The week was shaped by flows, money stepped back

The cleanest signal this week was not a chart pattern. It was capital moving out.

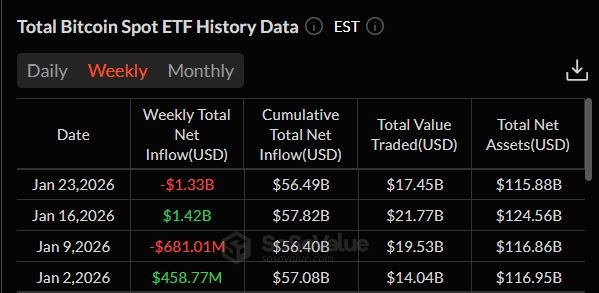

Across the week, Bitcoin ETF flow was -$1.33B, and Ethereum ETF flow was -$611M. Over a shorter window inside the week, the last 3 days alone saw about $1.58B leave Bitcoin ETFs, with big names like BlackRock and Fidelity leading the outflows. The message was simple: institutions did not want maximum exposure while headlines and rates were both unstable.

This kind of flow does not “kill” a bull market by itself, but it changes the tone. When ETFs are net sellers, rallies become harder, bounces get sold faster, and traders start treating every pump as temporary until the flow picture improves.

Altcoins stayed in a deep drawdown. “Survival mode” is real

A major theme this week was that altcoins have been in a bear market since late 2024, and 2025 did not fix it. One high-level framing was brutal but clear:

- Bitcoin was down about 6% (yearly frame),

- while altcoins saw an average drawdown around 79%.

Whether someone agrees with the exact numbers or not, the feeling matches the tape: in many portfolios, it’s been “BTC holds up, alts bleed.”

That gap matters because it changes behavior. When people feel burned in alts, they stop buying “stories” and start buying liquidity. That often pushes attention back toward BTC, majors, and anything with real depth.

Panic hit fast and liquidation pressure did the rest

Mid-week, the market had a true risk-off moment: stocks lost more than $1.3T in value, BTC dropped under $87,000, and crypto liquidations went over $1B, with a heavy share coming from Longs (including a burst of about $360M in one hour).

That matters because it wasn’t just price falling. It was forced selling. In those moments, the market is not “choosing” to sell, it is being made to sell.

At the same time, there was also a big psychological layer: a lot of traders believed this was the kind of shock that gets followed by a political “tone shift” and a bounce. And that idea actually became part of the market narrative: pressure first, then negotiation, then relief.

Bonds and rates kept haunting everything in the background

While crypto was moving, the bond market was still the shadow driver.

The US 10Y yield hit 4.30%, the first time it reached that level since September 2. The logic was simple: when yields jump, financial conditions tighten, and risk assets feel it quickly.

At the same time, Japan’s bond market looked extreme: the 40-year JGB yield moved above ~3.87% (record) and 30-year hit ~3.61% (also record) in the market notes. Even when crypto traders don’t watch JGBs, global funds do. When Japan’s rates shift sharply, it can leak into German yields, French yields, and US yields, and that can ripple into every risk market.

On inflation, another narrative showed up: Truflation was cited around 1.2%, and the argument was that deflation risk may now be bigger than inflation risk, pushing the idea that the Fed should cut aggressively. Whether or not that call is right, the point is that the market is already fighting about the next regime: “Do we get cuts because growth slows, or do we stay tight because politics and supply shocks keep pressure alive?”

Politics became a market variable again. Greenland was the spark

This week had a strong “policy headline whiplash” vibe.

The Greenland topic wasn’t just a meme. It turned into a chain reaction: tensions with Europe, tariff threats, and then sudden de-escalation. At one point, there was a shift where the idea of 10% tariffs on the EU for Feb 1 was walked back in the context of a framework for a future Greenland-related deal, and markets reacted like a spring releasing pressure: US stocks added roughly $700B in a session, gold and silver pulled back, and Bitcoin reclaimed $90,000 during the broader rebound.

At the same time, the bigger takeaway was uncomfortable: policy headlines are now moving markets faster than almost anything else, and that makes volatility feel “normal,” not special.

Europe did not stay quiet in the narrative. There was talk of the EU preparing a response package up to $100B, and France’s President Emmanuel Macron was linked to pushing Europe’s strongest trade tool the anti-coercion instrument, a tool described as something the EU has never used before. On the US side, Trump-style escalation stayed on the table, including a very aggressive-sounding threat of 200% tariffs on French wine and champagne.

There was also a strange diplomatic flavor: a reported private message from Macron, followed by talk of a Switzerland meeting involving a wide set of countries. In short: escalation and diplomacy started to mix, and markets had to price both at the same time.

One more political layer added to the volatility stack: reporting suggesting the US was actively seeking regime change in Cuba before the end of the year. Even if traders don’t trade Cuba, they trade what it represents: unpredictable geopolitical risk.

The US is signaling “structure” for crypto but banks want their rules too

The regulatory tone in the US looked like it was shifting.

A notable sign was that the SEC and CFTC planned a joint event on Tuesday to highlight coordination and “regulatory harmony,” with messaging that innovation should root inside the US. That is a different vibe than pure enforcement-first seasons, and markets notice these tone changes.

At the same time, politics and lobbying showed up clearly around stablecoins. The US banking lobby was framed as making stopping stablecoin yields a top priority for 2026, right as Congress tries to pass market structure legislation before the midterm cycle heats up. The conflict is straightforward: stablecoins that pay yield can look like a competing bank product, and banks tend to protect their model.

On the legislation side, there was a strong expectation that a US market structure bill (often called CLARITY) could move again, possibly within about a month, after delays and internal industry disagreements. The “bridge” narrative also mattered: Coinbase was positioned as talking with banks and exploring ideas that support community banks, which signals a more realistic strategy, not “replace banks,” but integrate with them.

Institutional infra kept growing: custody, IPOs, and derivatives

Even in a rough week, the “infrastructure” story kept moving.

- Ledger was discussed as exploring a possible IPO in New York at a valuation above $4B, which shows that crypto custody is being treated like serious financial infrastructure.

- Nasdaq filed to remove position limits on options tied to Bitcoin and Ethereum ETFs. That sounds technical, but it matters: fewer limits can mean deeper derivatives markets, more institutional activity, and more ways to hedge (or speculate) at size.

All of this supports a bigger theme: crypto is not just “coins.” It is becoming a market layer inside traditional finance, even while the coins themselves stay volatile.

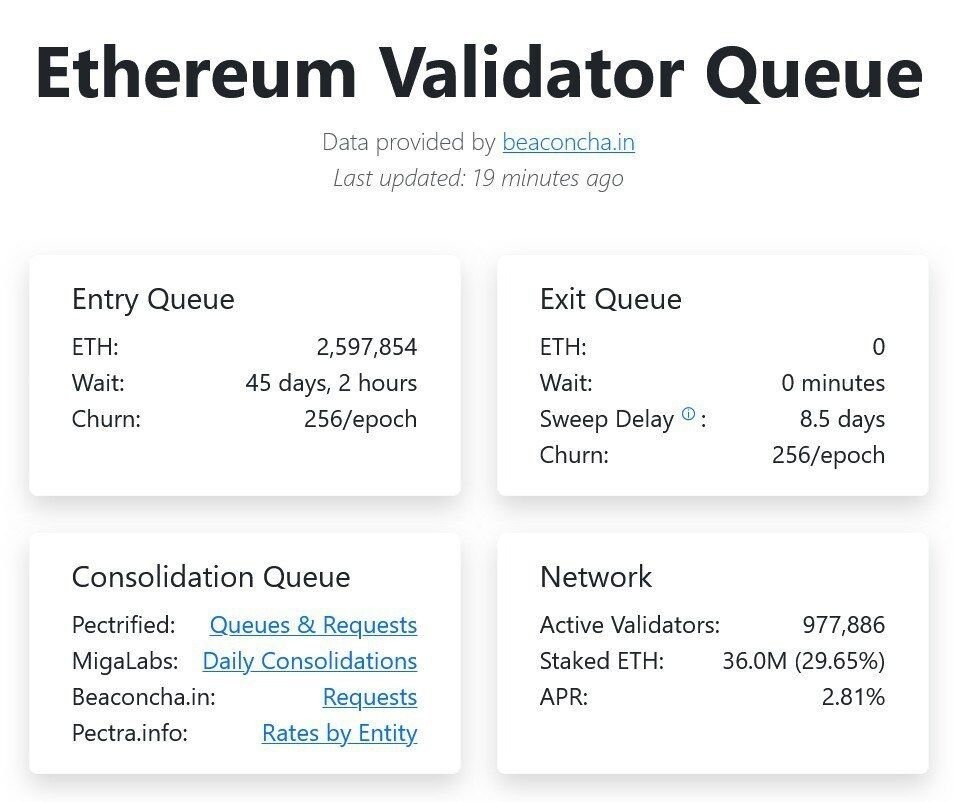

Ethereum had a quiet but important shift: staking demand returned

Ethereum’s internal supply mechanics got attention this week.

One of the more striking data points was that the unstaking queue went to zero, while the staking entry queue jumped to about 2.6M ETH, the highest since July 2023. That suggests renewed appetite to lock ETH for yield/security, or at least less urgency to exit.

On top of that, BitMine added 171,264 ETH to staking, worth roughly $503.2M, taking its total staked Ethereum value to around $5.71B. That is a big vote for Ethereum’s “bond-like” role inside crypto: an asset that can be held for network yield, not just traded.

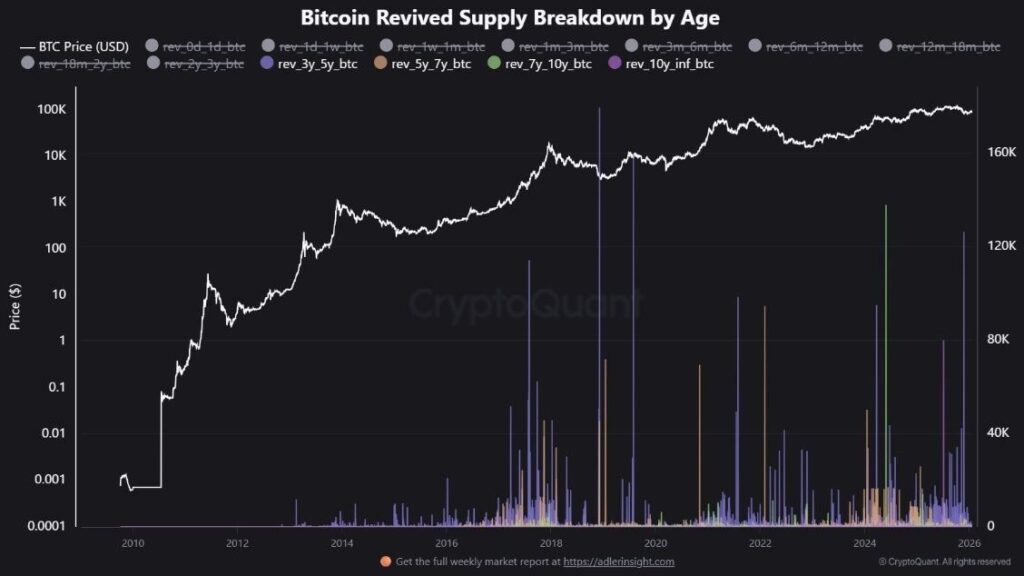

Ownership is rotating: whales steady, retail shaking out

A key long-cycle theme this week was distribution and re-accumulation.

Data framing suggested that 2024–2025 saw the largest release of long-term BTC supply in history, meaning older holders let go, and newer holders absorbed. That kind of transfer does not remove scarcity, it changes hands, and those transitions often mark important cycle phases.

In parallel, the message was that retail was exiting while whales kept accumulating on a monthly basis, even with geopolitical risk rising. That widening gap is classic: smaller players react to fear first, bigger players often react to price and liquidity.

Another data point fit the same idea: institutions and governments were said to now hold about 10.2% of total BTC supply (roughly 5.5% public companies, 1.45% private companies, 3.25% governments). That is a structural shift, because it means more BTC is sitting in sticky hands.

Sentiment got extreme in pockets and “risk/reward” started to look interesting

While people felt stressed, some indicators started hinting at “better forward odds.”

A Sharpe-based indicator (cited to CryptoQuant) was described as hitting levels historically seen near major bottoms. The key nuance was also stated clearly: it doesn’t call the exact bottom, but it can show when risk/reward resets to levels that often come before big moves.

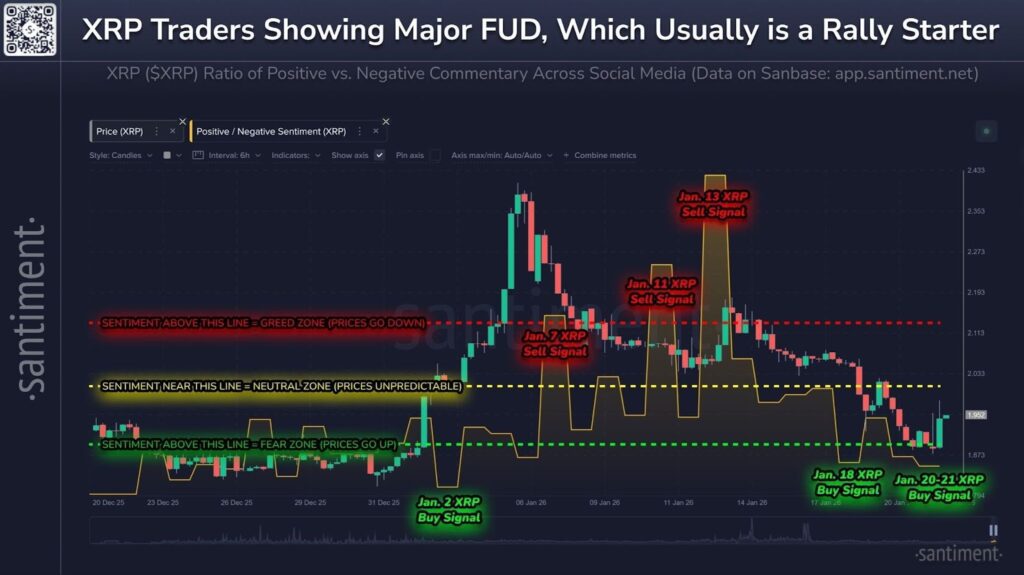

Specific assets also showed stress. XRP was said to enter Extreme Fear after a drop around 19% since January 5, based on a Santiment framing. These pockets of fear matter because they can become fuel for sharp bounces or they can become proof that the market still needs time.

A prediction market angle also captured the mood: Polymarket odds for BTC reaching $100,000 in January dropped to around 25%, basically the crowd admitting, “maybe not this month.”

Perps and exchange competition stayed brutal and fast

Crypto still trades like crypto: leadership changes quickly.

There was a note that Hyperliquid regained the top spot in perps volume and Open Interest, after activity on Lighter Perp Dex cooled during an airdrop period. This matters because it shows how traders chase best liquidity + best execution, not brand names.

Safety and trust: the hidden cost of hacks

One of the most practical reminders this week was about trust damage.

A widely repeated estimate was that about 80% of crypto projects don’t recover after major hacks, not because the money can’t be replaced, but because confidence breaks. In a week where flows were already negative and risk appetite was already fragile, this kind of reminder makes people even more selective.

Gold came back into the conversation as a hedge

While crypto fought volatility and politics, the old hedge stayed relevant. Goldman Sachs raised its end-2026 gold target to $5,400/oz (from $4,900), reflecting the idea that global risk, geopolitics, and uncertain policy can keep demand for hedges strong.

That’s important for crypto too: when gold gets bid hard, it often signals the market is paying for protection, not chasing upside.

The week in one sentence

This week looked like a market caught between two forces: short-term fear driven by yields and politics, and long-term structure driven by regulation, institutional plumbing, and ownership moving into bigger hands.

This article is not financial advice. Please do your own research (DYOR). You can start your DYOR at blog.millionero.com. When you’re ready, you can trade on Millionero.