This past week was full of signals that the crypto market is maturing on the surface, while politics, regulation, and security risks keep building underneath. Bitcoin did not explode up or down, but the stories around it, from courts and parliaments to embassies and whales, were very loud.

Governments, courts, and new rules for Bitcoin

One of the clearest signs of how serious regulators are becoming came from South Korea.

The Supreme Court of South Korea ruled that Bitcoin held on centralized exchanges can be confiscated under criminal law. In simple words: if funds on an exchange are linked to a crime, the state can legally seize that Bitcoin. This puts extra pressure on Korean users who keep coins on platforms instead of in self-custody wallets.

In the United States, the big political fight is over how to structure the entire digital asset market:

- A digital asset bill in the US Senate is moving toward a decisive moment. But disagreements around stablecoins and some Trump-related issues are threatening progress and could endanger key votes. So the future of US crypto law is still stuck in political drama.

- At the same time, the Senate Banking Committee will vote on Thursday on whether to open full debate and amendments on a Bitcoin and crypto market structure bill. This vote is a key step toward clearer rules, less legal fog for investors, and easier entry for big institutions.

There is also a separate front where US community banks are fighting the crypto world. They are pushing to close what they call a “loophole” in the GENIUS law, which lets exchanges pay yield on stablecoins.

Banks argue that:

- Exchanges have an unfair advantage.

- Stablecoin yields pull liquidity out of traditional banks.

- These yields are offered without the same strict rules that banks face.

In short, TradFi vs stablecoins just escalated. Any change to this law could directly hit stablecoins, exchanges, and overall market liquidity.

In Europe, the tone is still very cautious.

Christine Lagarde, head of the European Central Bank, said Bitcoin will not be added to central bank reserves in the EU. She explained that reserves must be liquid, safe, guaranteed, and not linked to money laundering or criminal activity.

The commentary around it was simple: “Europe is always late,” again showing how slow the EU is compared to the US and some states like Texas.

Japan is taking the opposite direction.

Japan is moving to cut capital gains tax on crypto to around 20% and the finance minister supports bringing digital assets into the traditional financial system. That is a very different message from Europe and shows that Asia is competing to be more crypto-friendly.

Macro, politics, and war risks

The macro and political backdrop this week was noisy and confusing.

In the US:

- Treasury Secretary Scott Bessent said that millions of Americans may get the biggest tax refund of their lives this year. That kind of refund could boost spending and maybe risk assets, but it also raises questions about fiscal policy and deficits.

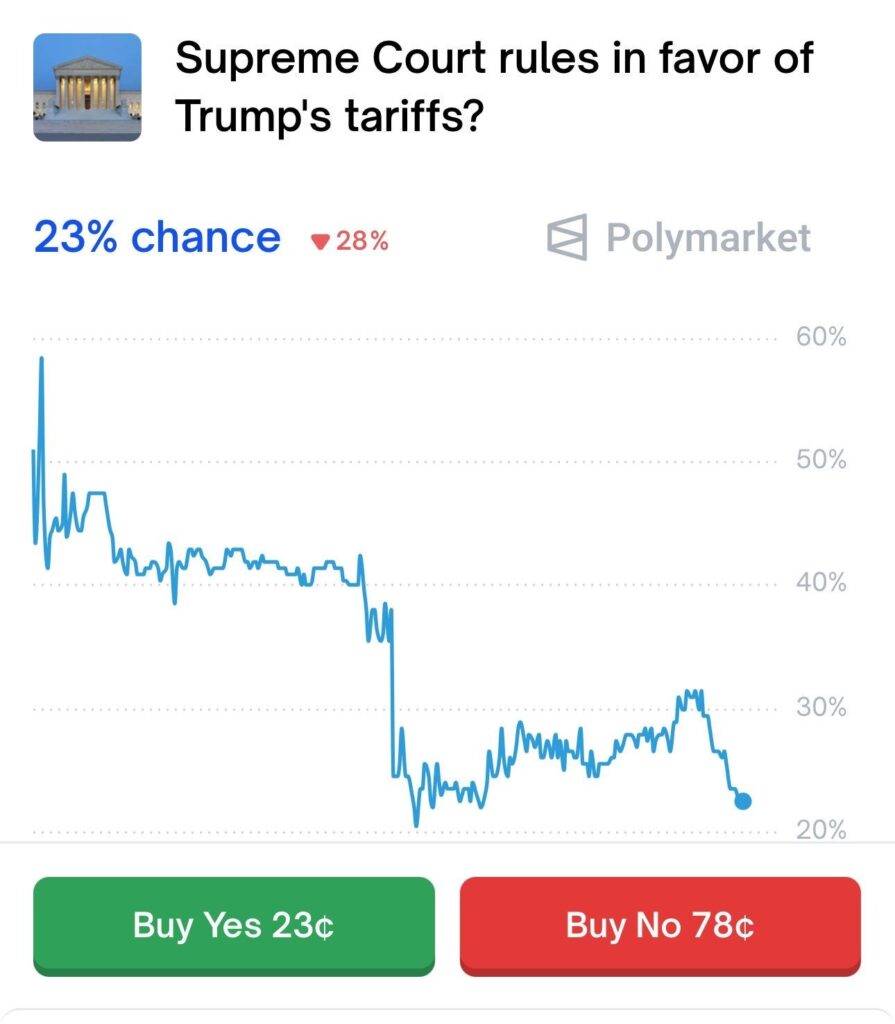

- A more dangerous story is the legal case around Donald Trump’s tariffs. The US Supreme Court may force him to return more than $133 billion in tariff revenue. Estimates say there is a 77% chance the court rules on Friday that the tariffs were illegal.

At the same time, the White House said Trump has considered using the US military to take control of Greenland. The summary is brutal:- Huge legal risk around US trade policy.

- A possible financial shock if tariff money has to be refunded.

- Geopolitical statements that could easily spook global markets.

Key US economic data also shifted on the calendar.

December income data, PCE (Personal Consumption Expenditures), and GDP were rescheduled to February 20, instead of January 29. This delay pushes back one of the most important data points for the Fed’s rate decisions and for traders who link macro numbers to Bitcoin and other risk assets.

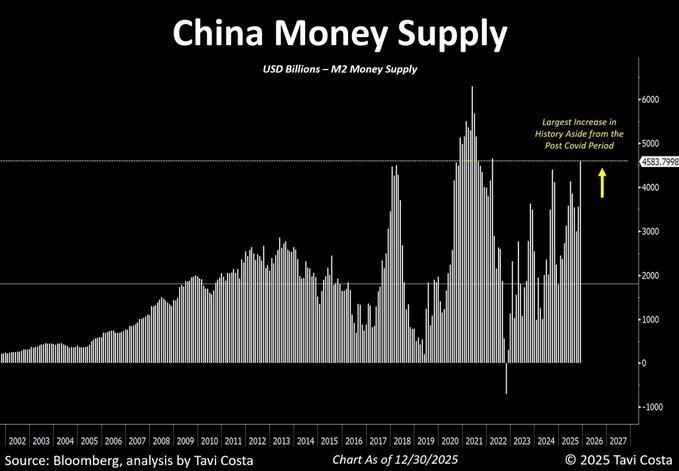

Outside the US, China delivered the largest increase in money supply in its history, except during the Covid crisis. This is heavy monetary stimulus, meant to support growth, credit, and deal with any economic slowdown or internal pressure. It also adds to the global liquidity picture that many Bitcoin bulls watch closely.

On the war and security side, the US embassy in Kyiv warned of a potential large air attack in the coming days. This keeps geopolitical risk high and reminds markets that war headlines can still hit risk sentiment at any time.

Bitcoin as a reserve asset and big-holder behavior

A symbolic moment for Bitcoin as “strategic money” came from Texas.

The Texas Senate passed a Bitcoin Strategic Reserve law. Texas is the eighth-largest economy in the world, so this move is like Italy, France, or India announcing a Bitcoin reserve. It doesn’t instantly change global reserves, but it sends a strong political signal about Bitcoin as a long-term store of value.

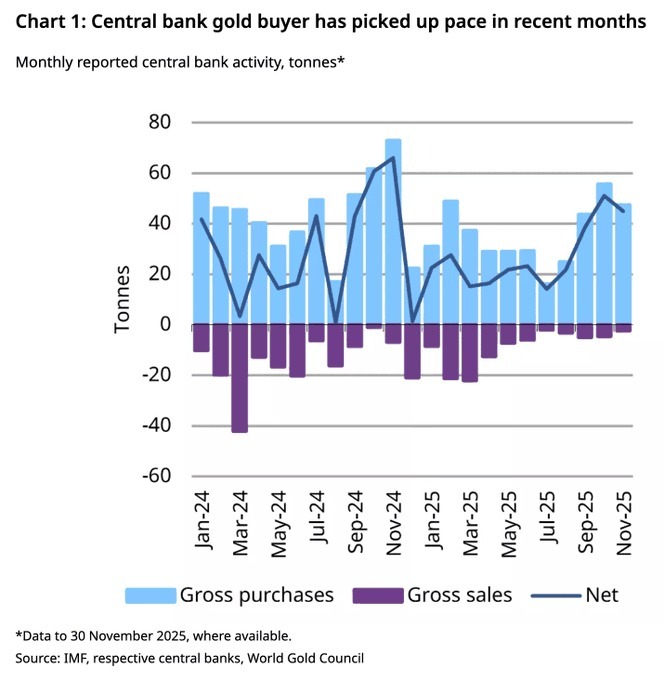

At the same time, central banks around the world continue to prefer gold, not Bitcoin:

- Central banks bought more than 300 tonnes of gold in 2025.

- And as noted earlier, the ECB openly rejected holding Bitcoin in reserves.

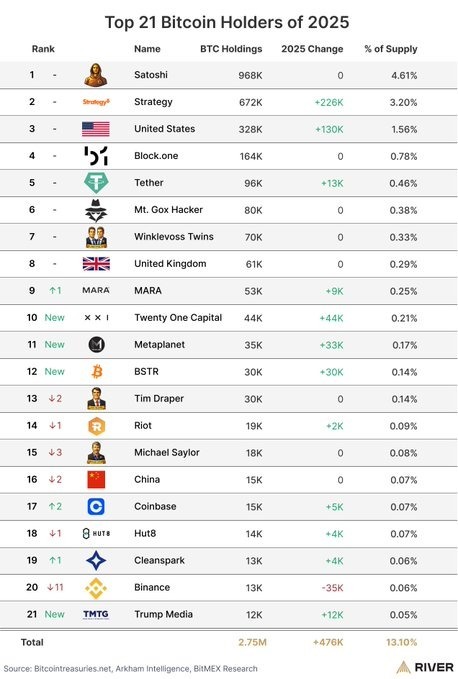

Even so, large private entities are quietly stacking BTC.

The largest 21 companies and holders accumulated around $40 billion worth of Bitcoin in 2025, according to River. The question now is: how will accumulation look in 2026?

MicroStrategy / Strategy stayed in the spotlight too:

- MSCI decided not to remove Strategy (Michael Saylor’s company) from its indexes, a big boost to all firms using Bitcoin as a main treasury asset.

- The direct result: MSTR rose about 6% in after-hours trading.

On the policy side, Raoul Pal (@RaoulGMI) said that the Digital Asset Market Structure bill will pass, and that big banks will eventually start promoting Bitcoin. If that happens, we move from banks fighting crypto to banks actively selling it, a huge narrative shift.

Bitcoin market mood: oversold, sideways, and no whales (yet)

Market data showed a strange mix of stress and boredom.

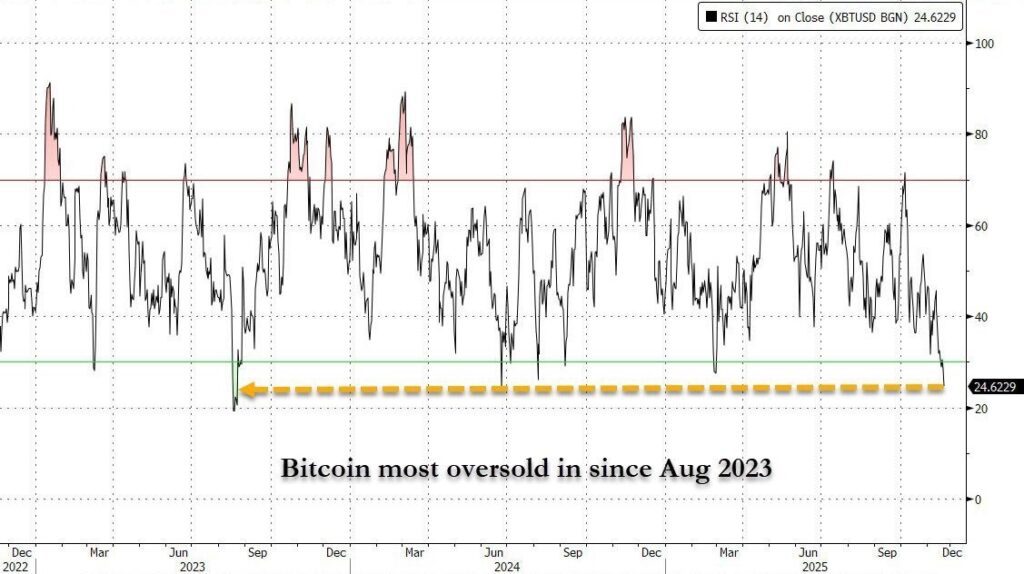

On the one hand, technical indicators point to extreme oversold conditions:

- Bitcoin is at its strongest oversold level since August 2023, the bear-market bottom.

- Historically, such levels often line up with weaker selling pressure, coming consolidation, or the start of a slow reversal.

But timing is still delicate, and nobody knows exactly when the turn happens.

On-chain and flow data gave another angle:

- According to @ki_young_ju, capital inflows into Bitcoin have dried up.

- Liquidity channels are now more diverse, so timing flows is less useful.

- Long-term institutions entering the market have ended the old cycle where whales dump on retail over and over.

- He also says Strategy (MSTR) is unlikely to sell a meaningful part of its 673,000 BTC, and overall liquidity has shifted toward stocks and precious metals.

- His base case: a boring sideways market for months.

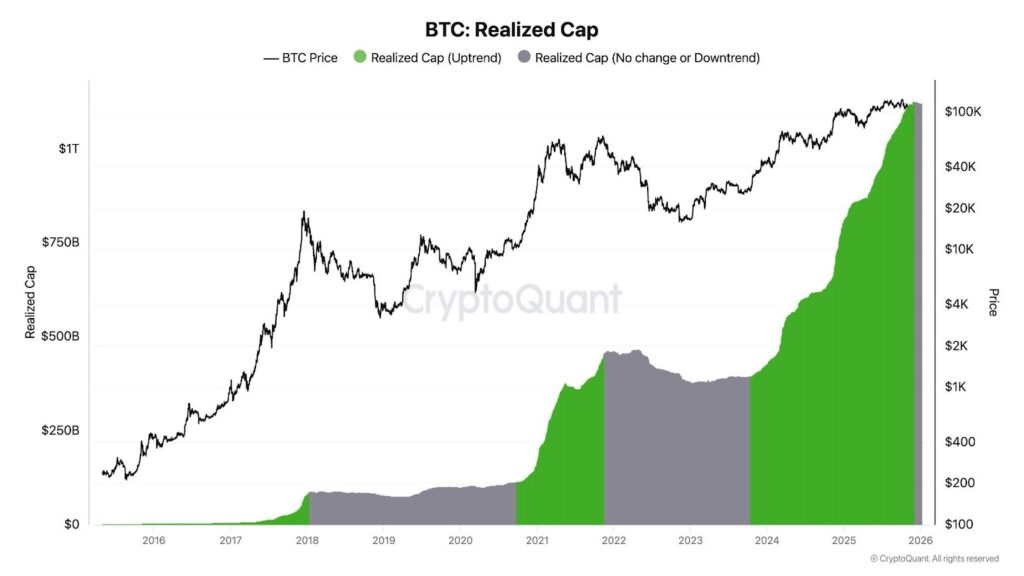

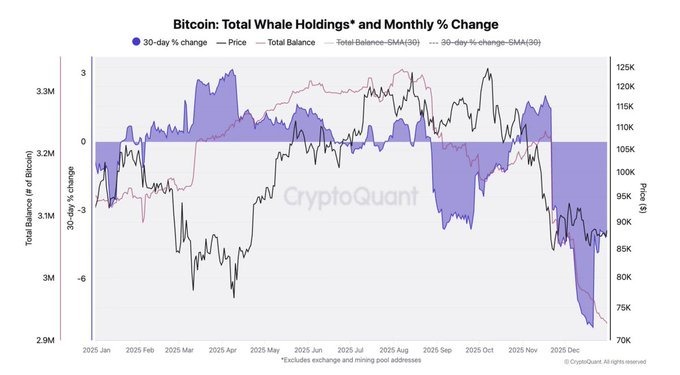

Supporting that idea, @cryptoquant_com data shows that Bitcoin whale holdings are actually declining, not rising. This contradicts the popular belief that whales are quietly accumulating. So far, the “big buyers” have not really stepped in.

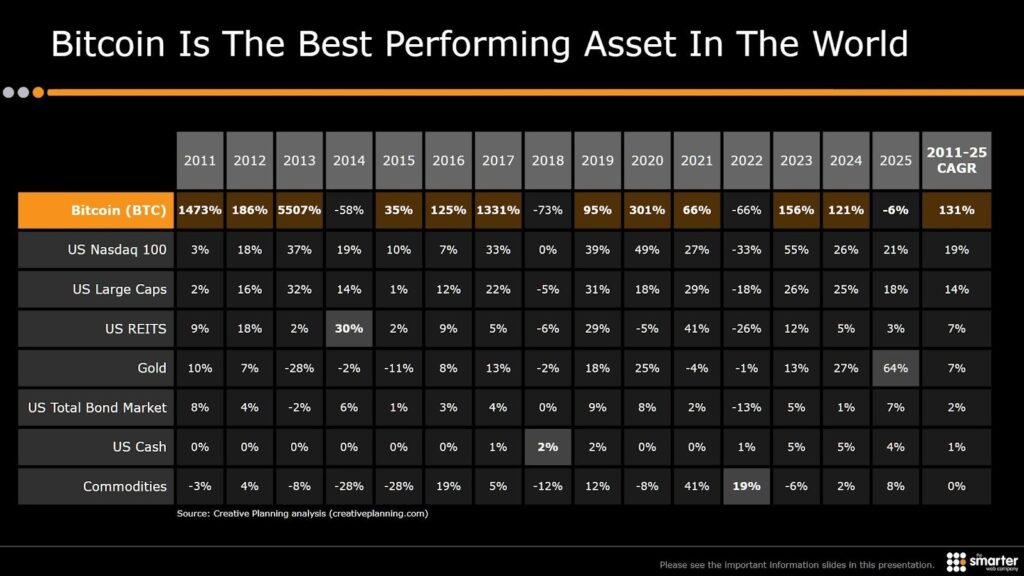

At the same time, the historical pattern haunts everyone: Bitcoin has averaged around 100% returns in the year after a down year.

Since 2025 saw a 6.36% drop for Bitcoin, the big question is simple: will 2026 repeat the pattern, or will this cycle be different?

Altcoins, infrastructure, and project drama

The week also brought heavy movement in altcoins and protocols.

On Solana, two opposite signals appeared:

- SOL Strategies reported selling 3,503 SOL in December, leaving them with around 523,000 SOL. That is a trim, not an exit.

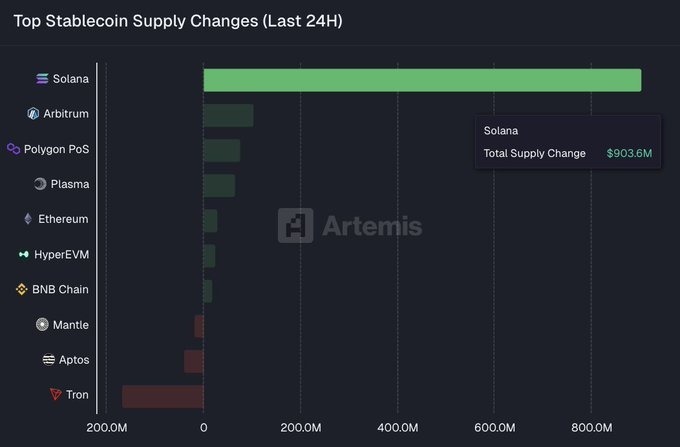

- At the same time, stablecoin supply on Solana jumped by more than $900 million in just 24 hours, according to Artemis. That inflow shows that users and capital still see Solana as a key place for stablecoins and DeFi, even if some funds derisk on SOL itself.

Zcash (ZEC) had real internal drama:

- Core Zcash developers announced a mass resignation after a conflict with the board.

- They formed a new company to continue building privacy technology outside the current ZEC structure.

- The price of ZEC fell after the news.

- Soon after, these former developers revealed cashZ, a new privacy-focused wallet, joking that they just “moved the letter Z” and now it is a new project. Behind the joke is a serious signal: talent is leaving the old structure and starting fresh elsewhere.

Another warning story came from Celestia (TIA).

TIA is now a textbook example of why you do not “catch a falling knife” in crypto. The coin:

- Dropped 72% from its peak at $21 to $6 at the start of 2025.

- Then crashed another 90% down to $0.58.

This is a brutal collapse and a reminder that sharp dips can still go much lower.

On the infrastructure and venture side:

- a16z crypto invested $15 million in the Babylon Project, which is building trustless Bitcoin vaults and expanding the use cases of the BABY token. This is one more step toward more complex financial layers on top of Bitcoin.

- Tether Gold (XAU₮) launched a new unit on-chain called Scudo, where 1 Scudo = 1/1000 of one XAU₮. The goal is to make gold-backed assets easier to use in daily transactions. The announcement was repeated more than once, underlining how important Tether wants this product to look.

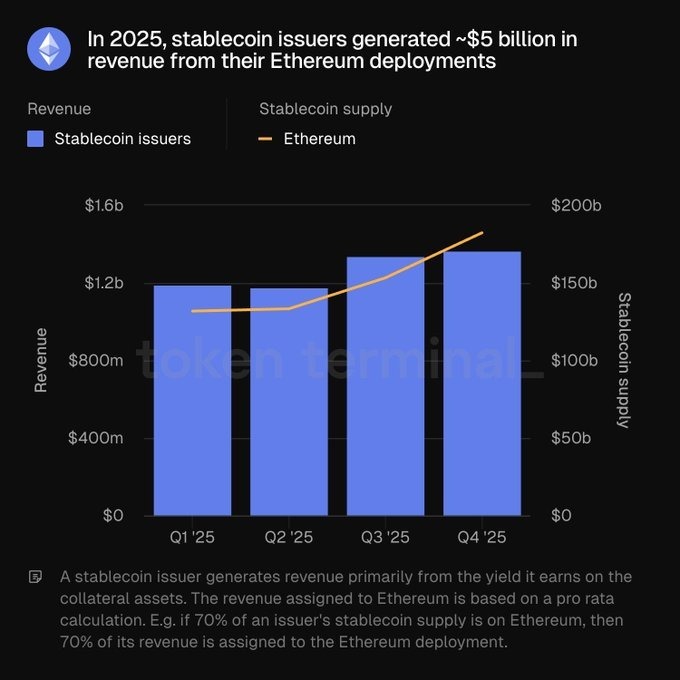

- Stablecoin issuers as a group had a huge year in 2025: they made around $5 billion in revenue from deploying their coins on Ethereum, according to Token Terminal. Stablecoins are not just “digital dollars”; they are a massive cash machine for issuers.

For big corporate players:

- Ripple confirmed it has no plans for an IPO right now. They said the reasons are:

- A strong balance sheet.

- A focus on growth instead of going public.

- Goldman Sachs released an analysis of Coinbase. They see Coinbase’s move to diversify revenue away from pure trading as a partial shield against market volatility. But they also warn that:

- Rising competition and

- Lower interest rates could slow growth in 2026.

The upgrade decision depends heavily on long-term opportunities from prediction markets and tokenization, and on how fast regulation clears the way for institutions.

Ethereum, prediction markets, and network health

Ethereum had two important stories:

- Vitalik Buterin said that Ethereum should be like Linux or BitTorrent: open-source, decentralized at its core, globally scalable, and trusted by companies and institutions. This is his vision of Ethereum as public infrastructure, not just a speculative asset.

- The Ethereum validator exit queue collapsed to almost zero, just 32 ETH waiting to exit, the lowest since July. This happened while demand for staking rose, which suggests rising confidence in the network and less desire to leave.

Prediction markets also made progress:

- Polymarket and Parcl announced a partnership to create real estate prediction markets. They will use Parcl’s house price indices to let users bet on home values across big cities around the world. This brings together real-world housing data and on-chain prediction markets, creating a new way to price and understand the housing market.

Security and personal risk in crypto

Finally, not all danger is on charts or in laws.

There is a worrying rise in “wrench attacks” against crypto holders, especially in Europe and Asia. These are physical attacks where criminals use force or threats to make victims hand over wallet keys or transfer coins.

The simple takeaway: crypto security is no longer just technical; it is also physical. Cold wallets and good opsec are not enough if someone is willing to use violence.

Where this leaves the market

Putting everything together, this week painted a picture of a market that is structurally stronger but emotionally tired:

- Bitcoin is historically oversold, with big entities holding large stacks, but whales are not yet buying aggressively and on-chain flows are quiet.

- Regulation is moving forward but in a messy way: South Korean confiscation, US bills, EU rejection, Japanese tax cuts, US banks vs stablecoins.

- Macro remains unstable: huge money printing in China, delayed US data, possible massive tax refunds, and a major legal overhang on Trump’s tariffs, plus war concerns in Ukraine.

- Altcoins and projects are splitting into winners and losers: serious Solana stablecoin demand vs TIA collapse, Zcash dev exit, and new plays like Babylon, Scudo, and real estate prediction markets.

The big open question is simple:

If Bitcoin usually doubles in the year after a red year, and 2025 was slightly negative, will 2026 respect the pattern, or will this finally be the cycle where history breaks?

For now, the data suggests sideways, cautious, and highly political, even while the underlying crypto infrastructure keeps growing quietly in the background.

This article is for information and educational purposes only and does not constitute financial advice, investment advice, or trading advice. Crypto markets are high-risk and highly volatile, and you can lose some or all of your funds. Always DYOR (Do Your Own Research) and make decisions based on your own risk tolerance.

For more market explainers and guides, visit blog.millionero.com.

If you choose to trade, you can access Spot and Futures/Perpetuals on Millionero.