What Changed Over the Weekend

Crypto, regulation, and market structure

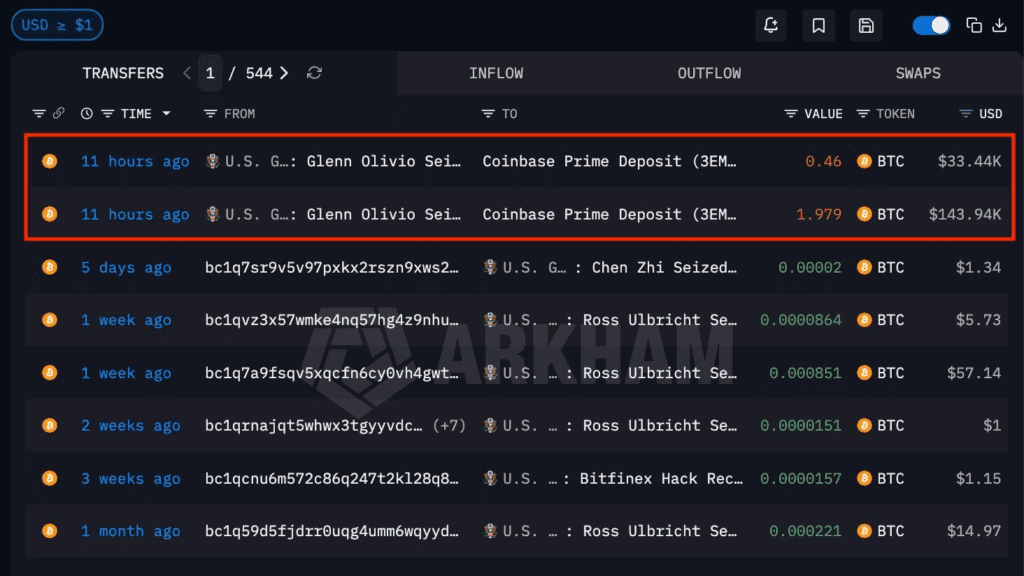

Over the weekend, crypto also had its own run of important updates. The US government moved 177.4 thousand dollars worth of Bitcoin to Coinbase (Prime). The funds were seized from Glenn Olivio, a steroid distributor who was indicted in 2025. This was the first movement of this kind in more than a month, which immediately raised one direct question in the market: whether this Bitcoin is now being prepared for sale.

At the same time, the CFTC moved closer to becoming the main regulator of the crypto market. The Commission is working to strengthen its role as a core regulator for digital assets while the United States continues to deal with competition between agencies over who will lead this sector.

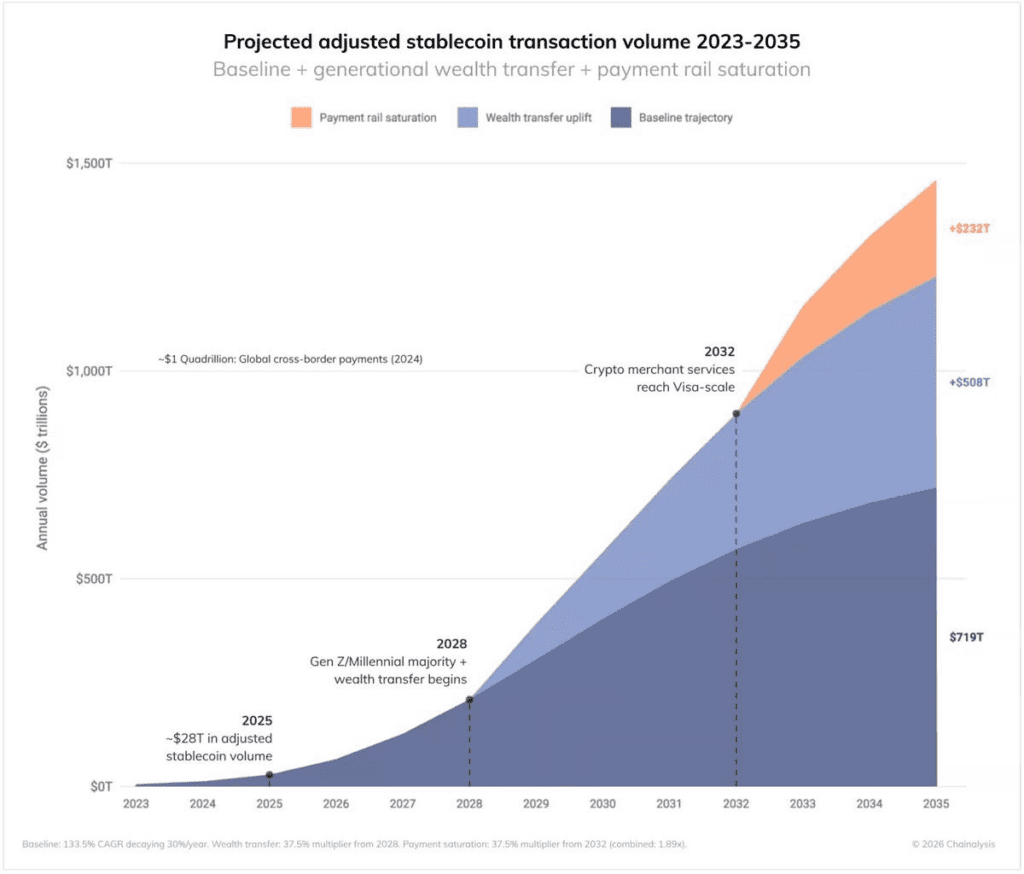

Another major long-term point came from the stablecoin market. A new projection shows stablecoin trading volume could reach $719 trillion by 2035 through organic usage growth alone. It also predicts that, with intergenerational wealth transfer and faster payment adoption, that number could climb to $1.5 quadrillion, a level that would move beyond current global payment systems.

There was also a quieter but important regulatory development in traditional finance. The Federal Reserve asked banks to clarify how exposed they are to the private credit market, while the US Treasury asked insurance companies the same thing. These requests were said to be moving through routine examination channels, not through a formal investigation. That usually points to growing concern inside regulatory bodies, but without full clarity yet on the size of the risk.

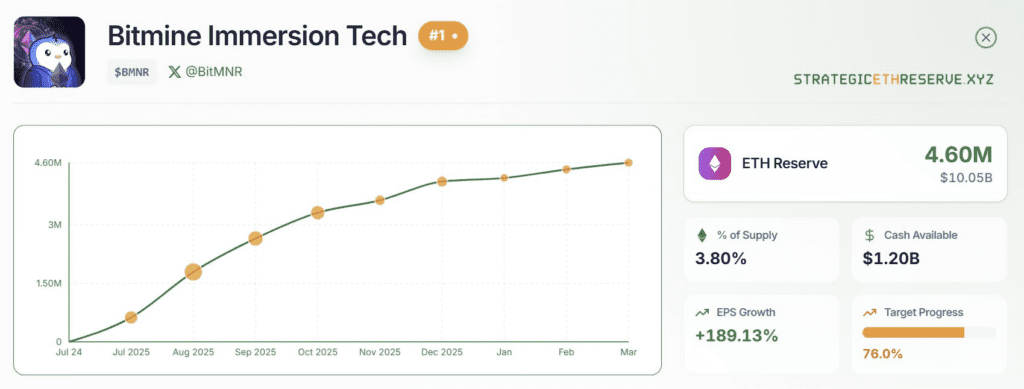

On the corporate side, BitMNR now owns about 3.8% of the circulating supply of Ethereum, and the value of that holding has reached around 10 billion dollars.

US-Iran talks broke down and pressure rose fast

The main weekend story, however, was the complete collapse of the latest peace effort between the United States and Iran. After 21 hours of intense talks, the first direct dialogue between the two sides since 1979 ended without an agreement. The broad message coming out of the weekend was simple: hopes likely collapsed, the talks hit a dead end, and the risk of war returning moved sharply higher.

The main dispute was clear. Iran refused to give an official commitment against developing nuclear weapons. That became the wall the talks could not get past. JD Vance then said Iran had chosen to reject the American conditions and had wasted this historic chance. Reports also said there were no plans for further rounds in the near term, and later updates repeated that there were currently no plans for additional talks.

As that breakdown became clearer, the tone from Washington hardened. During the weekend, there were already reports that Trump had proposed a naval blockade on Iran as a way to squeeze its oil exports and pressure major buyers such as China and India. The idea came after stalled peace talks and was framed as a way to use naval force as economic pressure. It was also described as similar to Trump’s earlier strategy against Venezuela, where reducing oil flows was central to weakening the economy. At that stage, it was still being described as a proposed option rather than an official decision, but the tone was already escalating.

Oil became the center of the global story

By Sunday, oil had become the focal point of everything. Trump said, “The price of oil and gas could be lower before the midterm elections, or maybe a little higher… Frankly, gas prices haven’t gone up as much as I thought they would.” That comment landed just hours before oil futures reopened.

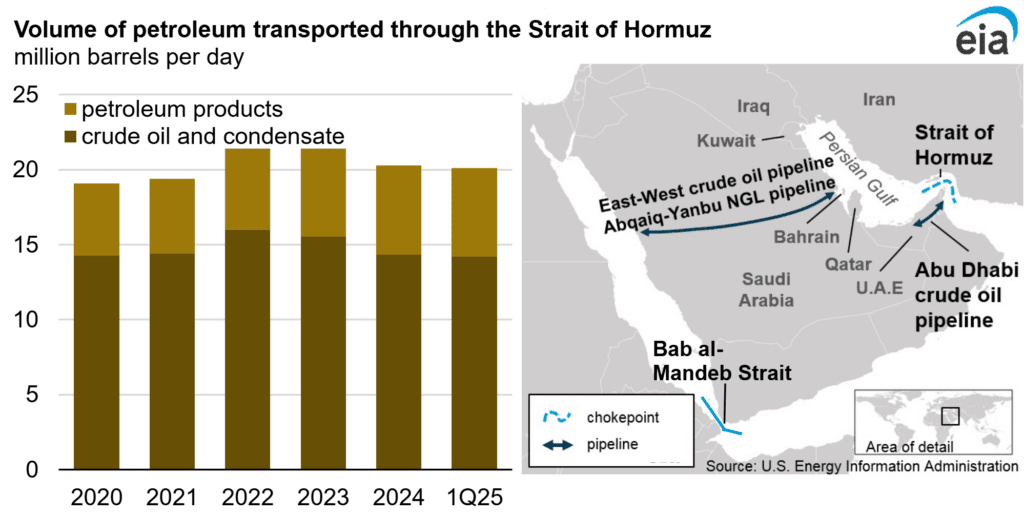

Then the situation moved again. The United States announced that it would begin blocking the Strait of Hormuz itself. The US Navy began the process of a blockade of the strait, meaning the United States and Iran were now effectively competing over the same crucial waterway. The idea behind the move was presented as gaining control of Hormuz and then allowing traffic to flow again later. But the same weekend analysis also warned that, if that goal could be achieved at all, it would likely be a long process that could restrict traffic for at least another 2 months. As diplomacy appeared to fail, reopening the Strait of Hormuz became the top US priority in the Iran war.

Soon after that, the US Military said the Strait of Hormuz blockade would begin at 10 AM ET on Monday. Another update said the military blockade would begin in 16 hours, putting a clear clock on the next phase of escalation.

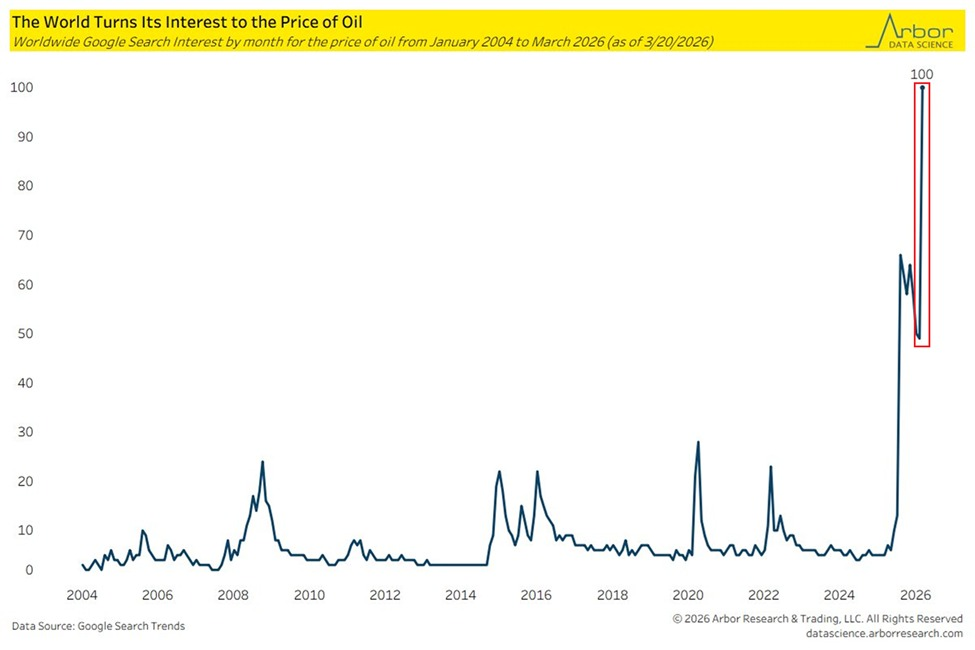

The whole world reacted to oil immediately. Google search interest for “price of oil” rose to its highest level on record in data going back to 2004. That beat the peaks from the 2022 Russia-Ukraine war and the 2008 Financial Crisis by 300%. It was also 235% higher than the 2020 pandemic spike, when oil briefly turned negative.

Search interest for “Strait of Hormuz” also hit an all-time high, rising 300% above the June 2025 levels seen during the 12-Day War between Israel and Iran, when the market had already feared a Hormuz closure. The global energy crisis was suddenly back in full view.

Source: Google Trends

Markets opened into a new risk environment

By the time markets moved into the new week, the reaction was immediate. Since BTC is always open, it had already rejected $74k on the weekend.

US stock market futures opened sharply lower after the peace talks ended without a deal. The early moves were:

- S&P 500: -1.0%

- Nasdaq 100: -1.3%

- Dow Jones: -1.0%

- WTI Crude: +10.0%

- Brent: +8.5%

- Natural Gas: +2.0%

At the same time, US oil prices officially surged 10% at the open, rising above $105 per barrel.

The conflict tone also became more severe. Trump was considering resuming “limited military strikes” in Iran in addition to the blockade of the Strait of Hormuz. He also stated that a full-fledged bombing campaign remained possible, though seen as less likely. Another option on the table was a temporary blockade while allies were pressured to take responsibility for a longer military escort through Hormuz in the future. At the same time, reports clarified that Trump still remained open to a diplomatic solution, even while again threatening Iran’s infrastructure. He said, “I would hate to do it, but it’s their water, their desalinization plants, their electric-generating plants, which are very easy to hit.”

Iran also answered publicly after the talks. Foreign Minister Araghchi said that, in the highest-level talks in 47 years, Iran engaged with the United States in good faith to end the war. He said that, when both sides were only inches away from an “Islamabad MoU,” the process ran into maximalism, shifting goalposts, and blockade, adding that “Zero lessons earned.”

The world woke up to major news because both sides had returned home, Iran was refusing to reopen the Strait of Hormuz without a permanent peace agreement, and the United States had called that bad news for Iran. Iran’s Speaker of Parliament also said the United States had failed to gain Iran’s trust during negotiations. With no more talks currently planned, the question now is whether the next move is a harder diplomatic push or a deeper military escalation.

That matters far beyond geopolitics because inflation is already moving. US CPI inflation had already risen from 2.4% to 3.3%, and that a further escalation in the Iran war could push inflation to 4.0%+ under the model being used in the market commentary. In other words, the weekend did not just raise military risk. It also directly changed the inflation outlook, the growth outlook, and the policy backdrop going into the new week.

What the United States Now Has to Watch This Week

Monday: the market reaction and Existing Home Sales

The week begins with markets still processing the failed negotiations and the Hormuz blockade. One key market event was listed for today at 6 PM ET, focused on how markets react to the failed negotiations and the Hormuz blockade. The calendar also includes March Existing Home Sales data on Monday.

By itself, Existing Home Sales is a housing release, but this week it sits inside a much bigger macro story. Housing is one of the most rate-sensitive parts of the economy, so this report can help show how demand is holding up while uncertainty rises, oil prices jump, and financial conditions tighten through sentiment even before any new policy move arrives.

Tuesday: March PPI Inflation data

The most important data point early in the week is March PPI Inflation data on Tuesday. This release matters even more now because energy is back at the center of the inflation story. If oil holds above $105 and the Strait of Hormuz remains disrupted, producer costs can rise further. That matters because producer prices often feed into broader inflation pressure later.

Markets are already dealing with the idea that CPI moved from 2.4% to 3.3%. If PPI comes in firm, it would reinforce the view that inflation pressure is not fading cleanly and could become harder for the Federal Reserve to ignore, especially if the war drives another round of energy price increases.

Wednesday: Beige Book and the growth picture

The weekly setup also points to Wednesday’s “Beige Book” economic report. This matters because the market is not only worried about inflation. It is also worried about weaker growth. One of the clearest themes going into this week is that inflation is rising because of oil prices and the war, while the economy is also showing a clear slowdown in growth.

That is a difficult mix. If the Beige Book shows slower activity across districts while price pressure stays elevated, it would support the idea that the economy is losing momentum at the same time inflation risks are rebuilding.

Thursday: Philly Fed Manufacturing Index and Initial Jobless Claims

Thursday carries two important releases: the Philly Fed Manufacturing Index and Initial Jobless Claims data.

The Philly Fed Manufacturing Index will matter because it gives a fast look at industrial conditions and business activity. This week, the number will be watched as a read on whether the slowdown in growth is spreading.

Initial Jobless Claims is the key labor market number in the lineup. If claims rise, it would suggest labor market conditions are softening. If claims stay low, it would suggest the labor market is still holding up better than growth fears imply. Either way, this report matters because it helps shape the balance between inflation worries and employment conditions, which is exactly the balance the Federal Reserve has to judge when thinking about future rate decisions.

Fed speakers and the policy path

This week is also heavy on Fed communication. There will be 10 Fed Speaker Events This Week. Officials will have many chances to shape expectations.

The market is clearly waiting for any hint about the next move. Right now, the setup is uncomfortable. Inflation pressure is rising again because of oil and war risk, but growth is slowing. That leaves the Federal Reserve facing a more difficult policy path. If inflation risk becomes more persistent, the case for easier policy weakens. If growth and labor data soften faster, the pressure to support the economy will grow. For now, expectations appear to be centered on caution, close monitoring, and a very sensitive reaction to every new headline.

One summary of the week captured the mood well: the geopolitical tension between America and Iran is frightening the global economy, markets are on edge, inflation is rising because of oil and the war, and growth is slowing at the same time. That is why the US data and the Fed tone matter so much this week.

It is also worth keeping the broader conflict timeline in view. Today marks day 44 of the Iran War. That alone explains why every inflation number, labor market signal, and Fed comment now carries more weight than usual.

Crypto Unlocks This Week

Xpla (CONX)

Date: April 15, 2026

Unlock Value: 15.95M USDT

% of Circulating supply: 1.52%

Number of Tokens: 1.32M CONX

Arbitrum (ARB)

Date: April 16, 2026

Unlock Value: 10.65M USDT

% of Circulating supply: 1.81%

Number of Tokens: 96.00M ARB

deBridge (DBR)

Date: April 17, 2026

Unlock Value: 9.08M USDT

% of Circulating supply: 12.90%

Number of Tokens: 618.33M DBR

YZY (YZY)

Date: April 18, 2026

Unlock Value: 6.36M USDT

% of Circulating supply: 4.67%

Number of Tokens: 20.83M YZY

Rain (RAIN)

Date: April 13–20, 2026

Unlock Value: 75.67M USDT

% of Circulating supply: 1.99%

Number of Tokens: 9.50B RAIN

Solana (SOL)

Date: April 13–20, 2026

Unlock Value: 38.22M USDT

% of Circulating supply: 0.08%

Number of Tokens: 467.97K SOL

Canton (CC)

Date: April 13–20, 2026

Unlock Value: 28.06M USDT

% of Circulating supply: 0.50%

Number of Tokens: 191.71M CC

Official Trump (TRUMP)

Date: April 13–20, 2026

Unlock Value: 17.72M USDT

% of Circulating supply: 2.72%

Number of Tokens: 6.33M TRUMP

Worldcoin (WLD)

Date: April 13–20, 2026

Unlock Value: 10.78M USDT

% of Circulating supply: 1.14%

Number of Tokens: 37.23M WLD

Dogecoin (DOGE)

Date: April 13–20, 2026

Unlock Value: 8.66M USDT

% of Circulating supply: 0.06%

Number of Tokens: 95.06M DOGE

Closing View

The weekend changed the tone of the entire week. Crypto saw a fresh government Bitcoin transfer, a stronger regulatory push from the CFTC, a huge long-term stablecoin volume projection, a quiet regulatory focus on private credit exposure, and a major Ethereum concentration update from BitMNR. But the much larger move came from the collapse of US-Iran talks, the move toward a Strait of Hormuz blockade, the jump in oil, and the sudden pressure that now places on inflation, growth, and Federal Reserve expectations.

That is why this week’s US calendar matters so much. Existing Home Sales, PPI Inflation, the Beige Book, the Philly Fed Manufacturing Index, Initial Jobless Claims, and a heavy run of Fed speaker events are no longer routine entries on a schedule. They now sit inside a market that is trying to price war risk, energy shock, inflation pressure, labor market resilience, and the next policy choice from the Federal Reserve all at once.

This article is for informational purposes only and should not be considered financial advice. Always do your own research, think carefully about your risk tolerance, and follow the market with caution. For more crypto explainers, market updates, and weekly recaps, visit blog.millionero.com. When you are ready to trade, you can explore the market on Millionero Spot for direct buying and selling, or use Millionero Perpetual Futures if you are looking for more advanced trading tools.