While global attention remains fixed on the US-Iran war and the broader instability spreading across the Middle East, another major geopolitical risk is quietly building in Asia. This time, the pressure is once again centered on Taiwan.

China has sharply increased military activity near the island. Taiwan’s defense ministry reported that 26 Chinese military aircraft entered Taiwan’s Air Defense Identification Zone, while 7 Chinese navy ships were also detected around the island. According to reports, this is the largest Chinese military presence near Taiwan in weeks.

For now, this is not a war. But markets do not need an official war to start pricing risk. When a region as important as Taiwan begins to show signs of renewed military pressure, the global economy has to pay attention.

Why the Timing Matters

The timing of this rise in activity is especially important. Global geopolitical risk is already elevated because of the conflict involving the US and Iran, oil market instability, and a broader sense that the world is becoming less predictable. In that environment, even a regional military escalation can have an outsized market effect.

China had reduced activity around Taiwan earlier in March, which gave the impression of a temporary cooldown. That now appears to have changed. The return of flights and naval operations suggests that pressure in the region is rising again, and traders know that Taiwan is one of the few geopolitical flashpoints that could quickly become a true global macro event.

This is because Taiwan is not just politically important. It is economically critical.

Taiwan’s Central Role in the Chip Industry

Taiwan sits at the heart of the global semiconductor supply chain. The island produces more than 60% of the world’s semiconductors and over 90% of the most advanced chips used in AI, smartphones, data centers, and high-performance computing.

That makes Taiwan one of the most important industrial centers on earth.

TSMC alone manufactures chips for some of the biggest companies in the world, including Apple, NVIDIA, AMD, and Qualcomm. If Taiwan’s production were disrupted, the effects would not stay inside Asia. They would spread almost immediately across the global economy.

Bloomberg’s economic modeling has estimated that losing Taiwan’s semiconductor production would cut global supply of advanced logic chips by more than 60%. That would create an immediate shock for industries that now depend on constant chip access to function normally.

The first wave of pain would likely hit sectors such as AI, consumer electronics, cloud computing, automobiles, and industrial manufacturing. But it would not stop there. Once those industries slow down, the effects would move into labor markets, trade flows, corporate earnings, and financial sentiment.

This Is Bigger Than a Tech Story

It would be easy to look at Taiwan only as a semiconductor issue, but that would be too narrow. Taiwan is also deeply tied to trade and shipping routes across the Asia-Pacific region, which remains one of the busiest and most economically important areas in the world.

A serious conflict, or even a prolonged blockade, could disrupt commercial shipping, delay deliveries, raise insurance costs, and create new stress across already fragile global supply chains. After the lessons of 2020 and 2021, markets know very well how quickly supply disruptions can turn into inflation, shortages, and weaker growth.

This is why economists take the Taiwan risk so seriously.

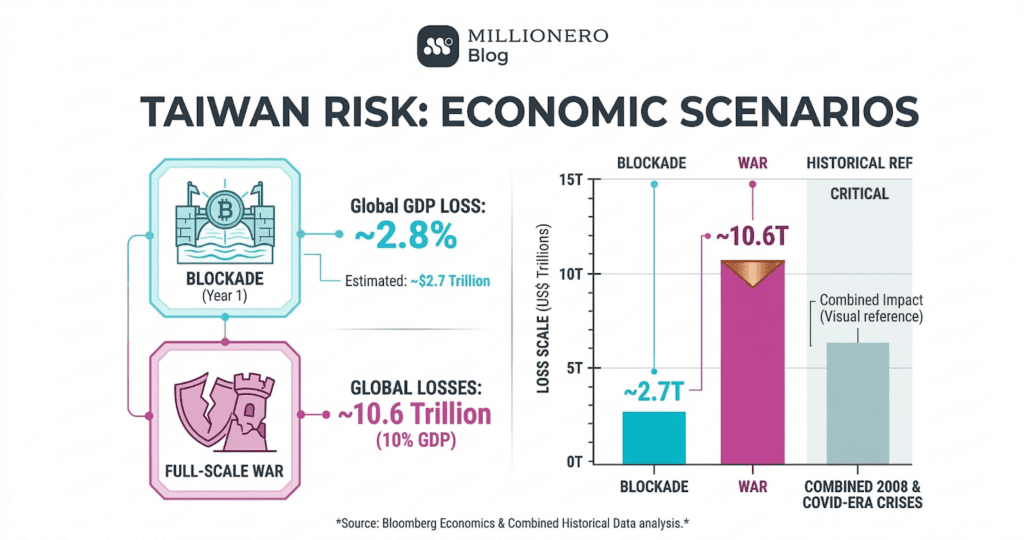

One scenario involving a Chinese blockade of Taiwan has been estimated to reduce global GDP by around 2.8% in the first year alone, equal to about $2.7 trillion in lost economic output. A full-scale war would be much worse. Bloomberg Economics has estimated that a major war over Taiwan could cause around $10.6 trillion in global losses, or roughly 10% of global GDP.

That scale of damage would be larger than the combined impact of the 2008 financial crisis and the COVID-era recession.

What Markets Would Likely Do

If Taiwan’s semiconductor output were interrupted or shipping in the region became unsafe, the market reaction would likely be immediate. Companies around the world would face shortages of critical components, especially in electronics and advanced manufacturing. At the same time, investors would likely move hard into risk-off positioning.

That usually means sharp declines in equities, spikes in volatility, stronger demand for US Treasuries, and broader stress across trade and credit markets.

There is also the China factor. China is the world’s second-largest economy and one of the biggest manufacturing hubs in global supply chains. Any major conflict involving China and Taiwan would likely raise the possibility of sanctions, export controls, and new trade restrictions. That would create another layer of damage on top of the military risk itself.

In simple terms, a Taiwan crisis would not be a local event. It would be one of the largest macroeconomic shocks the world has faced in decades.

The Bottom Line

Right now, there is no war over Taiwan. But the return of large-scale Chinese military activity around the island is a reminder that this risk has not disappeared. At a time when markets are already under pressure from war, oil, and rising geopolitical uncertainty, Taiwan remains one of the most dangerous fault lines in the global system.

For crypto, equities, commodities, and global trade, this is the kind of risk that cannot be ignored. Even without direct conflict, the market will keep watching every move closely, because if this situation ever turns from pressure into disruption, the economic consequences could be enormous.

This article is for informational purposes only and is not financial advice. Always do your own research. You can also explore more market insights on blog.millionero.com, and when you are ready, trade spot and perpetual markets on Millionero.