool, but at current scale they mostly cancel dilution instead of creating deep scarcity.

So MET is now in a “prove it” phase. The tokenomics are no longer obviously broken, but investors will want to see:

- steady or rising protocol revenue

- consistent buybacks quarter after quarter

- a visible drop in circulating supply over time

- clear, high-value uses for Comet Points

If those things happen, the market can slowly re-rate MET from “disappointing” to “real yield DeFi token on Solana.” If not, sentiment may stay lukewarm.

How Meteora Stacks Up Against Solana Rivals

To understand MET’s challenge, we need to look at competitors inside Solana DeFi.

- Raydium (RAY): The original Solana DEX giant, with deep liquidity and past fee-sharing and buybacks. Still strong in volume, but its tokenomics are seen as more “steady” than exciting.

- Orca (ORCA): User-friendly DEX with concentrated liquidity and fee sharing. Reliable but has not matched the hype or scale of newer memecoin platforms.

- Jupiter: The main aggregator, not a token competitor, but a key partner since it routes flow through Meteora’s pools.

- Pump.fun (PUMP): The most aggressive benchmark. Pump.fun sends 100% of its daily revenue to buy back PUMP. In only five months, its buybacks removed around 13.8% of supply and over $200 million worth of tokens, making it a “revenue machine” in the eyes of investors.

Compared to PUMP’s fully automated, daily, all-revenue buybacks, Meteora’s $10M per quarter, discretionary program looks modest. That is why many investors currently see PUMP as having stronger value accrual.

For MET to stand out, Meteora must:

- keep growing its volume and fees

- show that buybacks are consistent and maybe increasing

- use its more advanced liquidity tech (DLMM, vaults, anti-bot tools) to win and hold market share, not just spike during hype periods

The Bottom Line

Meteora has built real infrastructure on Solana and already proved product-market fit as a dynamic liquidity layer. The weak link has been the token, not the tech.

The Met Dhabi tokenomics shift is a serious attempt to fix that link:

- Comet Points try to reward loyal users and stakers

- Revenue-funded buybacks try to align MET with actual cash flow

These changes do not guarantee a price recovery, but they do give MET a clearer path to becoming a proper value-accruing DeFi token. From here, everything depends on execution: revenue growth, sustained buybacks, and meaningful rewards that make people want to hold and use MET over the long run.

This article is not financial advice. It is meant to help you understand the market and think more clearly, not to tell you what to buy or sell.

Always do your own research (DYOR) and make sure any decision fits your risk level and your personal situation. You can find more simple guides and deep market explainers on blog.millionero.com.

When you feel ready and informed, you can trade spot and futures on Millionero in a careful, step-by-step way, never with money you cannot afford to lose.