This past week in crypto sat between two forces:stress in traditional finance and global liquidity, and

clear, sometimes aggressive, adoption of Bitcoin and other digital assets by institutions, companies, and even governments.

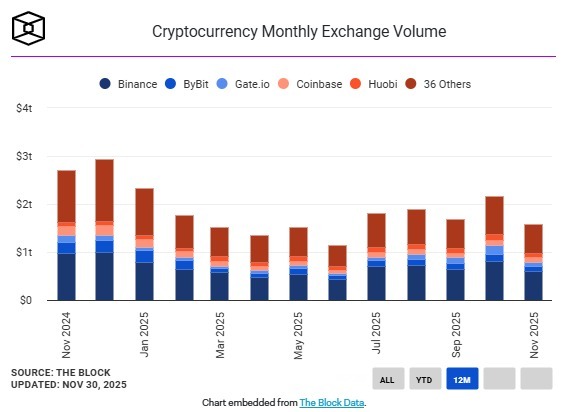

Bitcoin ETFs saw net outflows again. After last week’s +$70 million in net inflows, this week flipped back to about –$87 million. That is a negative signal, but it is still much less brutal than the heavy outflow weeks we saw recently. At the same time, spot trading volumes in November fell to $1.59 trillion, the lowest since June, showing that the market is quiet and cautious.

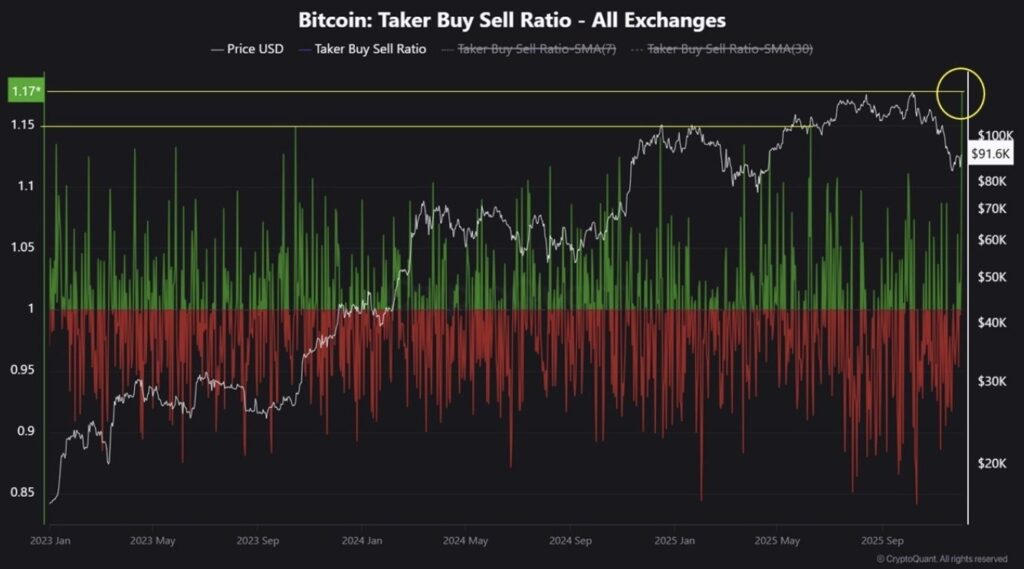

Yet on-chain and structural data tell a different story. The Market Buy/Sell Ratio hit its highest level since 2023, meaning buyers are clearly dominating sellers. Analysts note this kind of imbalance often appears in early or mid expansion phases, when long-term liquidity and structural inflows are starting to build instead of shrinking. So we have low volumes, but the flows that do exist are tilted to the buy side.

This tension, between short-term caution and long-term accumulation, runs through almost everything that happened this week.

Macro & Central Banks: Inflation Cools, Liquidity Gets Weird

On the macro side, the key inflation metric in the U.S., Core PCE, came in slightly softer than expected:

- 2.8% year-on-year vs expectations of 2.9%

- 0.2% month-on-month, exactly in line with forecasts

This was not a big surprise, but it confirms that inflation is still slowing down gradually. That gives risk assets, including crypto, a bit more room to breathe and keeps pressure on the Federal Reserve slowly moving lower.

U.S. jobless claims also came in stronger than expected:

- Previous: 216,000

- Expected: 220,000

- Actual: 191,000

This is positive for the U.S. dollar, because it shows the labor market is still strong. A strong dollar usually puts some pressure on risk assets, but in this case it stands next to other signals pointing toward easing financial conditions.

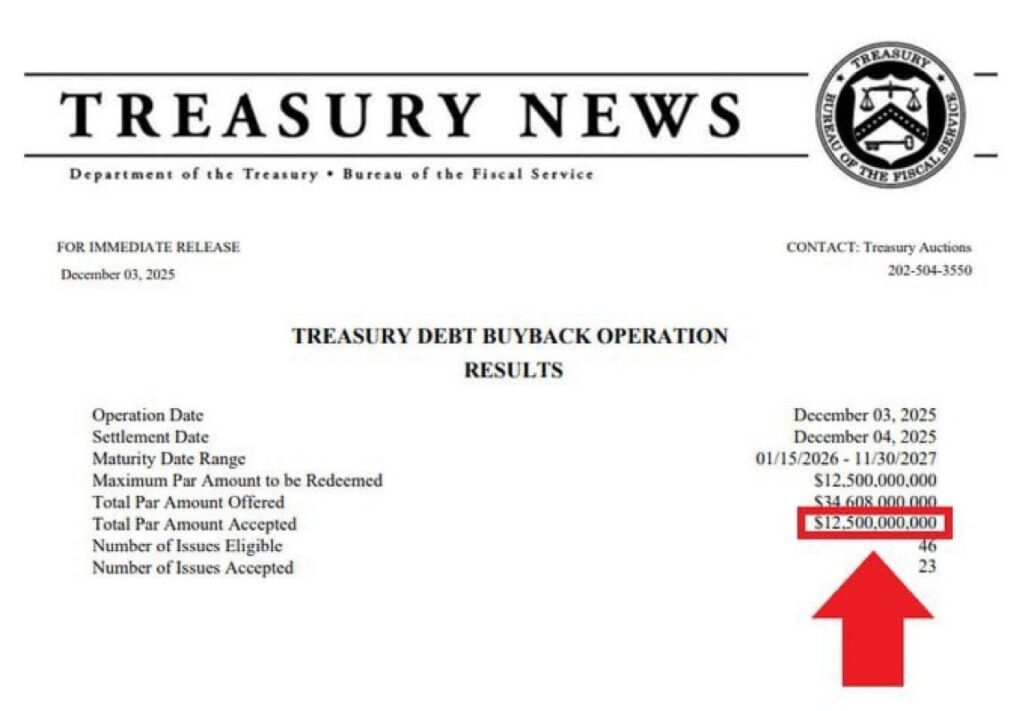

The U.S. Treasury executed the largest debt buyback in its history, repurchasing $12.5 billion of bonds on December 3, beating the prior record of $10 billion from June 2025. This can affect liquidity, bond prices, and expectations for future fiscal policy.

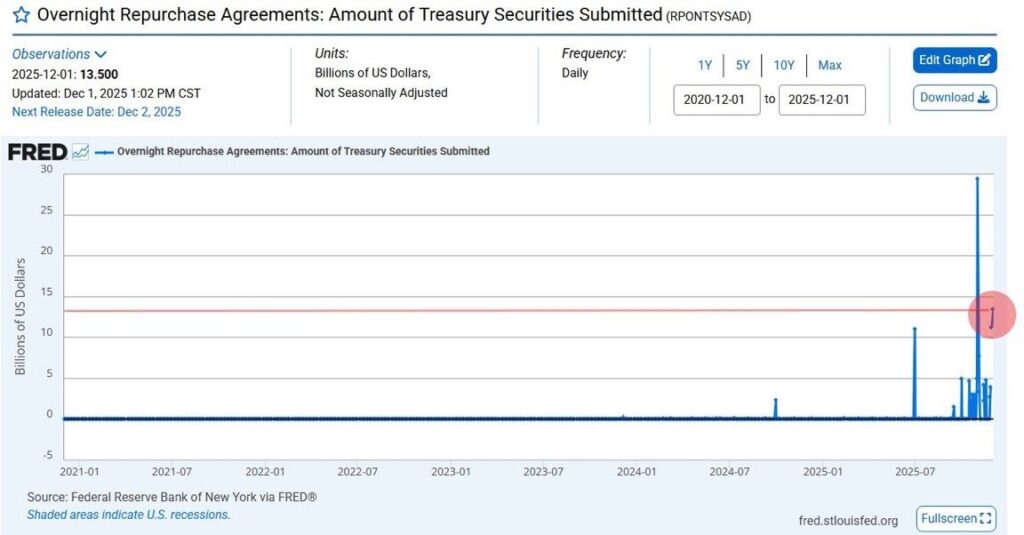

At the same time, the Federal Reserve injected $13.5 billion into the banking system via overnight repo operations, the second-largest repo injection since COVID and even bigger than levels seen in the dot-com bubble. Repo is basically a very short-term loan where banks give bonds to the Fed, get cash, then pay it back with a small interest the next day. It is a way to add liquidity quickly without saying “we are printing money.” Rising repo use often signals stress in the banking system, but it also means fresh cash entering markets in the short term, often supportive for risk assets like crypto.

Outside the U.S., Japan was also in the spotlight twice:

- The Japanese government bond (JGB) market saw a weak auction, putting pressure on bonds and global liquidity, and reducing risk appetite in general. This weighed on crypto sentiment in the short term.

- At the same time, Japan announced a plan to cut the tax on Bitcoin and crypto trading to 20%, a major pro-crypto policy that could invite more investors and speed up adoption inside the country.

Some analysts argue that stress in bond markets, and weakening trust in government debt, actually strengthens Bitcoin’s “Store of Value” narrative over the long run, especially when bond yields become volatile and governments look less reliable.

Interest Rates and Market Expectations: December and Beyond

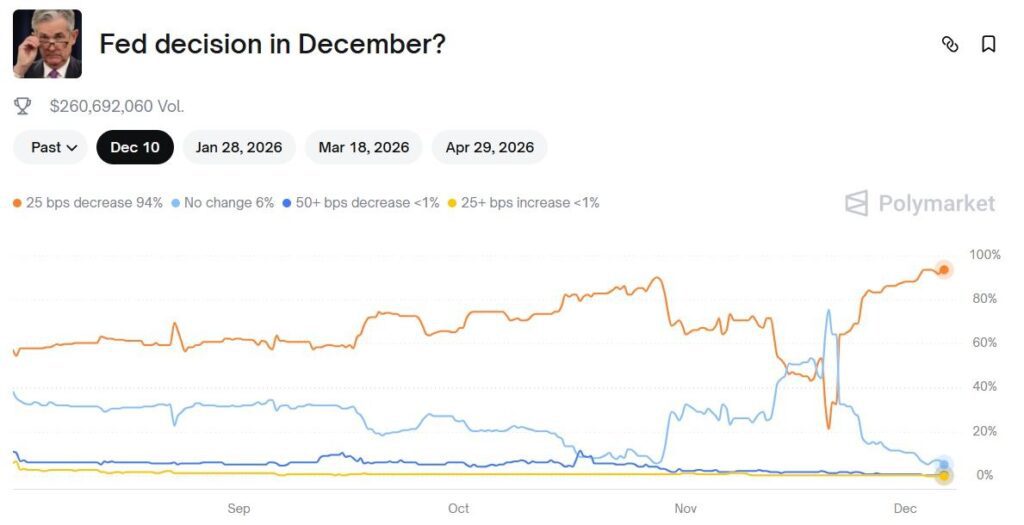

Rate cut expectations shifted again. Kevin Hassett, currently seen as the leading candidate to become the next Fed chair, hinted that a rate cut could come as soon as next week, with markets already pricing in about a 90% chance of a 25 basis point cut. On Polymarket, odds for a 25 bps cut even climbed to 94%.

Meanwhile, Kevin O’Leary took the opposite stance on timing. He said a December rate cut is unlikely, but added that Bitcoin should remain strong even without immediate support from the Fed. He made it clear he does not constantly rotate his portfolio based on potential cuts, which means his Bitcoin view is driven more by long-term fundamentals than by short-term monetary policy decisions.

Grayscale also published a bold macro view: they expect new all-time highs for Bitcoin in 2026, and argue that the old “every 4 years” halving cycle is no longer enough to explain market behavior. In their view:

- the market is more mature,

- institutions play a much bigger role, and

- ETF flows have changed the supply and demand mechanics permanently.

So while the next weeks are all about rate decisions, the bigger narrative is still about structural adoption.

Global Legal & Political Shifts: Crypto Enters the System

Several important moves showed how crypto is getting pulled deeper into legal and political structures.

- The United Kingdom officially recognized digital assets as a third category of property, alongside physical property and intangible property. This gives crypto stronger protection in courts and contracts, and marks a major step toward fully integrating digital assets into the UK’s legal and financial system.

- In the U.S., Fed Vice Chair Michelle Bowman said regulators are working on a new framework for stablecoins, according to a Bloomberg report. That means banks and regulators are preparing specific rules for stablecoin issuers and their reserves.

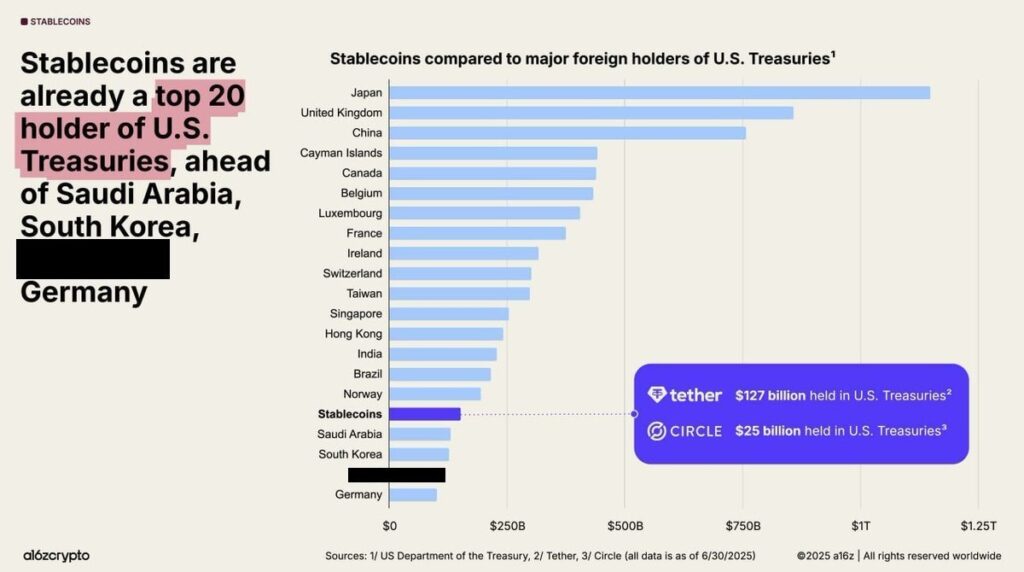

- Stablecoins themselves are now a major macro player. For the first time, stablecoins collectively became one of the top 20 holders of U.S. Treasury bills, ahead of countries like Saudi Arabia, South Korea, and Germany. This shows that stablecoins are no longer just a tool inside crypto, they are now a serious global financial force, holding U.S. debt at a scale comparable to nation-states.

- Japan’s crypto tax cut to 20% (mentioned earlier) is another sign of governments shifting from pure control to strategic support and competition for crypto capital.

- On the geopolitical side, Donald Trump confirmed authorization for military strikes on targets in Venezuela, specifically against drug networks. He noted that ground operations would be easier and would start soon. While this is not directly about crypto, such military moves can affect global risk sentiment, the dollar, and safe-haven narratives, areas where Bitcoin often appears in the conversation.

Institutional Bitcoin and ETFs: From Skepticism to Full Integration

On the institutional side, this week looked like a continuation of a big pivot toward Bitcoin:

- BTC ETF flows were negative, with about –$87 million across the week compared to +$70 million last week. However, the momentum behind their existence and integration into Wall Street continues to grow.

- Vanguard, managing $11 trillion, officially listed BlackRock’s spot Bitcoin ETF, with trading set to start the next day. This is notable because Vanguard has historically been very conservative about crypto.

- Goldman Sachs announced the $2 billion acquisition of Innovator, giving it access to a Bitcoin-linked ETF and expanding its portfolio of Defined-Outcome ETFs.

- Michael Saylor spoke at Binance Blockchain Week and highlighted the unbelievable speed of Wall Street’s turn toward Bitcoin. According to him, top banks like BNY Mellon, PNC, Citi, JPMorgan, Wells Fargo, Bank of America, Vanguard and others have moved in the last 12 months from doubt or rejection to full participation in crypto services.

- Schwab will start Bitcoin custody and crypto-backed lending next year.

- Citi is preparing a similar service.

- Out of the top 10 U.S. banks, 8 are now involved in crypto lending, and this shift happened mostly in just the last six months.

- Schwab will start Bitcoin custody and crypto-backed lending next year.

- Larry Fink, the CEO of BlackRock, admitted his own complete reversal. He went from calling Bitcoin a tool for illegal finance to running the largest spot Bitcoin fund in the U.S. This is a symbolic and practical confirmation of how far institutional perception has moved.

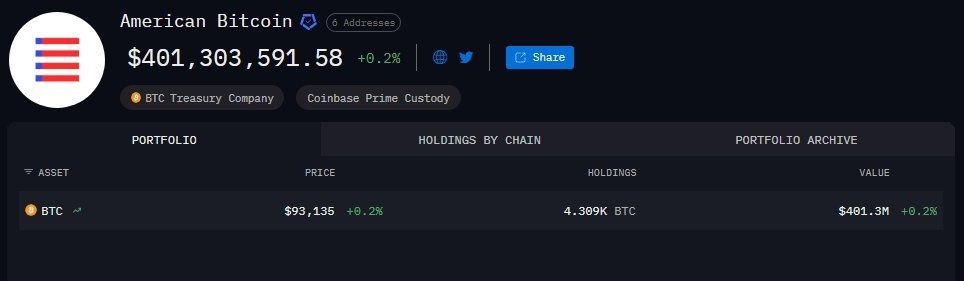

- American Bitcoin, a company linked to Trump, increased its Bitcoin reserves to 4,308 BTC. This reinforces the picture of Bitcoin becoming tied not only to finance, but also to specific political blocs that see it as part of their economic agenda.

- On the risk side, MicroStrategy made headlines twice. First, the company said it might be forced to sell Bitcoin if the market entered a continuous three-year bear cycle, something they consider a worst-case scenario. Second, data around the mNAV (modified Net Asset Value) level showed a key trigger:

- If mNAV drops below 1x, forced selling of more than 649,870 BTC (over $60 billion) could be required.

- The critical price level for this is around $73,575 per BTC.

- Right now, the indicator is at 1.13x, and as long as Bitcoin stays above $90,000, this risk is not active. But the market is watching it closely as a systemic risk point.

- If mNAV drops below 1x, forced selling of more than 649,870 BTC (over $60 billion) could be required.

Bitcoin Price Action and Market Structure

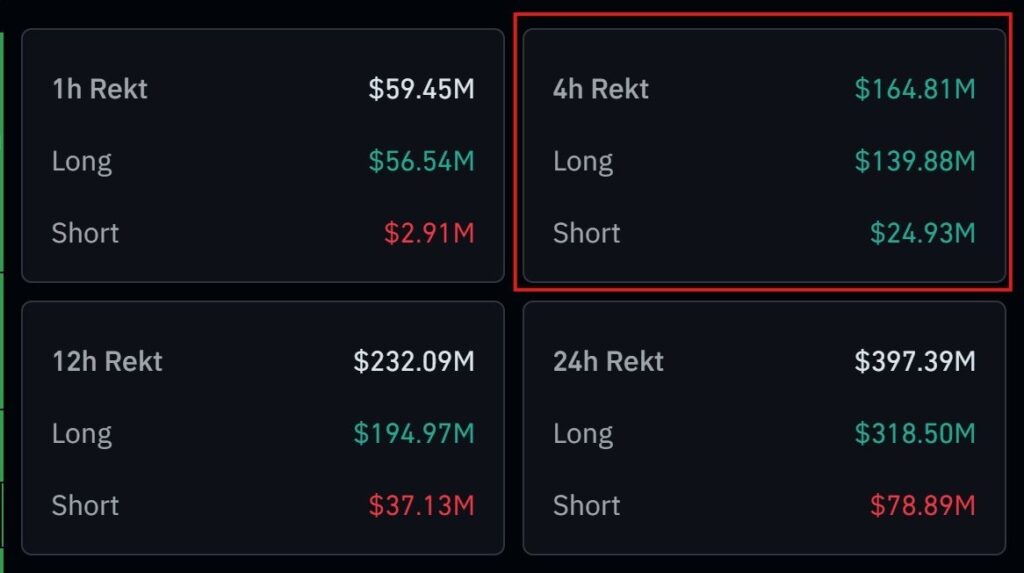

Price-wise, Bitcoin had a sharp move down this week. Yesterday, it fell below $90,000, triggering about $164 million in liquidations, mostly from long positions that were betting on further upside and could not survive the sudden drop. This confirms that many traders were still positioned for a rise, and got shaken out.

Despite the price dip and ETF outflows, the Market Buy/Sell Ratio (as mentioned) hit its highest level since 2023, signaling that buyers are still quite aggressive, and long-term accumulation is ongoing.

At the same time, overall spot volumes at $1.59 trillion in November show that many participants are still sitting on the sidelines. This combination, low volume but strong buy-side dominance, often comes before large directional moves in either direction.

Ethereum, ZEC, BNB, XRP and Other Major Tokens

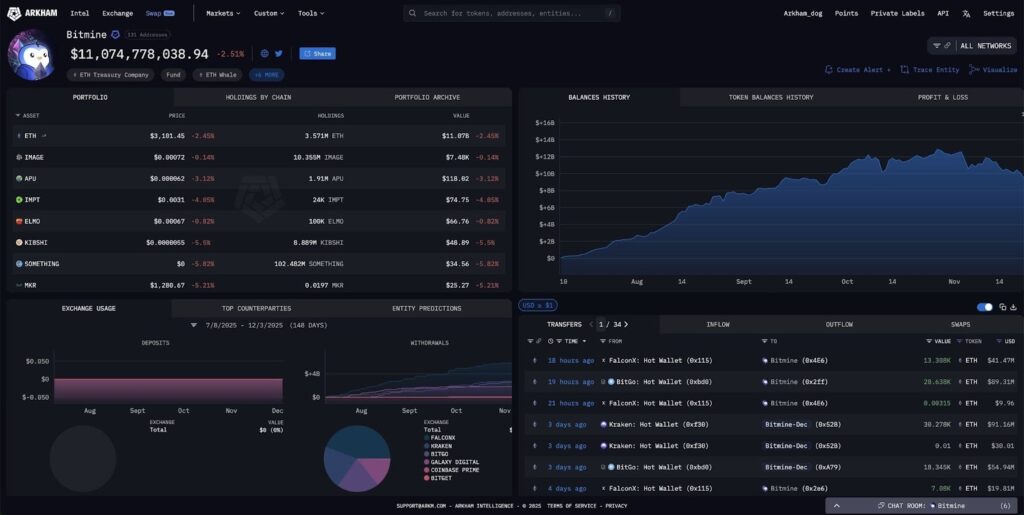

Ethereum (ETH) saw one of the biggest accumulation stories of the week. Two new wallets linked to Bitmine were detected buying a total of about $130 million in ETH this week, matching the known accumulation patterns of Tom Lee’s Bitmine operations.

- This week alone, Bitmine bought 97,650 ETH.

- They now hold around $12 billion in ETH, equal to 3.16% of the entire Ethereum supply.

This is a clear sign of aggressive accumulation and a strong bet on a major ETH bull cycle.

Zcash (ZEC) had one of the most violent short squeezes:

- Its market cap jumped from $6.3 billion to $6.7 billion in a very short time.

- This squeeze forced short sellers to close positions, leading to $710 million of short liquidations in a single hour.

BNB also had an institutional headline. CEA Industries, a Nasdaq-listed company, confirmed it is sticking to BNB as a core reserve asset. They hold 515,554 BNB, worth about $464.6 million, as part of their official reserve strategy. This shows corporations are willing to treat exchange tokens like BNB as long-term balance sheet assets, not just speculative positions.

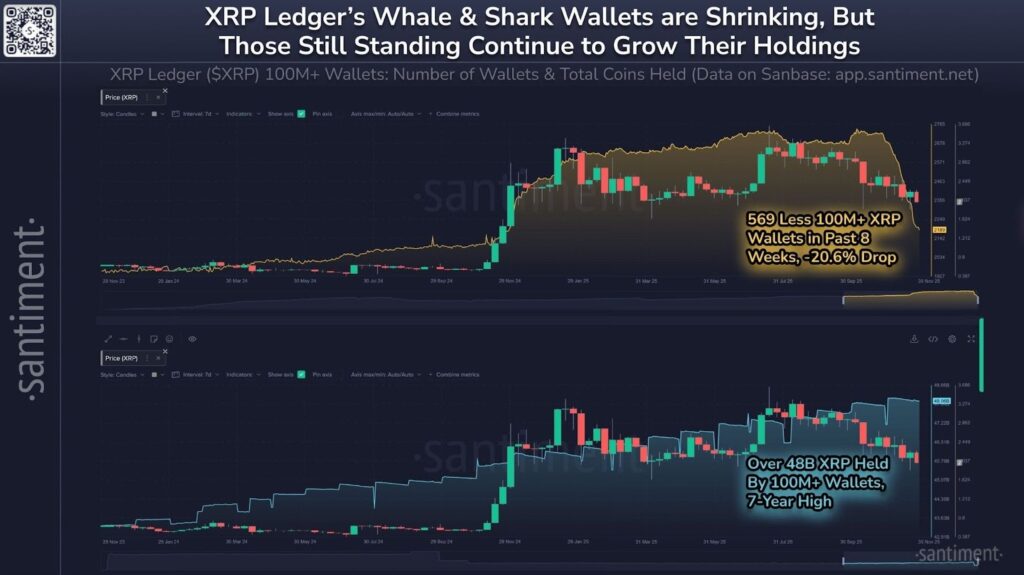

On XRP, data from Santiment showed a mixed picture:

- The number of whale wallets on the XRP Ledger has fallen over the last 8 weeks,

- but the whales that remain have accumulated to 48 billion XRP, the highest amount in seven years.

So the group of big holders has become smaller but more concentrated, which can have strong effects on future volatility and supply dynamics.

Chainlink also saw internal strengthening. The Chainlink Reserve added 81,131.31 LINK, bringing total reserves to 1,054,884.02 LINK. This continued build-up is meant to support liquidity and the broader ecosystem.

Networks, Fees, EVM Activity and Buybacks

Activity across blockchains showed clear leadership patterns:

- Tron was again the top network by fees in November, even though its fee levels dropped to their lowest since January 2023:

- Tron: $29.4 million

- Ethereum: $22.8 million

- Solana: $19.9 million

Crucially, 84% of Tron’s fees come from USDT transfers, proving that Tron has become the main backbone for Tether payments globally.

- Tron: $29.4 million

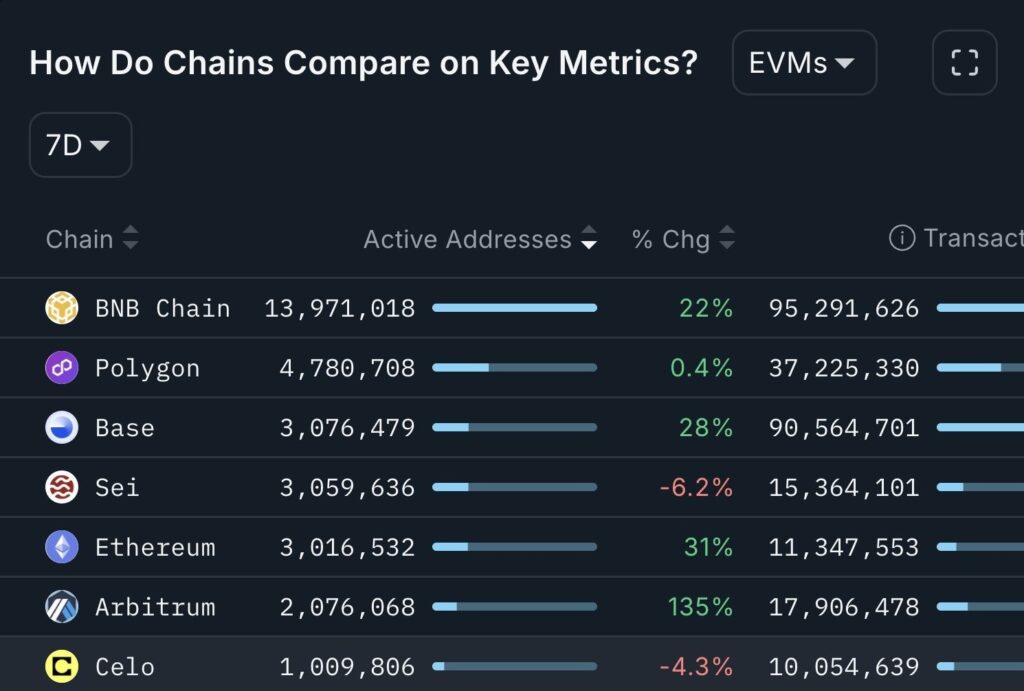

- Among EVM-compatible networks, the week’s activity showed:

- BNB Chain leading in active addresses,

- Arbitrum showing the fastest short-term growth with +135%,

- while over a month-long view, activity looks more “normal,” with BNB still dominant, and Polygon and Base regaining momentum with steady, renewed growth.

- BNB Chain leading in active addresses,

Buybacks and burns also continued to be a key theme:

- The ASTER team burned $77 million from its buyback wallet, tightening supply.

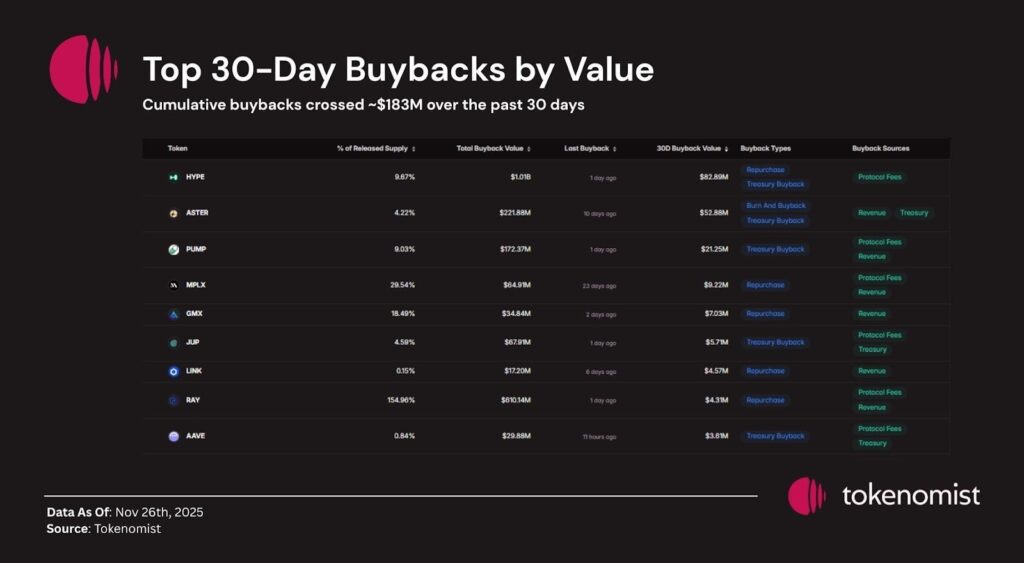

- Across the last 30 days, protocols executed over $183 million in buybacks. The leaders were:

- HYPE – about $81.02 million, currently the largest buyback program in the market and fully funded by protocol fees.

- ASTER – around $52.88 million, combining aggressive burning and buyback.

- PUMP – about $22.46 million from internal fees and incentives.

Other protocols like MPLX, GMX, RAY, LINK, JUP, and AAVE are also running regular buybacks, reflecting strong revenue generation and a focus on returning value to token holders.

- HYPE – about $81.02 million, currently the largest buyback program in the market and fully funded by protocol fees.

Solana, SKR, AI Agents and the New Payments Rail

On the Solana side, there were both product and payment updates:

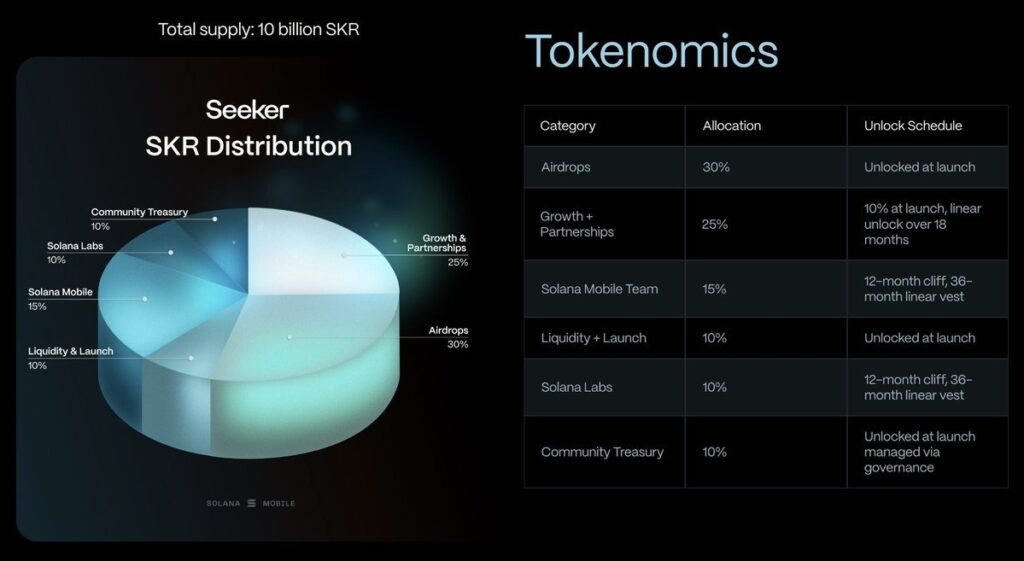

- Solana Mobile announced that it will launch a new token, $SKR, with a total supply of 10 billion in January. 30% of SKR will be airdropped to existing Solana phone owners, rewarding early hardware users.

- In payments, AI Agents are starting to play a noticeable role.

- Coinbase’s open payment protocol x402 processed more than $60 million in transactions.

- On the other side, Solana-based payments jumped to $380,000, a 750% increase in just one week.

Together, these moves suggest that we are at the early stages of AI-driven payment flows, where automated agents send money across blockchains directly.

Kalshi, a prediction market platform, had two major Solana-related headlines:

- Kalshi became the official forecast market partner for CNN, after raising $1 billion. CNN will now show Kalshi odds live on air, blending mainstream media with on-chain-style prediction markets.

- Kalshi also announced that it is tokenizing thousands of its prediction markets on Solana, enabling faster settlement, higher transparency, and easier scaling of its products.

These developments connect Solana not only to pure DeFi, but also to media, trading, and automated prediction rails.

DeFi vs TradFi: Regulation Battles and Tokenized Stocks

The line between DeFi and TradFi also sharpened this week.

Citadel submitted a request to the SEC asking that DeFi protocols be classified and regulated as exchanges, just like centralized trading platforms. The crypto community reacted with strong anger, because:

- treating DeFi as centralized exchanges would kill true decentralization,

- it would require KYC and other restrictions that do not fit autonomous smart contracts,

- and it would give traditional intermediaries more control over systems originally designed to be without intermediaries.

Many in crypto see this as an attempt by Citadel to protect its own business model by slowing or blocking DeFi competition. Others think it is part of a broader push to bring crypto under tight regulatory control before it grows too large.

Meanwhile, Nasdaq is pushing in the other direction, toward on-chain tokenization of TradFi assets. The head of its crypto division said they are moving “as fast as possible” to get SEC approval for trading tokenized stocks. If approved, investors could trade tokenized shares of companies directly on Nasdaq, blurring the lines between the stock market and blockchain-based assets.

Influencers, AI, and the Culture of Finance

The cultural side of finance also moved further toward tech and crypto narratives:

- MrBeast, the biggest YouTuber in the world, is working on a global financial services platform. With his reach, such a product could bring millions of users into new financial tools from day one, and possibly intersect with crypto or fintech rails.

- Jensen Huang, CEO of Nvidia, said in a conversation with Joe Rogan that Trump “saved the AI industry” through policies that pushed innovation and U.S. companies forward. This merges politics, AI, and markets into one story, and indirectly connects to crypto because Nvidia GPUs and AI infrastructure are deeply tied to both AI and some blockchain activity.

Summary: Cautious Surface, Aggressive Undercurrent

Putting everything together, this week looked like this:

- Short term: BTC ETF flows turned negative again (–$140M), Bitcoin dipped below $90K and wiped out $164M in mostly long liquidations, and overall spot volumes are at multi-month lows. Bond stress in Japan and mixed macro signals are pressuring global liquidity.

- Medium to long term: Institutions like BlackRock, Vanguard, Goldman Sachs, and major banks continue to move deeper into Bitcoin and crypto ETFs. Corporates hold BNB and Bitcoin as reserves. Stablecoins now hold U.S. T-bills like a medium-sized country. Governments like Japan and the UK are softening taxes and recognizing crypto legally, while stablecoin regulation frameworks are being built. Big players are accumulating ETH, XRP, LINK and others, buybacks are strong across several protocols, and networks like Tron, BNB, Arbitrum, Solana, Polygon, and Base are quietly building their own roles in payments, DeFi, and prediction markets.

The outward picture is one of hesitation and fear of the next move, but underneath, accumulation, integration, and infrastructure growth continue at full speed.

This article is not financial advice. Always do your own research, and you can find more educational material on blog.millionero.com. When you feel ready to trade, you can use Millionero for spot and futures markets, but only with money you can afford to lose.