This week did not feel like a normal crypto week. Not because of one big candle on a chart, but because of something deeper: crypto kept moving closer to the center of the financial system. Regulators shifted their tone. Wall Street pushed tokenization forward in public. Stablecoins crept into everyday payouts. And the macro background, rates, debt, and liquidity, kept shaping the way investors think about risk.

Regulation: the wind is changing direction

The strongest regulatory signal this week was about people, not paperwork. Caroline Crenshaw, one of the most aggressive internal critics of crypto at the SEC, is set to leave her role on January 18. That matters because it changes the internal balance and can affect how aggressively the SEC chooses to fight the industry in the next phase. Trump has not announced the replacement yet, but the simple market takeaway is that the SEC may become less hostile in practice.

On another front, the CFTC pulled back older crypto guidance, calling it outdated and not fit for today’s market. That sounds like a small administrative move, but it often signals something bigger: a regulator clearing old language to make room for newer, cleaner rules.

A second message came through in a very direct way: ICOs and many network-linked digital assets may not be treated as securities, while tokenized securities remain under SEC oversight and other digital categories move toward the CFTC. If that framing becomes policy, it would reshape where legal responsibility sits and reduce the “one-agency controls everything” approach.

In the same week, another institutional green light landed: U.S. national bank regulators signaled that banks can now buy and hold Bitcoin on behalf of clients. That is not a meme. That is the banking system quietly saying: this is allowed activity.

Wall Street’s onchain turn: tokenization goes from talk to process

Crypto spent years trying to get traditional finance to take blockchain seriously. This week showed something different: traditional finance is pulling blockchain into its own machinery.

A historic headline was the SEC approving DTCC’s plan to tokenize stocks, bonds, and Treasuries. DTCC is part of the settlement backbone of U.S. markets. When tokenization enters that world, the story becomes less about hype and more about efficiency: faster settlement, clearer tracking, and smoother market operations.

Then came an even more concrete move: JPMorgan issued a fully tokenized bond on Solana, used for Galaxy, with a $50 million short-term bond created, distributed, and settled onchain. This is the type of event that tells institutions: it can be done, and it can be done at scale.

Even Jamie Dimon’s tone reflected the shift. The message was not “crypto is the future.” It was more blunt: huge transfer volumes already exist, and blockchain is cheap and fast. JPMorgan’s direction now looks simple: tokenization is becoming a product strategy, not a PR debate.

And as this onchain bridge grows, Jupiter made its own statement: it hired a major Wall Street name, bringing in a digital-asset strategy leader from KKR, while also pointing to massive scale, crossing the $1 trillion level in yearly managed volume. The core idea is clear: onchain finance is recruiting from the old world, because it is trying to become part of the new world’s default.

Stablecoins: from trading tool to payout rail

One of the biggest “real use” stories this week was simple: YouTube enabled stablecoin payouts for creators in the U.S. through PayPal. That is a mainstream platform turning stablecoins into a normal payout option. It moves stablecoins away from “exchange money” and closer to “income money.”

At the same time, USDT gained official recognition in Abu Dhabi (ADGM) across multiple major networks, including Aptos, Celo, Cosmos, NEAR, Polkadot, Tezos, TON, TRON, and more. The region is clearly trying to position itself as a regulated hub for digital payments and stablecoin usage.

This is the stablecoin trend in one line: the world is slowly treating stablecoins as payment infrastructure, not a crypto niche.

Macro: rate cuts, debt pressure, and the liquidity argument

This week also came with a strong macro anchor: interest rates were cut by 25 basis points. The market reaction was always going to depend on the tone around inflation risk and whether policymakers signal caution or support.

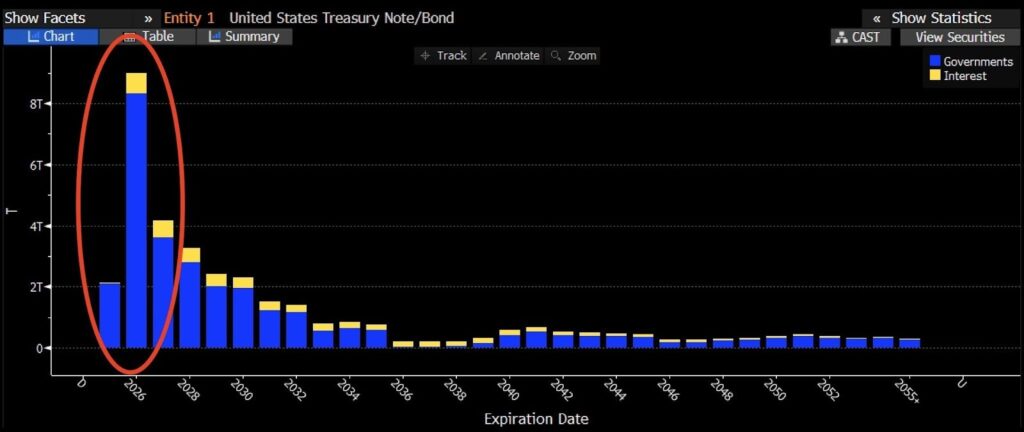

The bigger macro pressure is waiting in 2026. The United States is expected to face around $8 trillion in refinancing needs. That number changes how markets think because it raises the same question again and again: how do you refinance that much without breaking something? Lower rates help. Liquidity programs help. And if growth weakens, policymakers often find ways to keep the system moving.

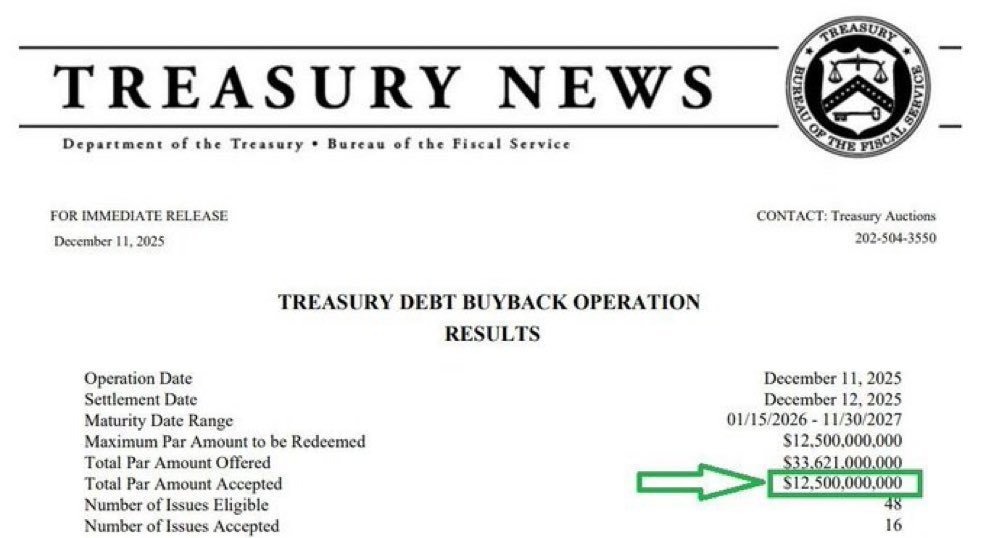

Debt management also came into focus. The U.S. Treasury executed another $12.5 billion debt buyback operation. Separately, a large $40 billion buyback narrative circulated as a “liquidity returning” story, framing it as cash moving back into institutions and pushing investors toward higher-return assets.

And then, almost like a simple sentence that summarizes why people keep watching all of this, Warren Buffett’s quote landed hard: governments naturally push currencies down in value over time. Inflation is not always loud, but it is persistent. That is the background logic behind why people keep looking for assets that feel harder than paper.

Bitcoin’s corporate chapter: still real, but not automatic

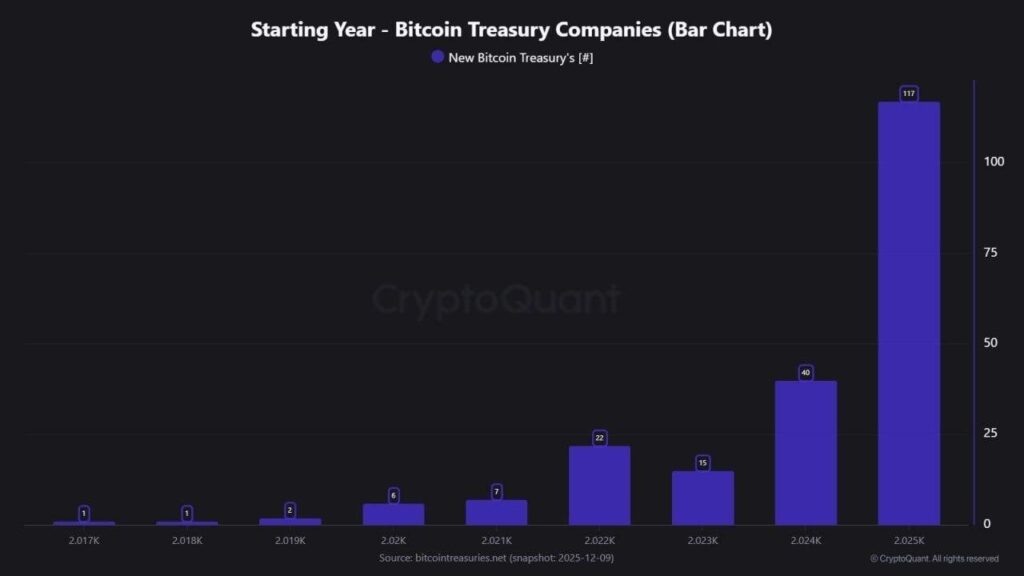

Bitcoin adoption by corporations had a strange shape this year. The numbers suggest that 2025 started strong and ended soft.

A total of 117 new companies added Bitcoin to their reserves, but the pace collapsed late in the year: 53 companies joined in Q3, then only 9 companies joined in Q4. That is not a small change. It shows corporate demand is sensitive. It depends on volatility, credit conditions, and confidence.

At the same time, public companies now hold more than 5% of total BTC supply, and Strategy alone is around 3%. That’s a sign of real structural adoption, but also a sign of concentration.

Corporate buying did not disappear either. Strive announced a $500 million preferred share raise to buy more Bitcoin, building on a position of 7,525 BTC.

And on the research side, JPMorgan analysts projected Bitcoin could reach $170,000 in 2026, using a store-of-value comparison with gold.

So the corporate picture is mixed but clear: Bitcoin is now a treasury asset class, but companies are still cautious when conditions feel unstable.

Index products: a quiet shift in how investors want exposure

Another major theme was indexes.

Bitwise defended Strategy index after an MSCI-related proposal suggested exclusion. Bitwise’s message was simple: indexes should remain neutral, and rule changes can hurt investors who want clean exposure to digital assets.

In the same week, the “index era” moved forward with a big milestone: the Bitwise 10 Crypto Index product (BITW) began trading on NYSE Arca, tracking a basket that includes BTC, ETH, XRP, SOL, ADA, LINK, LTC, SUI, AVAX, and DOT, with $1.25 billion in assets.

And a bigger claim sat behind that: crypto index funds may become the “big game” in 2026, because the market is too complex for many investors to pick single winners. Many will prefer the basket.

Onchain signals: flows, whales, and who made money

A week like this also had strong “under the surface” activity.

Avalanche (AVAX) saw the highest stablecoin inflows in a 24-hour window, suggesting liquidity was moving onto that network. This type of flow often reflects positioning: stablecoins arriving before deployment.

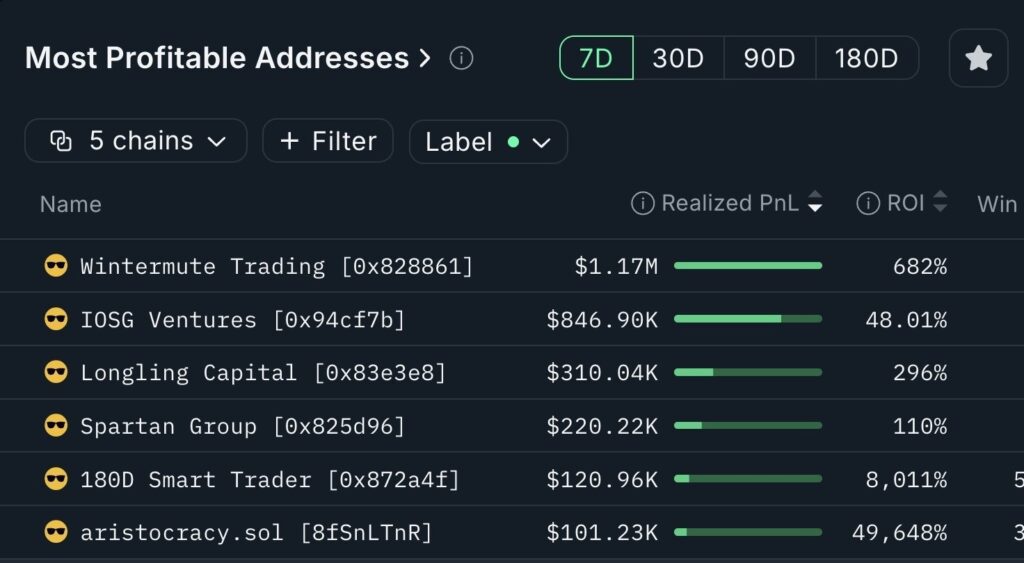

Smart money activity also looked active. Wintermute led weekly “smart money” rankings with $1.17 million in realized profit, followed by IOSG Ventures with $847k, with strong showings by Longling Capital and Spartan Group too. The message is not “copy them.” The message is: big players were taking decisive trades.

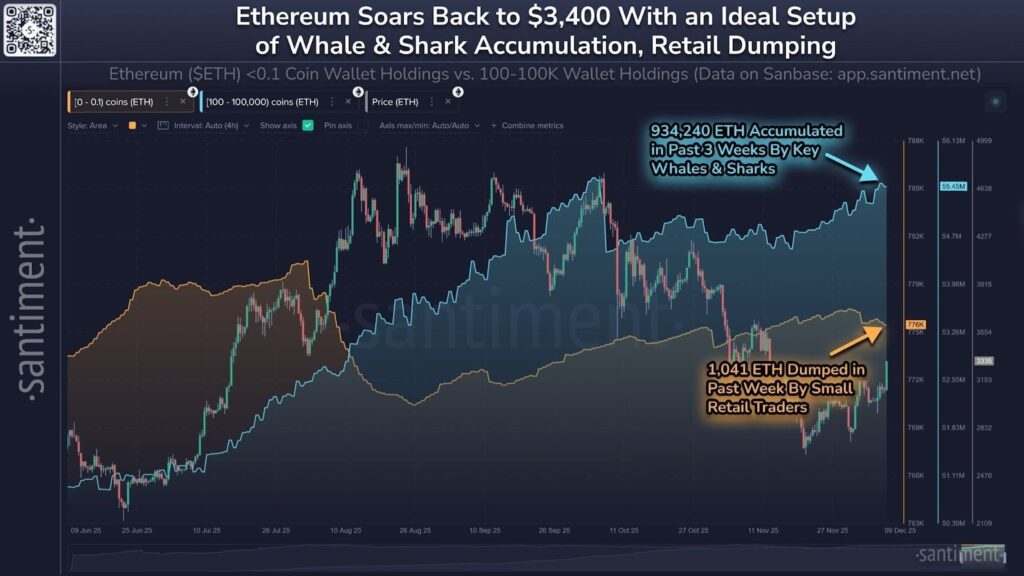

Ethereum positioning was also sharp. Large holders accumulated about 934,240 ETH (around $3.15 billion) over three weeks, while small traders barely added. ETH rose about 8.5% to around $3,400 in that period. It was a classic split: big money buying, smaller money hesitating.

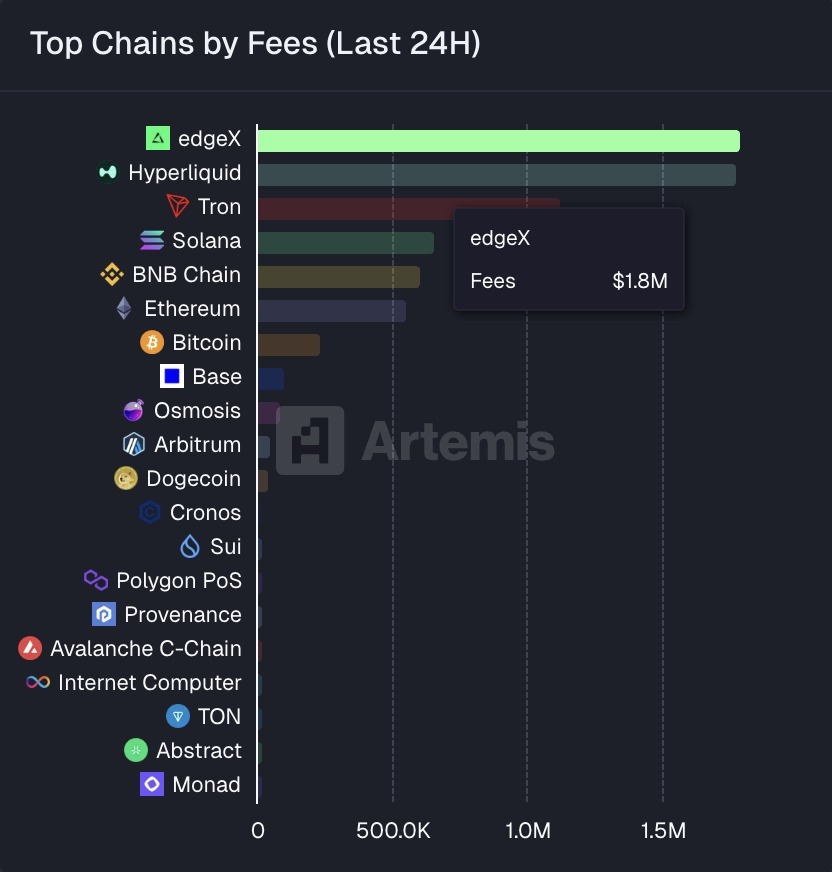

And for pure usage, EdgeX and Hyperliquid led networks in daily fees at $1.8 million each, showing where activity and demand were concentrated.

The “cycle is changing” narrative returns again

Grayscale argued that Bitcoin may be drifting away from the old four-year halving rhythm. The idea is simple: institutions now dominate long-term flow through ETFs, corporate treasuries, and large hedging structures. That could make Bitcoin behave more like a macro asset, more tied to liquidity, rates, and institutional risk appetite than retail cycle psychology.

This does not mean the market gets calmer. It means the drivers change.

Politics and policy: the setup for 2026

Finally, politics stayed close to the market.

Trump said he is entering the final round of meetings to pick the next Fed Chair. Even before a name appears, markets react to the idea that future policy leadership could shift the tone around inflation tolerance, rates, and liquidity.

Trump also claimed that personal income tax could be removed in the future, funded by tariffs, and announced a plan for $12 billion in support for farmers affected by trade policies. It is a headline that mixes fiscal policy, trade politics, and economic pressure, exactly the kind of mix that moves sentiment.

Outside the U.S., Argentina discussed allowing banks to offer crypto trading and custody under stricter rules, which could pull crypto deeper into formal banking channels.

And in Congress, Senator Cynthia Lummis said she hopes small Bitcoin payments could be freed from taxes by next year, an attempt to make BTC spending feel less like a reporting burden and more like normal usage.

Closing thought

This week’s story was not just “crypto news.” It was the slow merging of two worlds.

When DTCC talks tokenization, when JPMorgan settles onchain, when YouTube pays out in stablecoins, and when regulators start cleaning up old guidance, crypto stops being a parallel universe. It starts becoming part of the base layer.

And once something becomes infrastructure, the market stops asking if it is “real.” The market starts asking who controls it, who benefits, and how fast it spreads.

This article is for general information only and should not be taken as financial, investment, or legal advice. Crypto assets are volatile and can involve significant risk. Always do your own research and consider your risk tolerance before making any decision.

If you want to keep learning, you can explore more market explainers and guides on blog.millionero.com. When you’re ready, you can access spot and futures markets on Millionero, always with a clear plan and strong risk management.