This past week in crypto felt like a contradiction: prices and volumes were ugly, but the long-term structure around Bitcoin and digital assets kept getting stronger. Central banks moved, politicians talked, Inflation eases, institutions built new products, and retail traders got squeezed again.

Macro and Central Banks: Liquidity Slowly Changes Direction

In the United States, inflation data came in softer than expected. November CPI (year-on-year) printed 2.7%, below the 3.1% forecast and down from 3.0% before. Initial jobless claims were 224k, exactly in line with expectations and slightly better than the previous 237k, showing the labor market is still holding up. Together, this means inflation is cooling while jobs are not collapsing, which keeps pressure on the Federal Reserve but also gives it more room to think about future rate cuts.

At the same time, unemployment ticked up to 4.6%, the highest since September 2021. So the picture is mixed: the economy is not in crisis, but the labor market is clearly softening compared to the boom years.

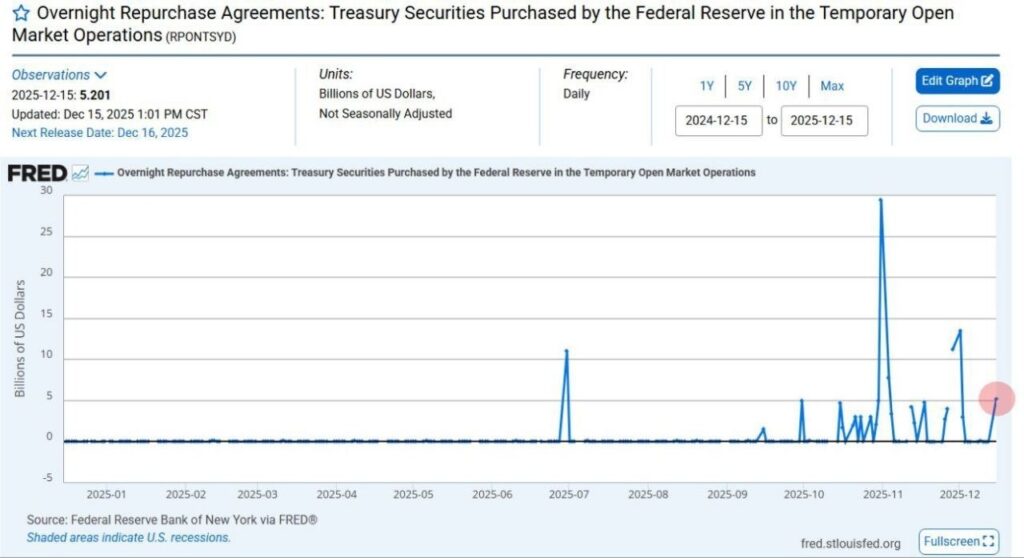

Liquidity tools also came back into play. The Fed injected $5.2 billion through its standing repo facility after years of almost no use. The commentary around it pointed to a bigger shift: quantitative tightening ending, Treasury purchases returning quietly, and old “emergency” tools becoming active again. When these “sleeping” tools wake up, it usually means the system is tighter than it looks from the surface.

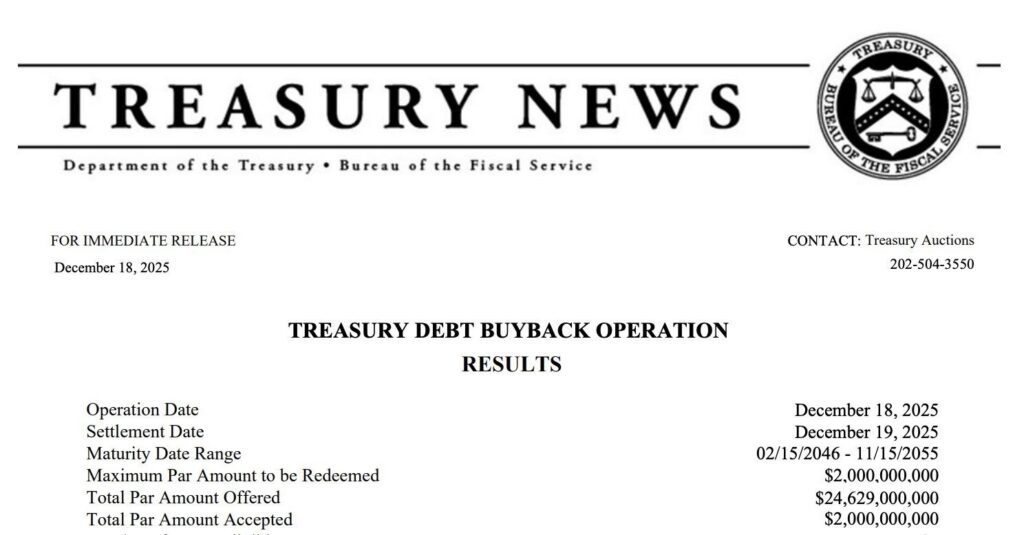

On top of that, the U.S. Treasury continued buying back its own debt, with $2 billion in repurchases in one day and roughly $6 billion over the week. It is not huge compared to the full market, but it fits the same theme: policymakers are managing liquidity much more actively.

Outside the U.S., Japan was a major story. The Bank of Japan raised rates by 25 basis points to 0.75%, the highest level in about 30 years. At the same time, the BoJ plans to slowly sell more than ¥83 trillion (about $534 billion) in ETF holdings, at a pace of about ¥330 billion per year. At that rate, the process could take more than 100 years. Traders noted that in past cycles, every BoJ rate hike has been bad for Bitcoin, because Japan is a huge holder of U.S. government debt and a key player in global carry trades.

Politics also mixed with policy. Donald Trump said the U.S. is preparing for a “historic economic boom,” pointing to what he expects to be the largest tax refund season ever and the possibility of lower interest rates. His basic story is: more liquidity plus cheaper cost of capital could create a good environment for Bitcoin and other risk assets going into 2026, though he also joked that hopefully there are no “surprises” hiding in the background.

Trump’s relationship with China also came up. He said he has a “great relationship” with President Xi Jinping, a comment that markets see as a possible sign of de-escalation between the two biggest economies. That matters for trade, inflation, and global capital flows, and therefore for risk assets, including crypto.

Finally, there was a heavy data calendar: retail sales, the delayed U.S. jobs report, CPI, the Philadelphia Fed manufacturing index, PCE inflation, existing home sales, and the Japanese rate decision all packed into one week. Put together, this week felt like the start of a new phase: less emergency tightening, more careful liquidity management, but still a lot of macro uncertainty.

The Battle for the Fed: Warsh, Hassett, and Waller

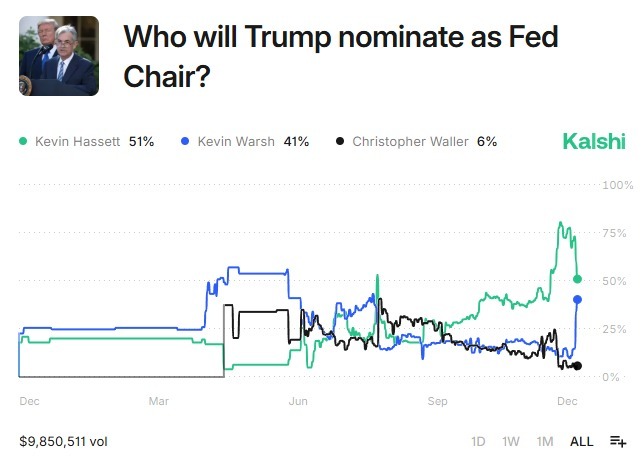

The race for the next Fed chair moved from quiet speculation to an open political story. Trump said he has narrowed his list to 3–4 candidates and praised Christopher Waller, calling him “great.” He plans to make a final decision in the coming weeks, and markets clearly understand that the next chair will shape interest rates and liquidity for years.

Christopher J. Waller, an American economist who has been a member of the Federal Reserve Board of Governors since 2020. A nominee of US President Donald Trump,

Betting and prediction markets now show rising odds for Kevin Warsh, whose chances jumped from 10% on December 9 to around 41%, while Kevin Hassett dropped from 77% to about 51%. Reports say Warsh is open to rate cuts, in line with Trump’s public wish for the policy rate to move towards 1% or even lower. Trump also raised the bar, saying the next Fed chair must consult him on interest rate decisions.

On top of that, Trump is scheduled to interview Christopher Waller, who is known as pro-crypto. So the short list is a mix of candidates who are both dovish on rates and relatively open to digital assets. For markets, this combination is important: easier money plus friendlier regulation is usually a tailwind for high-risk assets.

Regulation: From Market Structure to Stablecoins

On the regulatory front, the big message was: rules are coming, but not always in a straight line.

Trump’s administration said the U.S. is closer than ever to passing historic legislation to structure the crypto market. Clear rules for market structure would mean less legal fog, lower regulatory risk for projects, and more comfort for big institutions. The logic in the thread was simple:

At the same time, the wider U.S. market structure bill was delayed to January. Drafts are circulating, but there is still no final agreement between the industry, the White House, and both parties in Congress. So the file moves into the new year, and the short-term result is more uncertainty.

The SEC was active too. It published guidance for broker-dealers on how they can custody digital-asset securities, calling this a temporary solution until a full, long-term framework is ready. Separately, the SEC released a basic custody guide for retail investors, explaining self-custody vs. regulated custody, and the main risks of each. Both moves signal something important: regulators now assume that many people already hold crypto and need practical guidance, not just warnings.

The Bank of Canada took a clear stance on stablecoins. Its new framework will only approve high-quality stablecoins that are linked to central bank currencies, with full rules expected in 2026. The message is: stablecoins will be regulated, but the bar will be high.

In the U.S., the Blockchain Association, together with 125 crypto organizations, sent a letter to the Senate opposing an expansion of stablecoin yield restrictions in the GENIUS Act to the app layer and third-party platforms. They argued that stablecoin reward mechanisms are similar to credit card cashback, and that blocking yield sharing would hurt competition and favor the banking system.

Within crypto itself, World Liberty Financial (WLFI) community members proposed using part of their treasury unlocks as incentives to speed up adoption of the USD1 stablecoin, a classic “use rewards to drive usage and liquidity” approach.

Tokenization and the TradFi–Onchain Bridge

Another strong theme was tokenization and the slow but steady move of traditional finance onchain.

The CEO of Securitize, Carlos Domingo, said tokenization is a $400 trillion opportunity, and that Wall Street has finally started shifting onchain. He listed three main drivers:

- A change in regulatory tone under the SEC’s current leadership.

- BlackRock entering tokenization in 2024, which forced other institutions to pay attention.

- Old systems in stocks, bonds, and Treasuries that still run on outdated, siloed infrastructure.

Tokenization promises instant settlement (atomic trades), fewer middlemen, lower costs, and faster capital rotation. His main point: Wall Street is not changing the rules, it is updating the infrastructure, and the next big area for tokenization is equities.

In a concrete step, JPMorgan launched its first tokenized money market fund on Ethereum. This is not a testnet demo; it is a real fund running on a public chain. The message is that Wall Street has moved from “experimenting” to executing on public blockchain rails.

On the stablecoin side, Circle started testing USDCx, a privacy-preserving version of USDC on the Aleo network using zero-knowledge proofs. The goal is bank-level privacy while keeping full compliance records. If it works, this model could redefine how stablecoins are used by both institutions and individuals: private enough for comfort, transparent enough for regulators.

Institutional Adoption and Real-World Use

While charts looked bad, institutional and real-world adoption quietly strengthened.

- Bitwise filed for a SUI ETF, joining the wave of products after new ETFs for XRP, DOGE, and SOL in recent months.

- The owner of the New York Stock Exchange (NYSE) entered talks to invest in MoonPay, showing that even the most traditional venues are now interested in crypto infrastructure.

- A thread noted that 14 of the 25 largest U.S. banks are developing Bitcoin products for their clients, moving from years of ignoring and fighting BTC to a clear phase of adoption.

- The largest bank in Brazil recommended that clients allocate 3% of their portfolios to Bitcoin, calling BTC real diversification, not just speculation.

- ADNOC, the biggest fuel seller in the UAE, began accepting stablecoin payments at 980 stations across three countries. This is direct, everyday usage of crypto for fuel, not just trading.

- Phantom wallet launched Phantom Cash debit cards in the U.S., with plans to expand globally. This ties self-custody wallets to real-world spending.

- CryptoPunks announced that eight punks are now part of the Museum of Modern Art (MoMA) permanent collection in New York, donated by Art on Blockchain and other collectors, with extra pieces from Larva Labs. It is another big step for early NFTs into the mainstream art world.

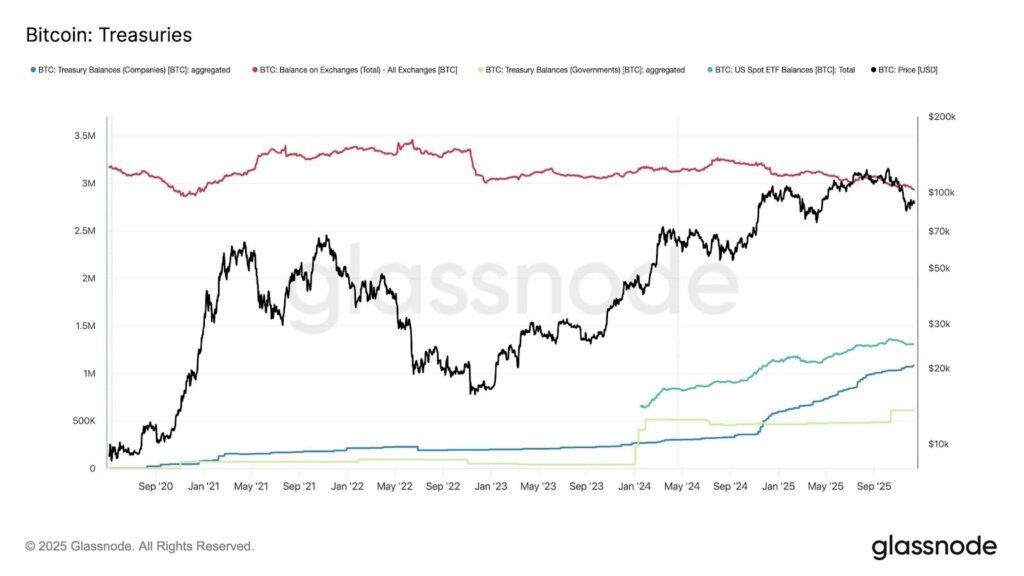

On the corporate and allocation side, Glassnode data showed that institutional holdings of Bitcoin are close to 30% of circulating supply, around 5.94 million BTC held by exchanges, ETFs, public companies, and governments. That means less free float and more impact from any new wave of demand.

BitMine, a company tied to Tom Lee, was reported to have bought another $140 million of ETH on Tuesday, taking its holdings to roughly 4 million ETH, worth about $11.6 billion. That is a strong signal of long-term conviction in Ethereum even in a weak market.

Networks and Technology: Solana vs. Ethereum, plus New Experiments

On the network level, Solana and Ethereum both had important updates, but with very different vibes.

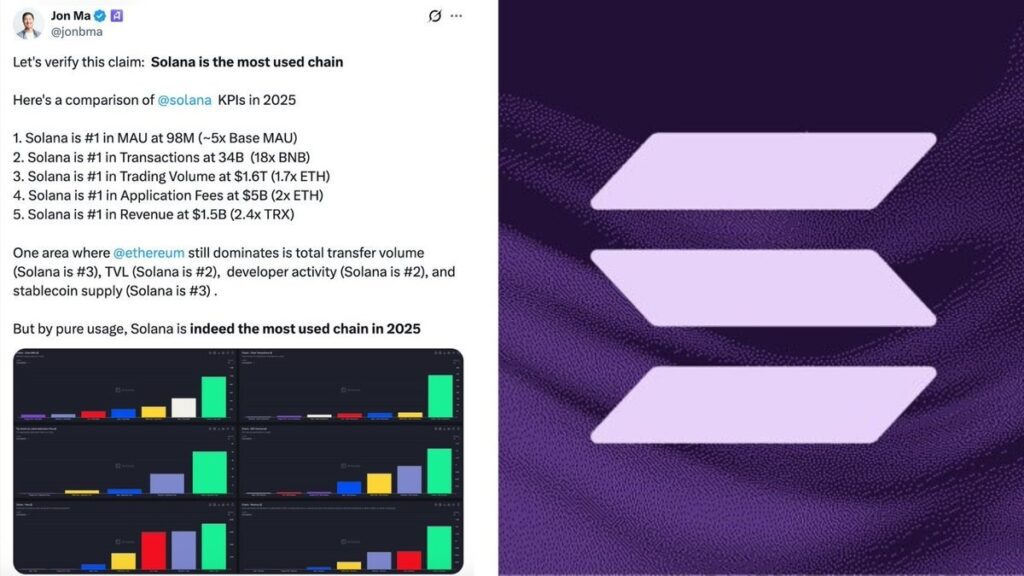

A report from Artemis said Solana is the most used network in 2025 by a wide margin:

- About 98 million monthly active users, roughly 5x Base

- Around 34 billion transactions, about 18x BNB

- Trading volume near $1.6 trillion, about 1.7x Ethereum

- $5 billion in app fees (twice Ethereum)

- $1.5 billion in revenue (2.4x TRX)

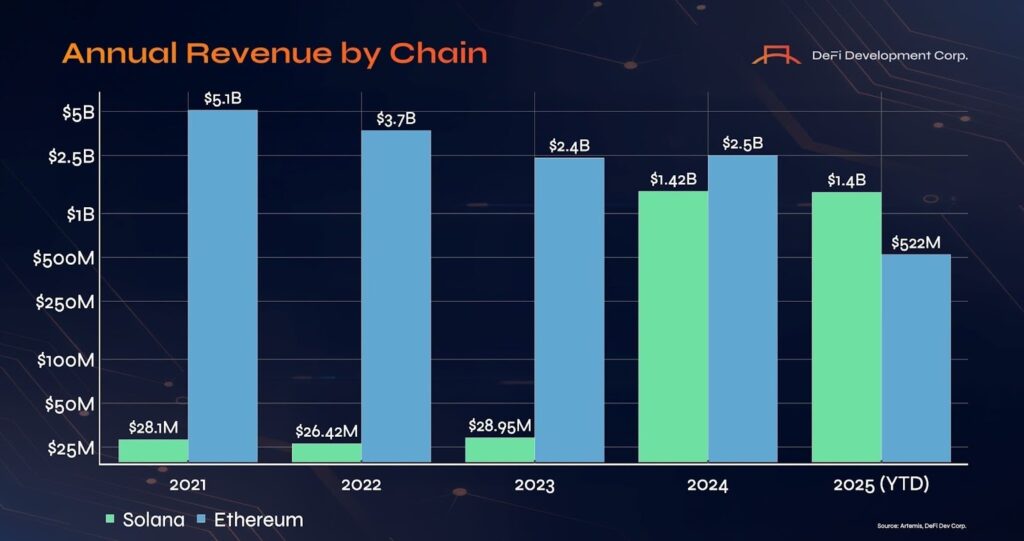

Another analysis said Solana is on track to surpass Ethereum in annual revenue for the first time, jumping from around $28 million in 2021 to about $2.5 billion in 2025 year-to-date, while Ethereum’s revenue has fallen from above $5 billion to about $1.4 billion. The comment from DeFi Development Corp described Solana as the “revenue chain where the dApps of tomorrow will live, scale, and breathe.”

Anthony Scaramucci doubled down on this view. He said Solana could still 20x from here and kept his long-term $2,500 SOL target. For him, the delay is about regulation and macro, not about Solana failing. He compared the situation to Amazon, which once fell 90% and was declared dead many times before dominating global retail. His simple message: great technology survives volatility, and regulation catches up later.

On the Ethereum side, developers are discussing a gas limit increase to 80 million after the upcoming Blob Parameters upgrade, possibly in January. That would mean higher transaction capacity, faster processing, and less pressure in peak times, assuming the network can handle it safely.

Market Stress: Volumes Collapse, Liquidations Spike, and Altcoins Bleed

Price action and flows were rough almost everywhere.

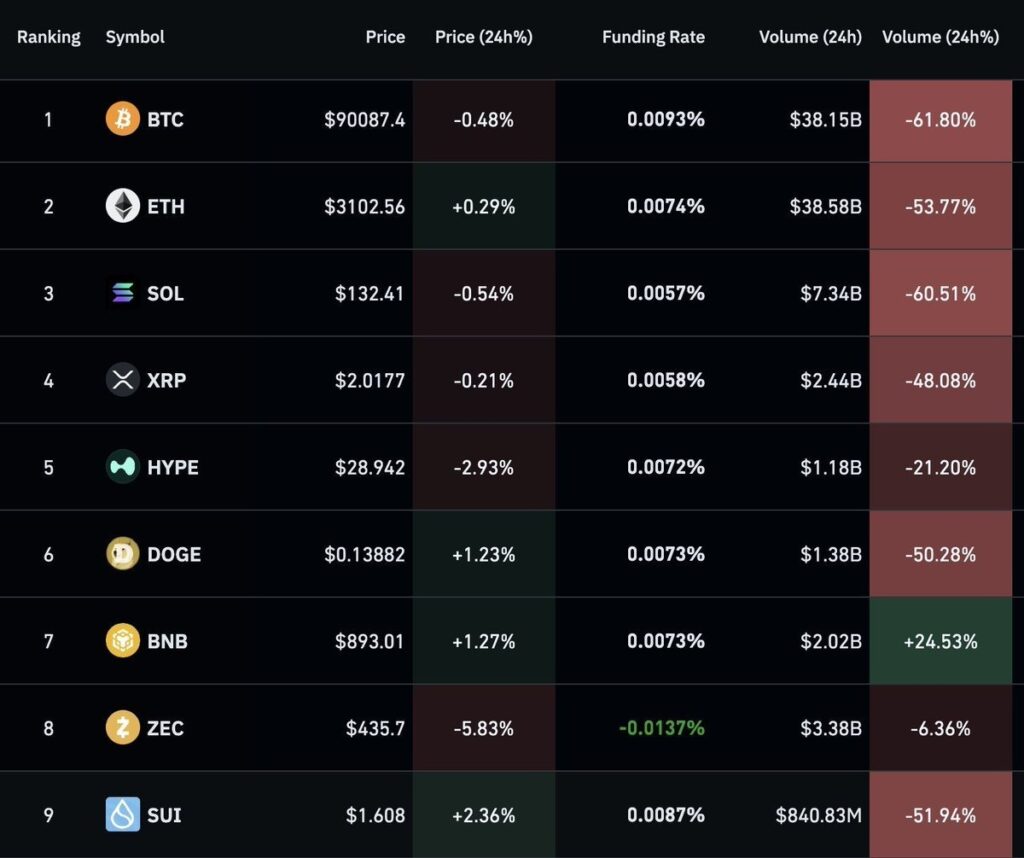

Early in the week, the market saw a sharp crash in volumes over 24 hours:

BTC volumes fell 61%, ETH volumes fell 54%, and most altcoins saw double-digit drops in trading volume. BNB was the only major coin with +24% in volume. Low liquidity means less depth and a higher chance of sudden moves.

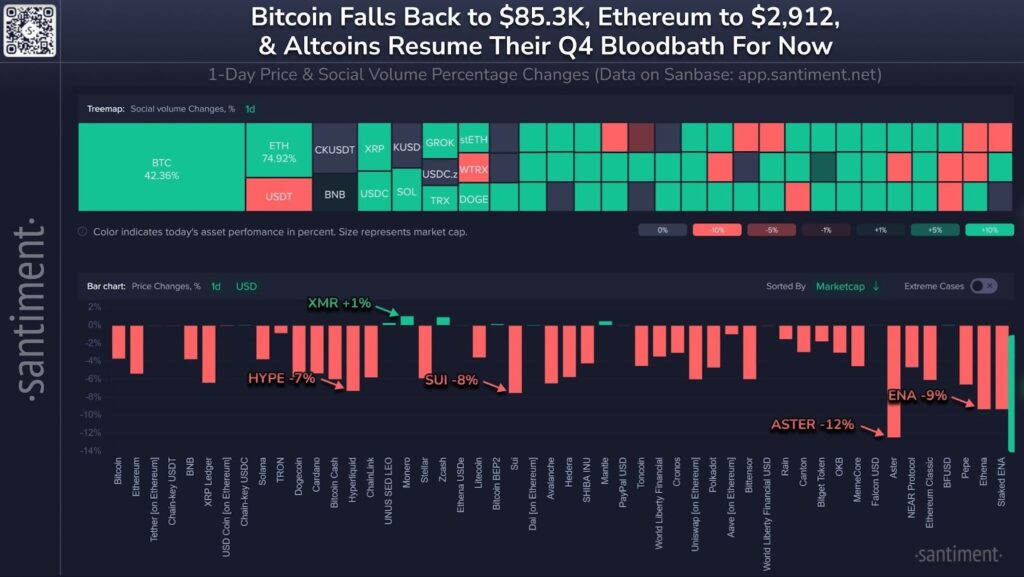

In another window, crypto lost $23 billion in under two hours, taking the total loss to about $127 billion in market cap over 24 hours. At the same time, more than $544 million in positions were liquidated, mostly longs, which tells us many traders were still betting on upside despite the macro fear.

On Monday, the start of the week was described as disappointing: Bitcoin held its ground, but altcoins took heavy hits. Some of the worst one-day drops were ASTER (-12%), ENA (-9%), SUI (-8%), and HYPE (-7%). The message was clear: BTC support is the main line of defense right now, while altcoins take the damage first.

On a bigger horizon, one thread described 2025 so far as one of the worst years for crypto. Most crypto investments from the last year are deep in red. Bitcoin and a small group of large-caps are holding up relatively better, but:

- Stocks are near all-time highs

- Gold and silver are at or near record levels

- Even Treasury bills have outperformed Bitcoin this year

- Altcoins, meme coins, and even projects with tens of billions in TVL have fallen back to levels near the 2022 bottom

This is happening despite many positive structural signals: Wall Street opening its doors, banks and institutions adopting digital assets. The conclusion was that we might be in a “maximum pain” zone, which historically often appears near cycle lows. The hope is that next year will look better.

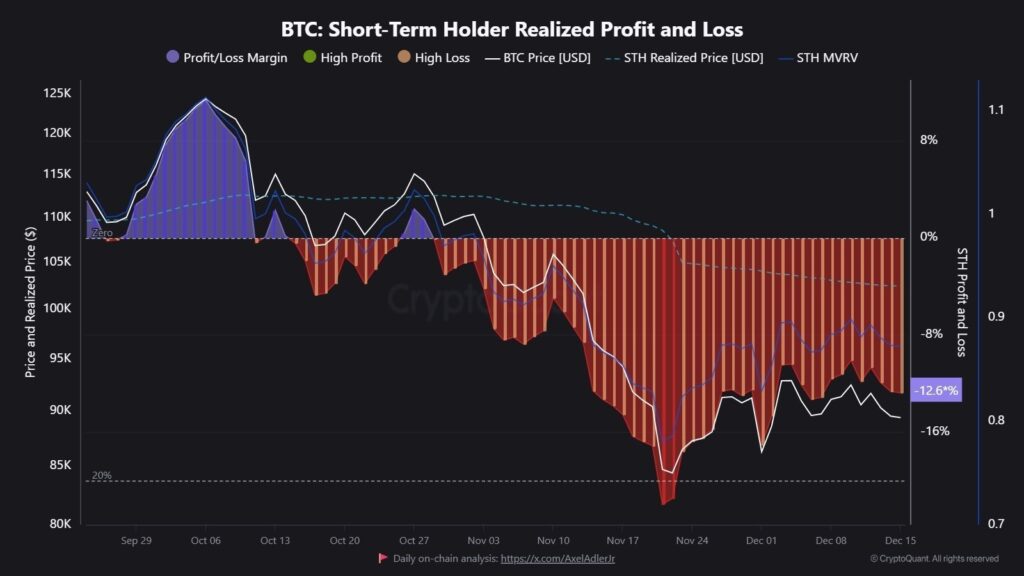

On-chain data backed up the stress. Short-term Bitcoin holders are under heavy pressure. Since October 30, BTC has traded below around $104,000, which is the average cost basis for these new buyers. They are now realizing losses at an average of –12.6%, a clear sign of capitulation. Glassnode’s view was that these periods of realized loss and surrender often come right before major trend shifts, though volatility stays high.

At the same time, the number of active Bitcoin addresses fell to the lowest level in a year, showing lower network usage and less retail participation for now.

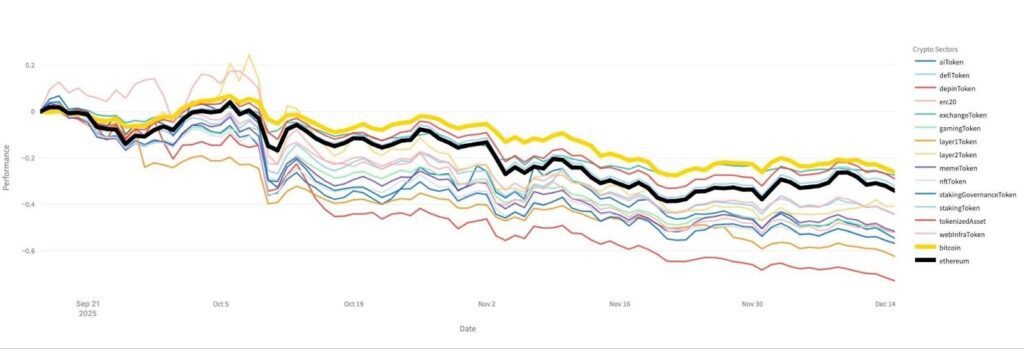

Glassnode also reported that most crypto sectors underperformed Bitcoin over the last three months, which means capital has moved back into BTC as the “strongest asset” during turbulence.

Sentiment and Narratives: Fear, Supercycle, or “Hard Year” Ahead?

Sentiment data from Santiment showed that retail mood is now mostly bearish. Historically, this kind of pessimism often lines up with price reversals, where prices move up when most people expect more downside. The line was simple: when fear dominates, opportunities start to appear. Whether that pattern repeats is always uncertain, but the setup looks familiar.

On the narrative side, there were mixed signals.

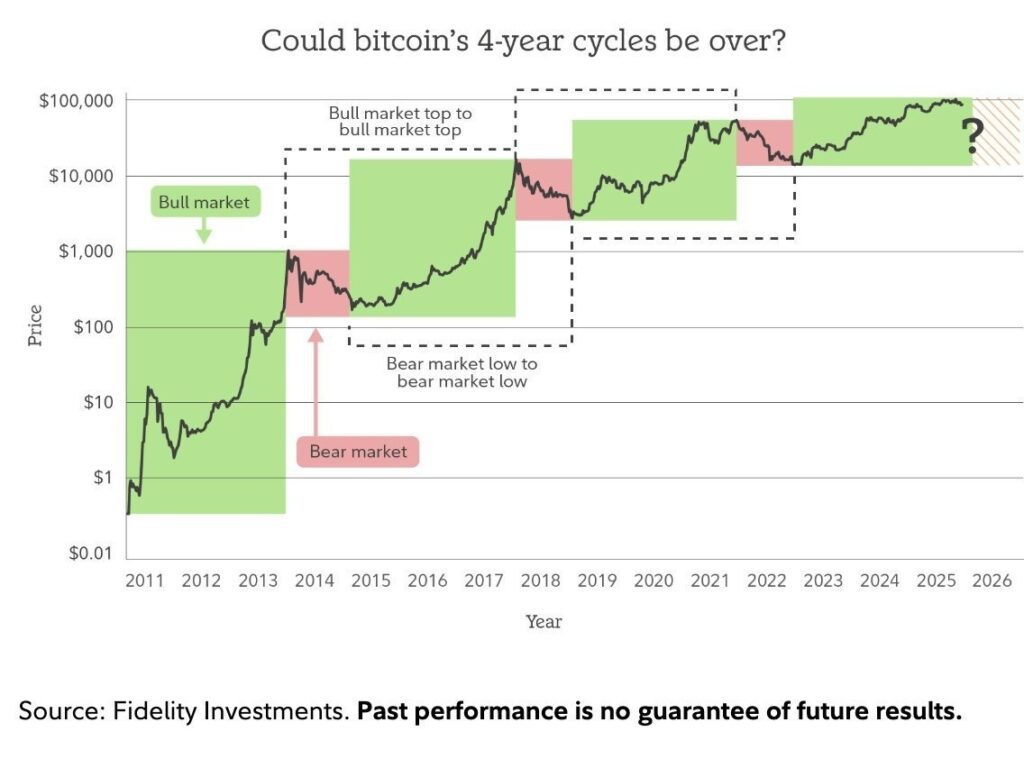

- Fidelity suggested that the classic four-year Bitcoin cycle might be over and that we could be in a supercycle instead.

- Barclays, on the other hand, warned that 2026 could be a difficult year for crypto if spot volumes stay low and demand remains weak.

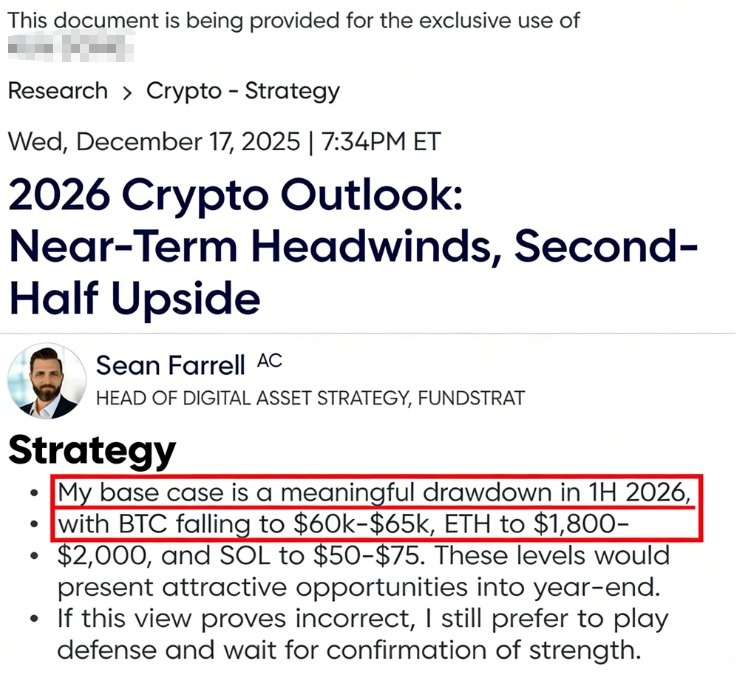

- Fundstrat’s internal 2026 crypto strategy report (shared by @_FORAB) reportedly expects a large correction in the first half of 2026, with target ranges of BTC $60k–$65k, ETH $1,800–$2,000, and SOL $50–$75. This directly contradicts Tom Lee’s public statements, where he recently said ETH at $3,000 is deeply undervalued and even predicted $15,000 ETH by the end of 2025.

So we have big firms telling two different stories at the same time: public bullishness and private caution. That alone tells you how uncertain the environment is.

Individual Projects and Assets: SUI, HYPE, WLFI, and Strategy

A few specific names also had important updates:

- SUI: Beyond the price drop earlier in the week, SUI was in the spotlight because Bitwise filed for a SUI ETF, adding it to the list of assets with institutional-grade products.

- HYPE: The Hyper Foundation proposed a burn of HYPE tokens held in the support fund. Validators will vote on whether to permanently remove these tokens from circulation, and the community is watching the result closely.

- WLFI / USD1: As mentioned, the WLFI community is pushing the idea of using treasury unlocks as incentives for USD1 usage, in an attempt to grow a new stablecoin in a crowded market.

- Strategy (MicroStrategy): CEO Phong Li explained that Bitcoin’s drop to around $85,000 is not a “Bitcoin problem” but a liquidity problem. He pointed to risk-off flows, tighter central bank policy from the Fed and BoJ, and stressed that in the long run they expect wider bank adoption, potential sovereign buyers, a more dovish Fed by 2026, and stronger risk appetite during the election cycle. Their strategy: keep being a net buyer, treating BTC as a generational asset class despite short-term pain.

Culture, Access, and Market Hours

Two more trends touched the edges of crypto:

- Nasdaq is planning to extend its trading hours to 23 hours per weekday, aiming for 24/5 markets by the second half of 2026. This brings traditional equities closer to the 24/7 crypto model and shows global demand for constant market access.

- The mix of MoMA’s CryptoPunks, Phantom’s debit card, ADNOC’s stablecoin fuel payments, and banks recommending direct Bitcoin allocations all point to the same direction: crypto is slowly leaving the “isolated exchange screen” and entering normal life, art, fuel, cards, and portfolios.

Closing Thought

This week looked bad if you only watched prices: market cap wiped out in hours, volumes collapsing, altcoins bleeding, short-term holders capitulating. But underneath, the structure around crypto kept getting thicker: more rules (even if messy), more tokenization, more banks building products, more real-world payment rails, more institutional Bitcoin and Ethereum positions, and rising usage on networks like Solana.

For now, it is a market of maximum discomfort: macro is noisy, policy is shifting, and narratives are conflicting. But the plumbing, regulatory, technological, and institutional, is being laid down piece by piece, even in the middle of the pain.

This recap is for information and education only. It is not financial advice, and it is not a recommendation to buy or sell any asset. Markets are risky, and every investor’s situation is different, so always do your own research (DYOR) and, if needed, talk to a professional advisor before making decisions.

If you want to go deeper into these topics, you can read more detailed breakdowns on blog.millionero.com.

When you feel ready, you can trade spot and futures on Millionero, but always use size and risk you are comfortable with.