Nasdaq got SEC approval on March 18, 2026 to let some shares trade in tokenized form under rule change SR-NASDAQ-2025-072. At first look, this sounds huge. Many headlines make it sound like Wall Street is about to jump fully on-chain. But that is not what this order does. What the SEC approved is real and important, yet it is also narrow, slow, and very controlled.

What the SEC actually approved

This is not a full Nasdaq blockchain launch. Nasdaq can only do this inside the DTC tokenization pilot. DTC, the Depository Trust Company, is the key part of the whole setup. The SEC staff gave DTC a no-action letter for that pilot on December 11, 2025, and Nasdaq’s new rule works inside that pilot, not outside it. In simple words, if DTC’s pilot and systems are not there, this Nasdaq plan does not move at all.

There is also no launch date yet. The SEC order says Nasdaq’s rule only becomes active once DTC finishes the needed post-trade and settlement setup. After that, Nasdaq still has to give members an Equity Trader Alert at least 30 calendar days before tokenized trading starts. So the approval is here, but the market is not going live tomorrow.

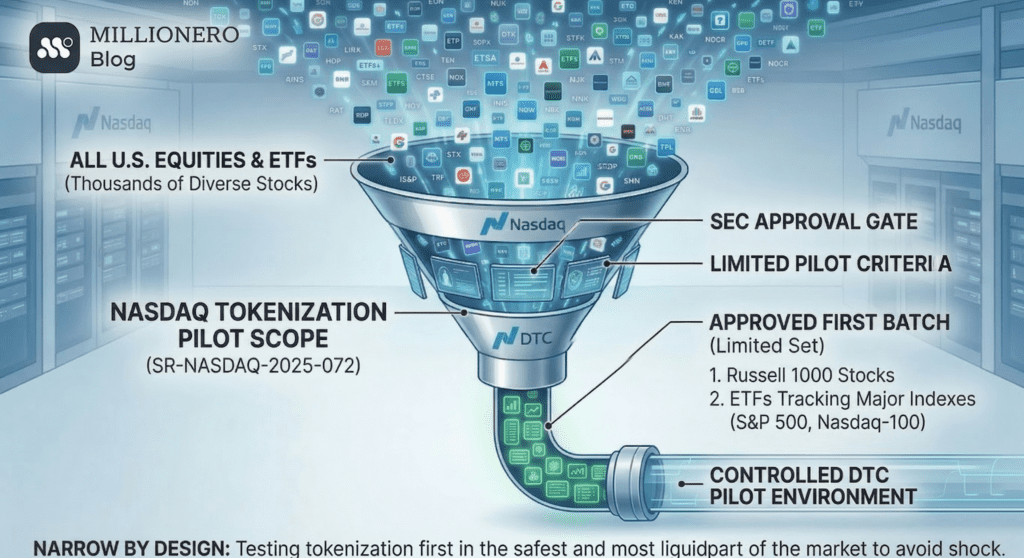

Which shares can be tokenized

The first batch is very limited. The rule only covers Russell 1000 stocks and ETFs that track major indexes like the S&P 500 and Nasdaq-100. Nasdaq will publish the list of names that qualify. This means the launch set is narrow by design. It is not a free-for-all where any stock can suddenly become tokenized.

That narrow list matters because it shows the real goal here. The SEC and Nasdaq are trying to test tokenization in the safest and most liquid part of the market first. This is a pilot built to avoid shock, not a big break from the system.

A tokenized share is still the same share

This may be the most important point. A tokenized share in this plan must be fully the same as the normal share. It must have the same CUSIP, the same ticker, and the same rights. That includes things like dividends, voting, and a claim on assets if a firm is closed down. It also has to trade on the same order book and get the same execution priority as the normal version. So there is no second market with a second price.

This is why the news is more quiet than loud. The change is not about making a new type of share with new rights. It is about changing the form of the record for some trades, while keeping the share itself the same inside the normal market system.

How the trade will actually work

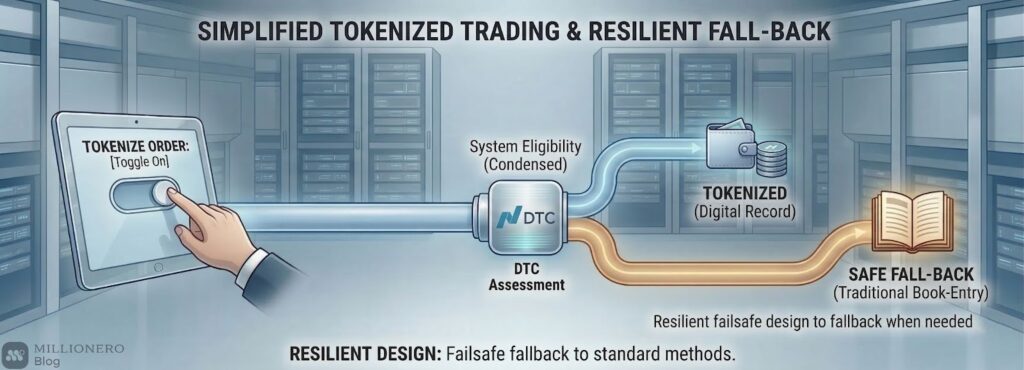

Only certain firms can even try to use tokenized settlement. The SEC order says DTC Eligible Participants can choose tokenized handling by adding a tokenization flag when they enter an order. Nasdaq then passes that choice to DTC after the trade.

But Nasdaq’s own systems will not check in advance if the firm is allowed, if the stock is allowed, or if the wallet and blockchain match DTC’s pilot rules. If any of that fails, the trade does not break. It simply settles in the normal, non-tokenized way. That is a very big detail because it shows this setup is built to fall back to the old system when needed.

Retail users also do not really press a button and choose this by themselves. In practice, the choice sits with the broker or market firm that is part of DTC’s pilot. DTC mints the token and sends it to a Registered Wallet tied to that participant. DTC’s letter also says a firm may set up a wallet for a customer, but during the pilot DTC only recognizes the participant as the holder on its books.

What does not change

A lot of the hype around tokenized stocks talks about instant settlement, round-the-clock trading, and a whole new market shape. None of that is part of this approval. The SEC order says trades handled by DTC in tokenized form would still settle on a T+1 basis. So this is not 24/7 trading and not instant settlement. The blockchain part here is mainly about the digital form of the holding record after the normal trade process.

Almost all core market rules also stay the same. Nasdaq says order types, routing, trading sessions, opening and closing crosses, connectivity, fee schedule, market data, CAT reporting, and surveillance stay in place. Market surveillance would still use the same data and stay visible to Nasdaq and FINRA. In other words, the whole thing remains inside the current U.S. market frame.

The SEC also made clear that tokenized securities in this plan are still under the same federal securities law and investor protection rules. This was not a loophole or a side door. The order came only after public comments, a longer review, and two amendments to Nasdaq’s filing.

Even corporate actions can send tokens back to normal form

Another small but very telling detail is that tokenized shares may have to go back into normal book-entry form for some events. DTC says a participant may need to give a de-tokenization instruction, or DTC may need to force that move, in order to handle things like a distribution, a replacement security, or other corporate action steps. DTC says it would try to give notice first where it can.

This again shows the truth of the pilot. The rights are the same on paper, but the operating flow is still tightly managed by DTC. The token is not a free-floating object outside the system. It stays under a very watched structure with approved wallets and reversal tools.

Why this still matters

Even with all these limits, this is still a big step. The real change is not that crypto is taking over Wall Street in one day. The real change is that Wall Street is testing how tokenization can fit inside the regulated system without breaking the market it already has. That may end up being more important than the louder dream of “everything on-chain now.”

It also matters that Nasdaq has said this is only one method of tokenization. If it wants to do other kinds later, including non-fungible structures, it would need new filings. That means this order should be read as a first lane, not the whole road.

One more thing: Nasdaq’s earlier March 2026 work with Kraken on tokenization is a different move. That partnership is about wider tokenization infrastructure and global distribution ideas. This SEC order is the much narrower DTC-pilot rule for trading and settling certain U.S. shares in tokenized form. They are linked by theme, but they are not the same thing.

Final take

So yes, this is historic. But it is historic in a calm way. Nasdaq did not get approval to blow up the old market and replace it with a crypto market. It got approval to test a small tokenized layer for a limited set of shares, through DTC, under the same rules, with the same rights, and with the old system still there as the backup. That is why this matters. It is not a jump. It is a bridge.

This article is for informational purposes only and should not be taken as financial or investment advice. Always do your own research before making any trading decision. If you want to explore the crypto market, trade on Millionero.