Bitcoin Under Pressure: Fear, Capitulation, and the Search for a Bottom

It has been a rough week for Bitcoin. The dominant story across the market was a sharp and sustained drop that pushed Bitcoin into a zone traders call “Extreme Fear” on the Crypto Fear & Greed Index. For many in the space, this feeling was familiar, and not necessarily in a bad way.

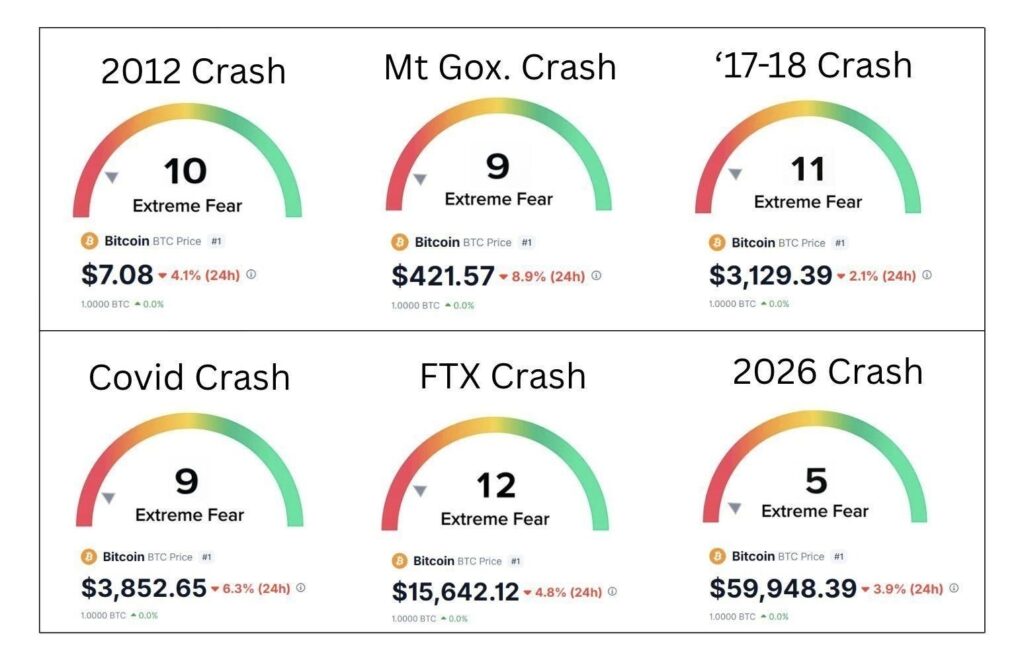

Analyst Quinten François pointed out that every major moment of Extreme Fear in Bitcoin’s history ended up being a turning point, not a graveyard. He traced the pattern back through the 2012 crash, the Mt. Gox collapse, the 2017–2018 bear market, the COVID crash of 2020, and the FTX implosion in 2022. In each of those moments, Bitcoin was priced at what seemed like impossibly low levels, $7, $400, $3,000, $15,000, and in each case, long-term holders who stayed in were rewarded. His argument this week was that the structural picture in 2026 is meaningfully different from past cycles: institutional investors are in the market, ETFs are live, some governments are actively mining Bitcoin, and the infrastructure around the network is far more developed than it was during any of those previous crashes. The fear itself, he suggested, is a signal that weak hands are leaving, not that the story is over.

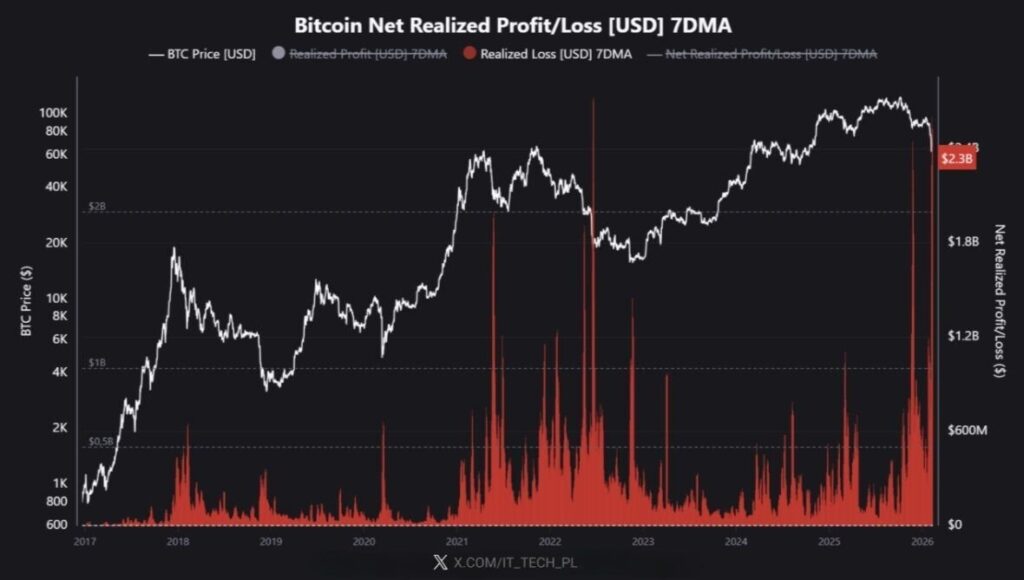

That idea was backed up by on-chain data from CryptoQuant, which flagged one of the largest Capitulation events in Bitcoin’s history this week. CryptoQuant ranked this event among the top three to five loss-realization moments of all time, comparable in scale to the collapse of late 2021. What capitulation means in plain terms is this: a large number of investors sold their Bitcoin at a loss. They gave up. Positions were liquidated across the market. According to CryptoQuant’s framing, these moments tend to mark the peak of pain in a cycle, the point where coins move from people who are scared into the hands of those who are not.

The 200-week moving average (200WMA) was also front and center in the discussion. One widely-shared analysis noted that in every major bear market cycle, 2015, 2018, 2020, and 2022, Bitcoin’s price has touched or broken below the 200WMA before recovering. This week, that moving average sits around $60,000, and Bitcoin touched it. Historically, the pattern from here has gone one of three ways:

- An immediate bounce from current levels

- A dip of around 20% to approximately $48,000

- In the worst historical scenarios, a drop of closer to 30% toward $42,000

The analyst was careful not to predict which outcome would happen, but noted that every time Bitcoin has been near these levels historically, it has turned into a buying opportunity in hindsight.

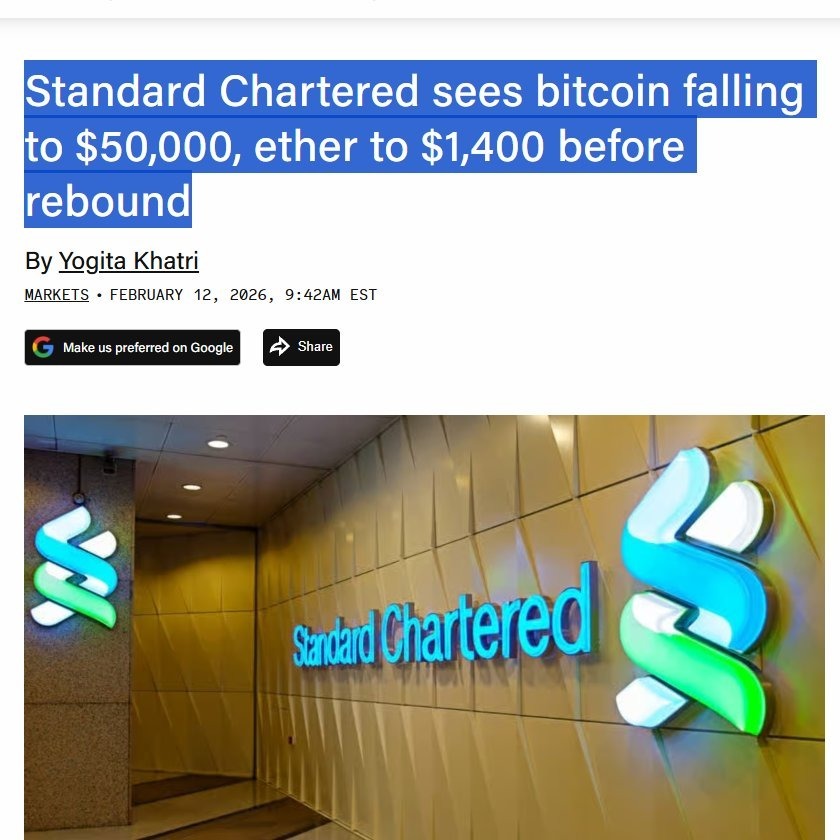

Standard Chartered added its voice to the bearish side of the debate, forecasting that Bitcoin could fall to $50,000 and Ethereum to $1,400 before any meaningful recovery begins.

Meanwhile, prediction market platform Kalshi showed traders actively betting on Bitcoin reaching $48,000 at some point this year.

On the more counterintuitive end, Anthony Pompliano noted that despite the sharp-looking drops, this current correction is actually the smallest Bitcoin has ever had from a peak, in relative terms. The annualized volatility of Bitcoin has roughly halved, from around 80% historically down to about 40% today. The market is becoming less wild even as it feels painful.

Not everyone was being thoughtful about it. Jim Cramer, the television personality known for his often-backwards market calls, declared this week that Bitcoin “has lost its luster,” argued that its price falling alongside a weak dollar proved it wasn’t really a store of value or inflation hedge, and called it “just a speculative asset that’s starting to collapse.” Given Cramer’s track record as an accidental contrarian indicator, his bearish turn was noted by many in the community with a degree of amusement rather than alarm.

Capital Flows, Liquidations, and Structural Weakness

The sell-off was not just emotional. The numbers behind it were significant. More than $4 billion in leveraged positions were liquidated across crypto markets in just five days. This is what happens when the market moves quickly against traders who borrowed money to amplify their bets, their positions get force-closed, which adds more selling pressure, which triggers more liquidations in a cascade.

On-chain data from Glassnode described the broader structural picture as a market stuck in a defensive posture, with Bitcoin ranging between $60,000 and $72,000, selling pressure sitting above current prices, and trading volumes that are reactive rather than proactive. Buyers are showing up when prices dip, but not with enough conviction to push through the supply sitting overhead. The market needs real structural demand, not just dip-buying, to break out of this range.

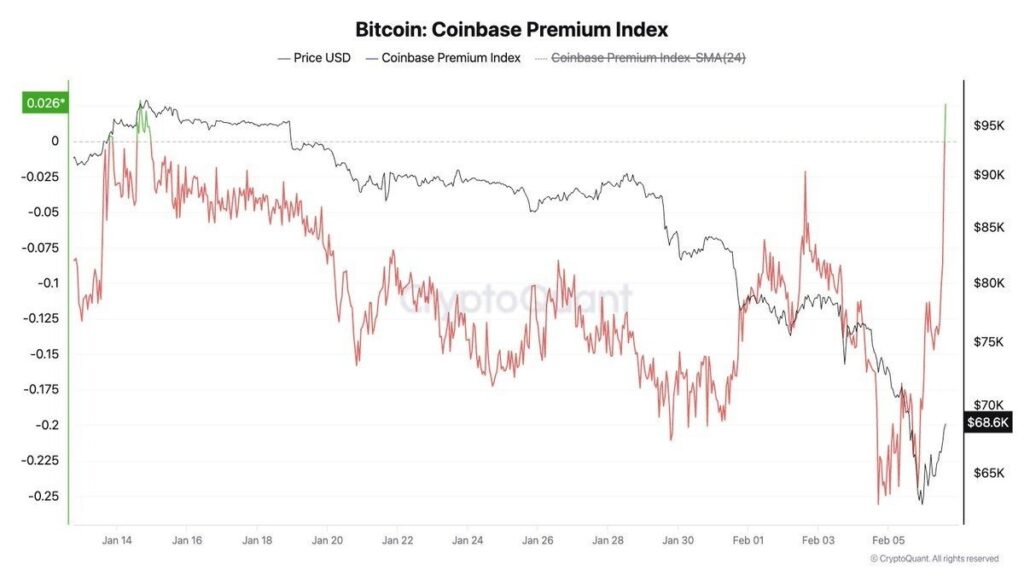

There was, however, at least one positive signal mid-week. The Coinbase Premium Index, which measures whether Bitcoin is trading at a higher price on Coinbase compared to offshore exchanges, a rough proxy for American retail and institutional buying, turned positive on February 7th for the first time since mid-January. This suggested that U.S. buyers were stepping back in as Bitcoin bounced off the $60,000 level, which was an encouraging sign even if it didn’t change the bigger picture.

One broader context worth noting: the U.S. stock market lost about $1 trillion in market value in a fast sell-off during the week, with all eyes on incoming CPI (Consumer Price Index) data that could signal whether inflation is still a problem. The uncertainty around that data was feeding into crypto markets too, since rising inflation expectations tend to keep the Federal Reserve from cutting interest rates, which tends to weigh on risk assets like Bitcoin. However, CPI came in within expectations.

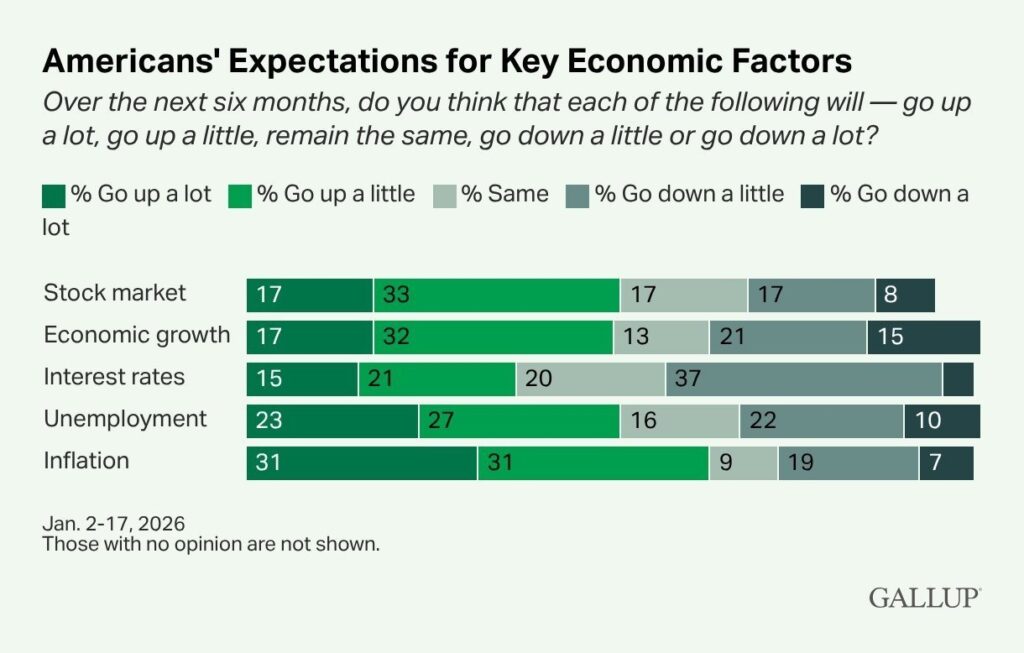

A separate Gallup survey revealed a striking split in American sentiment: roughly 50% of people expect stocks to go up, while 50% expect unemployment to rise. As one commentator noted, that kind of divergence between financial optimism and economic pessimism doesn’t last, either the economy improves to match market prices, or markets fall to match the economy.

Michael Saylor, Strategy, and the Bitcoin Accumulation Playbook

One company that showed no sign of changing course was Strategy (formerly MicroStrategy), led by Michael Saylor. Despite the company sitting on paper losses exceeding $5 billion on its Bitcoin holdings this week, Saylor was unambiguous: “We won’t sell. We will keep buying Bitcoin.” He confirmed that Strategy will continue purchasing Bitcoin every quarter regardless of price conditions.

To fund that strategy without putting more pressure on the company’s common stock, Strategy’s CEO Phong Le announced a new preferred share offering called “Stretch.” This new class of shares would carry an 11.25% dividend yield with monthly resets, targeting a stable price of $100 per share. The idea is to shift Strategy’s fundraising away from issuing more common stock, which dilutes existing shareholders and can drag the stock price down, toward preferred shares that attract yield-seeking investors. The goal, in essence, is to keep accumulating Bitcoin while managing the capital structure more carefully.

Regulatory Landscape: A Busy Week in Washington

The regulatory picture in the United States moved in several directions at once this week, which is becoming a normal state of affairs.

On the constructive side, SEC Chairman Paul Atkins publicly backed the CLARITY Act, describing a clear federal framework for crypto regulation as something the country has needed for a long time. He outlined a joint effort between the SEC and the CFTC to establish a Token Taxonomy, essentially a rulebook for how to classify different types of crypto assets, alongside potential exemptions for certain on-chain activities and a refocusing of enforcement on actual fraud rather than regulatory ambiguity. For an industry that has spent years operating under unclear rules, this was a notable statement of direction.

In a related development, Sergey Nazarov, the co-founder of Chainlink, was appointed to the CFTC’s Innovation Advisory Committee. Chainlink is a major piece of blockchain infrastructure, it provides the data feeds that smart contracts use to interact with the real world, so having its founder at the regulatory table signals a genuine effort to bring technical expertise into the rule-making process.

However, the picture in Washington is not uniformly positive for crypto. Meetings at the White House between banks and crypto companies about stablecoin yield rules ended without an agreement. Banks reportedly pushed for a near-total ban on stablecoins paying interest to users, which participants said was more restrictive than even the current draft legislation. Crypto firms pushed back, arguing for a framework that allows innovation. The tension between the two sides remained unresolved.

The banking lobby also escalated its campaign to keep crypto firms from accessing Federal Reserve payment networks. The argument from banks is that giving stablecoin issuers access to the Fed’s infrastructure, even conditionally, tied to legislation like the GENIUS Act, before a full regulatory framework is in place creates systemic risk. The counter-argument from the crypto side is equally blunt: if stablecoin issuers can settle directly through the Fed, transactions become faster and cheaper, costs drop, and deposits start flowing out of traditional banks. The fight isn’t really about technology, it’s about who controls the layer of infrastructure that money moves through.

DeFi, Ethereum, and a Week of Milestones

Despite the market downturn, some notable things happened on the protocol side of the industry.

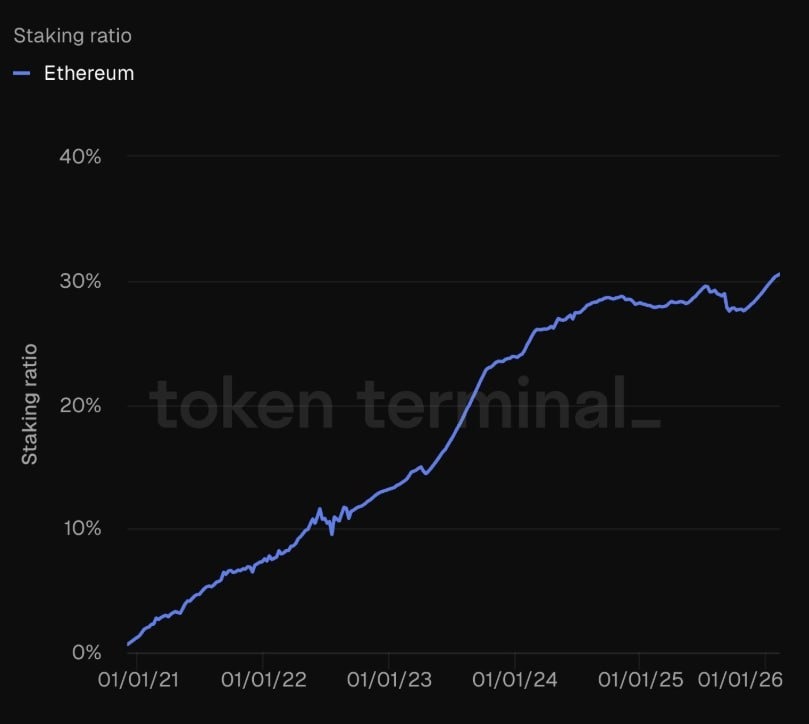

Ethereum hit a milestone this week that hadn’t been reached before: more than 30% of the total ETH supply is now locked in staking, according to Token Terminal. Staking means holders are locking their ETH in the network in exchange for yield, effectively committing to hold it rather than sell it. A staking rate above 30% reduces the amount of ETH circulating freely, which in theory means less immediate selling pressure.

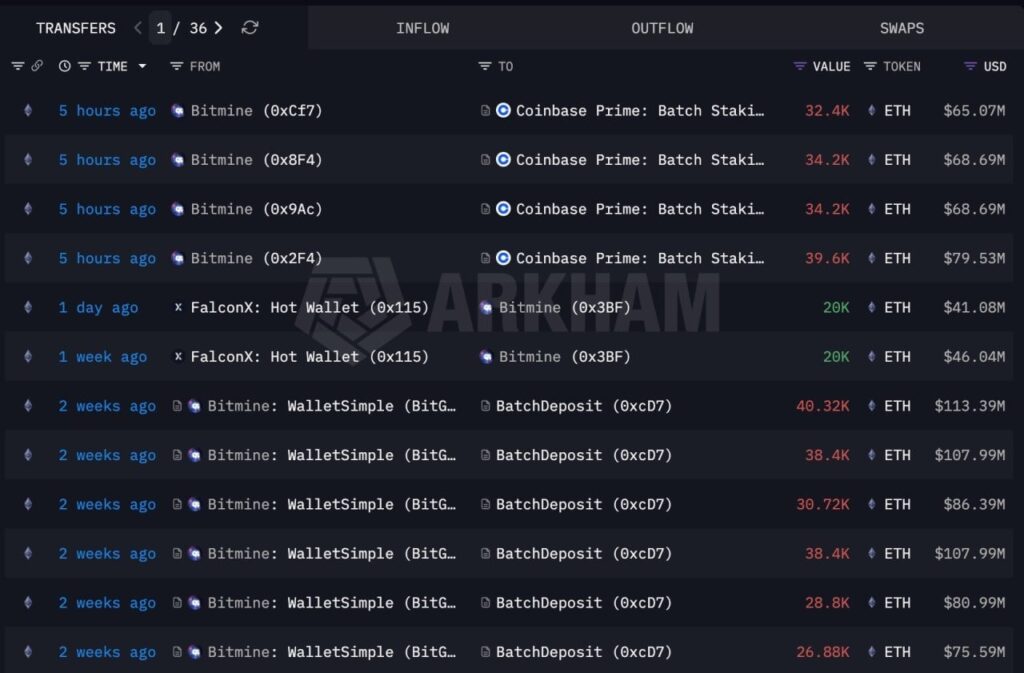

Combined with the fact that Bitmine ($BMNR), the company backed by Tom Lee, added another 140,400 ETH to its holdings this week, bringing its total to nearly 3 million ETH worth approximately $6 billion, the institutional commitment to Ethereum remained strong even through the volatility.

On the DeFi side, Uniswap had a dramatic moment when BlackRock announced it would make its BUIDL tokenized money market fund tradable on the Uniswap protocol, with plans to purchase an undisclosed amount of the UNI governance token. UNI jumped 40% in under ten minutes. BlackRock is the world’s largest asset manager, and its decision to plug into a decentralized exchange rather than a traditional one carries symbolic weight well beyond the price move.

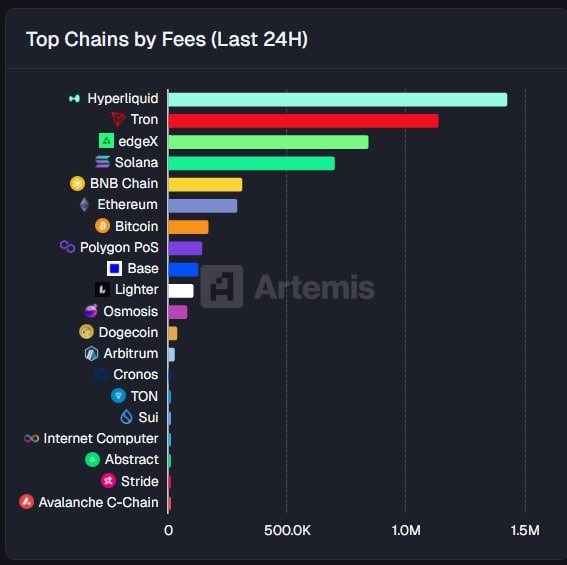

Hyperliquid, the decentralized derivatives exchange, topped all platforms in fee revenue over 24 hours with $1.4 million, ahead of Tron and EdgeX.

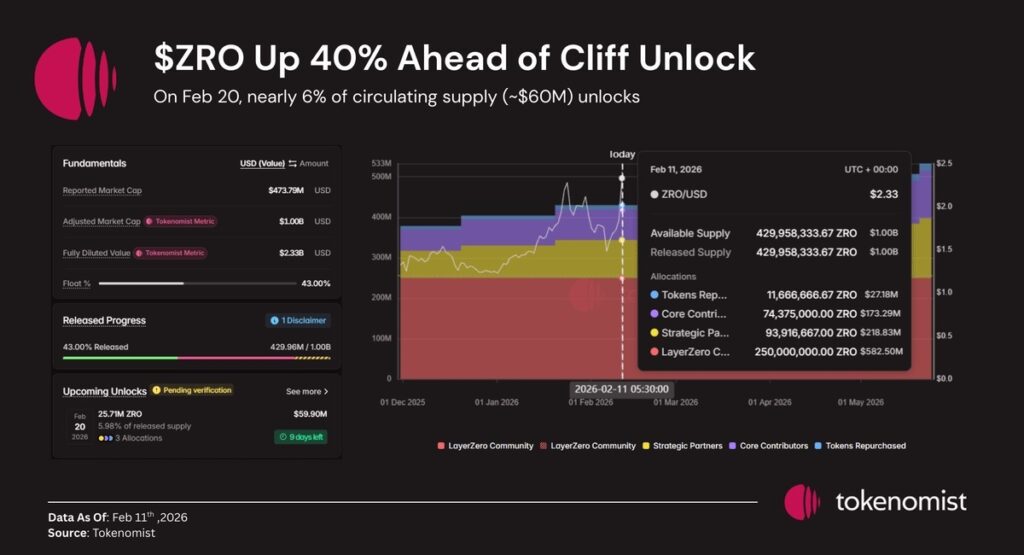

Separately, LayerZero’s ZRO token surged 40% ahead of a token unlock event on February 20th, when approximately 6% of total supply, worth around $60 million, will enter circulation. LayerZero also announced an investment from Tether and partnerships with major banks, alongside an investment from ARK Invest. Whether the rally holds through the unlock or gives way to selling pressure afterward is the question traders are watching.

Charles Hoskinson, founder of Cardano, offered a sobering counterpoint to any near-term optimism. He said the industry is “not in good health” and that sentiment has reached historically low levels. His argument was that crypto needs a new narrative to rally around, because the current one has run its course.

Geopolitics and the Macro Chess Board

Some of the most significant news this week came from outside the crypto markets entirely, but with direct implications for them.

China ordered domestic banks to reduce their exposure to U.S. Treasury bonds, a significant geopolitical signal that China is repositioning its reserves away from dollar-denominated assets. This matters for global capital flows and for the broader question of dollar dominance in international trade.

In a related development, Russia signaled openness to using the U.S. dollar again, and reports emerged of a potentially large trade deal being negotiated with the United States. Shortly after, China announced it would provide an energy aid package to Ukraine. The sequence of events was notable: one major geopolitical player warming to the dollar, and another offering support, even if limited, to a country it had previously been distant from. International politics is not about feelings or permanent alliances. It is about calculations and shifting interests.

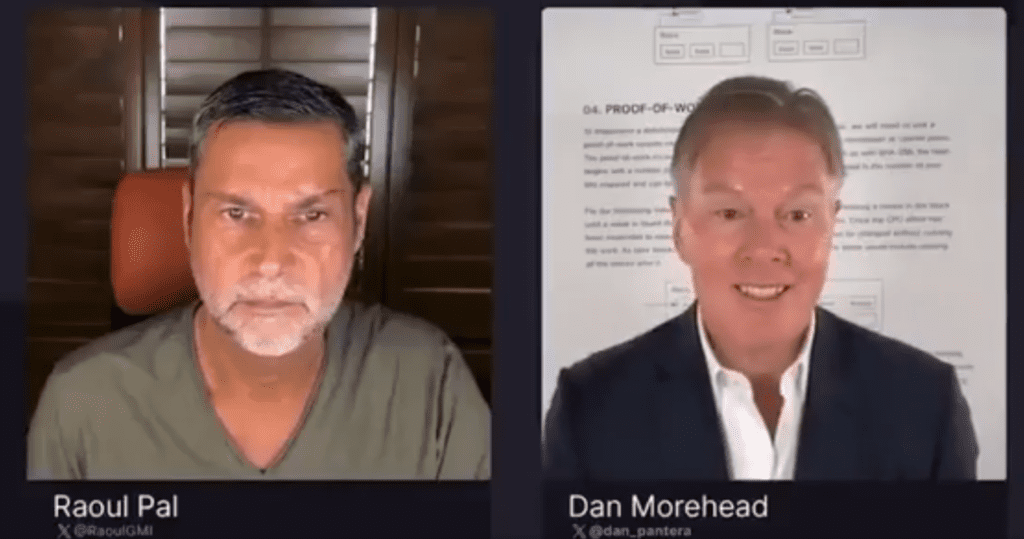

Meanwhile, billionaire investor Dan Morhead made a striking prediction: that China will eventually buy one million Bitcoin, representing nearly 5% of the total supply that will ever exist. If that happens, it would not just be a market event, it would be a sovereign decision with geopolitical consequences that dwarf any single institutional trade.

On U.S. monetary policy, Donald Trump said this week that he made a “very big mistake” in choosing Jerome Powell as Federal Reserve Chair back in 2017, and said he believes Kevin Warsh would have been the better choice. Trump claimed that under Warsh, the U.S. economy could grow by 15% or more. He also argued more broadly that lower interest rates would help reduce the burden of U.S. national debt, a claim that economists would debate, since lower rates can also fuel the kind of inflation that erodes savings and complicates economic management.

Bank of America separately moved up its forecast for when the Bank of Japan will next raise interest rates, now expecting a 25 basis point hike in April rather than June, which would bring Japanese rates to 1.0%, the highest level in thirty years. The Bank of Japan’s rate decisions matter globally because decades of near-zero rates in Japan led to massive carry trade flows, where investors borrow cheap yen and invest in higher-yielding assets elsewhere. Any meaningful shift in Japanese rates has a way of rippling through global markets in unexpected directions.

Institutions, Tokens, and the Mainstream Creep

Goldman Sachs disclosed its crypto holdings in a regulatory filing this week:

- $1.1 billion in Bitcoin

- $1 billion in Ethereum

- $153 million in XRP

- $108 million in Solana

The disclosure confirmed what many had suspected, that Wall Street’s largest investment bank has been building a meaningful crypto position. The allocation is still small relative to Goldman’s total assets, but the direction of travel is clear.

The United Kingdom announced it is testing the issuance of a Digital Gilt Instrument, essentially a government bond issued on a blockchain, using HSBC’s Orion platform. If it proceeds, the UK would become the first G7 country to issue a sovereign debt instrument on distributed ledger technology (DLT). HSBC argued that blockchain-based bonds could settle faster and reduce operational complexity compared to traditional systems. The move reflects a broader trend of governments taking blockchain seriously as infrastructure rather than just speculative technology.

This theme was echoed in a report from the Abu Dhabi Blockchain Centre, which described how blockchain has moved from experimental to operational in the UAE. The country processed more than 20 trillion dirhams in domestic transfers over a ten-month period, 95% of residents send international remittances, and tokenized real estate, funds, and sukuk bonds are now live products, not whitepaper concepts.

Tether, the company behind the world’s most widely used stablecoin USDT, continued its transformation from crypto infrastructure provider into a diversified investment group. According to the Financial Times, Tether now holds roughly 140 investments, employs about 300 people, and is hiring 150 more, all under the direction of a new CFO focused on growth outside traditional crypto markets.

Quantum Computing, CBDCs, and the Risks Nobody Wants to Think About

Two risk conversations that came up repeatedly this week deserve mention.

Joseph Lubin, one of the co-founders of Ethereum, raised the quantum computing threat to Bitcoin this week, referring to what is sometimes called “Q-Day”, the hypothetical future point when quantum computers become powerful enough to break the cryptographic algorithms that secure Bitcoin addresses. Lubin said the concern is “reasonable,” even if we are not there yet. The question, he said, is not whether quantum computers will eventually pose a threat, but whether Bitcoin’s codebase will be updated before that threat becomes real.

CoinShares pushed back on the narrative, arguing that only around 10,200 Bitcoin are actually at risk from quantum attacks in the near term, a small fraction of the roughly 21 million that will ever exist. Their view is that the widespread panic about quantum computing and Bitcoin is significantly overstated. The technical reality, for now, is that the threat is real in the abstract but not imminent in practice.

Ray Dalio added another kind of warning to the week’s discourse, cautioning that Central Bank Digital Currencies (CBDCs), the digital currencies that central banks around the world are developing, could become tools of financial surveillance and control. His concern was specific: CBDCs would technically allow governments to track every transaction, apply taxes in real time, freeze accounts, or cut off financial access for political dissidents. He acknowledged that CBDCs might improve efficiency in some ways, but argued the tradeoff in privacy and individual financial sovereignty is severe. It is a debate that has no clean resolution, and it sits at the heart of why many people hold decentralized assets like Bitcoin in the first place.

Solana and the Payments Race

Finally, one piece of data that cut through the noise: Solana was ranked the fastest-growing payment platform in the world over the past year, with a 755% year-over-year increase in payment volume, according to data from Artemis. That number is not about the price of SOL, it reflects actual transactions, real money moving through the network for real purposes. In a week full of fear and uncertainty, it was a reminder that the underlying usage of some of these networks is growing regardless of what the price is doing on any given day.

This article is not financial advice. Always do your own research (DYOR) before making any investment decisions. You can also DYOR on blog.millionero.com. When you’re ready, trade spot and perpetuals on Millionero.