This week started with a slow grind lower across risk assets, and it ended with a literal shock headline: early Saturday, Feb 28, Israel said it launched a “pre-emptive attack” on Iran, with explosions reported in Tehran and alerts triggered inside Israel.

Within minutes, the market did what it usually does when geopolitics turns real: it hit the sell button, punished leverage, and reminded everyone that “calm” is often just a temporary setting.

The Middle East story stopped being “background noise”

The key shift is not that tensions existed, they did, but that this week the messaging around Iran’s nuclear file felt like it was running out of polite exits.

One widely shared thread framed Iran’s stance in blunt terms: no dismantling Fordow, no shutting Natanz, no touching Isfahan, no handing over enriched uranium, with a “temporary freeze” offered instead, while Washington’s demand was described as zero enrichment, forever. Another part of that same thread added a darker layer: even with a large U.S. buildup, “Pentagon insiders” allegedly said a long bombing campaign would be hard to sustain, with strikes only lasting 7–10 days before munitions constraints bite.

Then Saturday hit: Israel’s announcement, reports of blasts in Tehran, and a fast rise in “what happens next?” risk.

The market doesn’t need perfect information to react. It only needs uncertainty plus positioning.

Bitcoin’s instant reminder: leverage is always the first victim

As the strike news spread, the crypto tape reacted like a levered instrument tied to global risk appetite.

A breaking post claimed Bitcoin fell below $64,000, and that over $100M of levered longs were liquidated in about 15 minutes. Another clip-style post described Tehran “right now” during the strikes, with the implication that the headline itself was the catalyst.

Whether your model says “BTC is a hedge” or “BTC is risk-on,” weeks like this push you toward the simple observation: in sudden fear, BTC trades like liquidity. That lined up with another theme that appeared earlier in the week: Ki Young Ju arguing Bitcoin is in a phase of “not digital gold,” behaving more like a growth asset driven by liquidity conditions and risk mood.

Inflation wasn’t gone, it was just waiting for attention again

Even before Saturday’s geopolitical jolt, the macro data and macro mood were already heavy.

Producer prices ran hot

January PPI came in hotter than expected, with headline final demand up 2.9% year-over-year, and market chatter focusing on a hotter-than-expected “core” read.

The important part is not the exact decimal. It’s what it does to the story: sticky inflation keeps the rate-cut dream on a tighter leash.

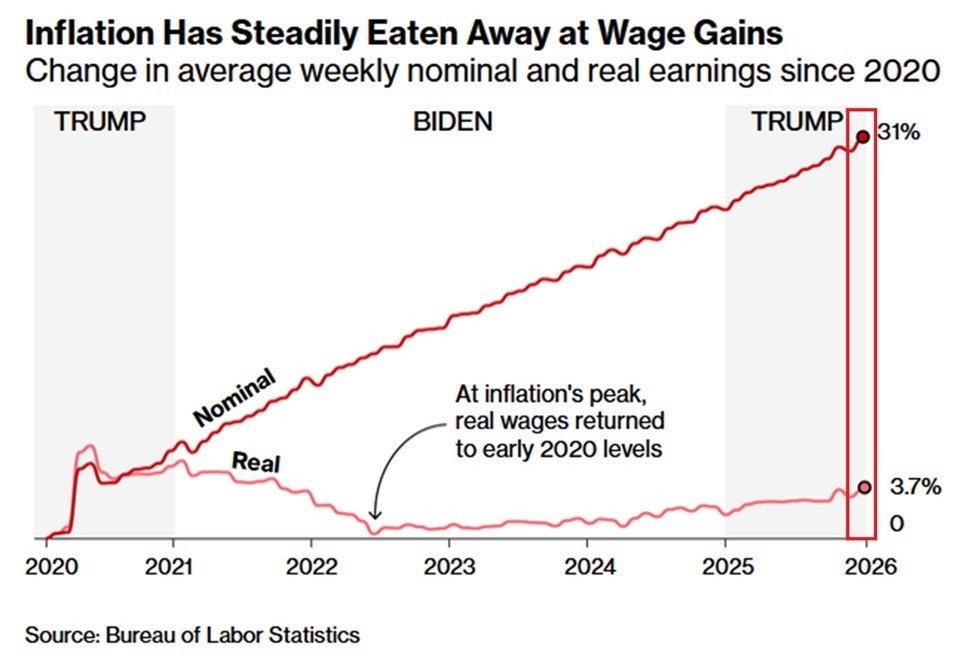

Real wages: small gains, big frustration

Another post laid out the lived reality: since 2020, real (inflation-adjusted) weekly earnings were said to be up only about +3.7%, while the cost-of-living lines looked ugly, utility gas, electricity, home insurance, used cars, motor vehicle insurance, all up sharply over the same window. The message was simple: households feel squeezed even if nominal wage numbers look “fine.”

The leverage elephant: margin debt at records

This week also carried a loud warning about leverage in traditional markets: U.S. margin debt was cited as jumping +$53B in January to ~$1.28T, marking the 9th consecutive monthly increase, with year-over-year growth described as the biggest since the meme-stock era.

That matters because high leverage makes markets fragile. When a surprise hits (inflation, war, earnings), the unwind can be fast and mechanical.

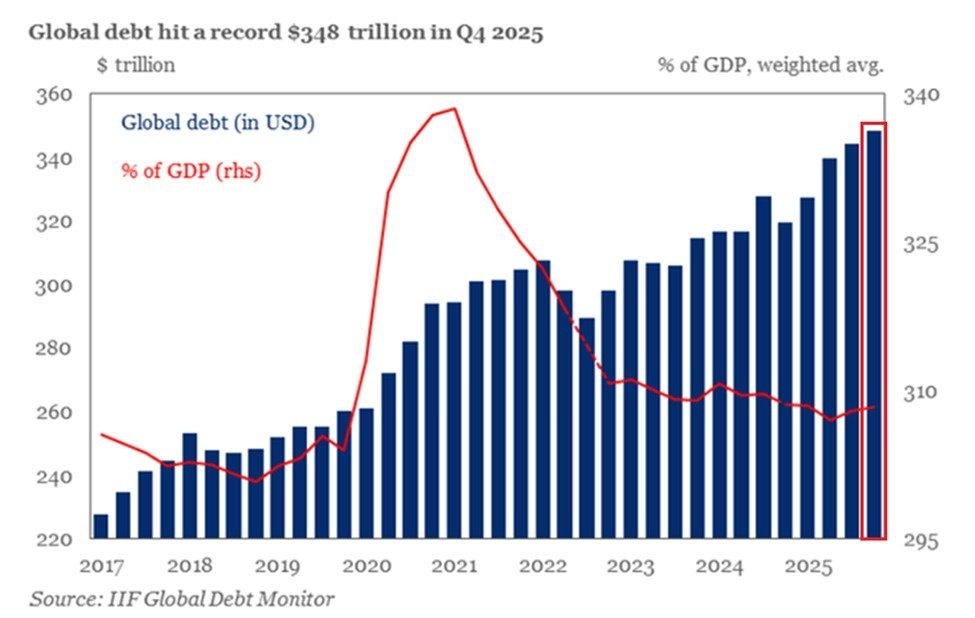

Global debt kept climbing

A separate macro thread pointed to global debt hitting about $348T at end-2025, with roughly $29T added in 2025, flagged as the fastest pace since the pandemic period.

In plain terms: the world is still leaning on debt, even as rates and geopolitics make that comfort less comfortable.

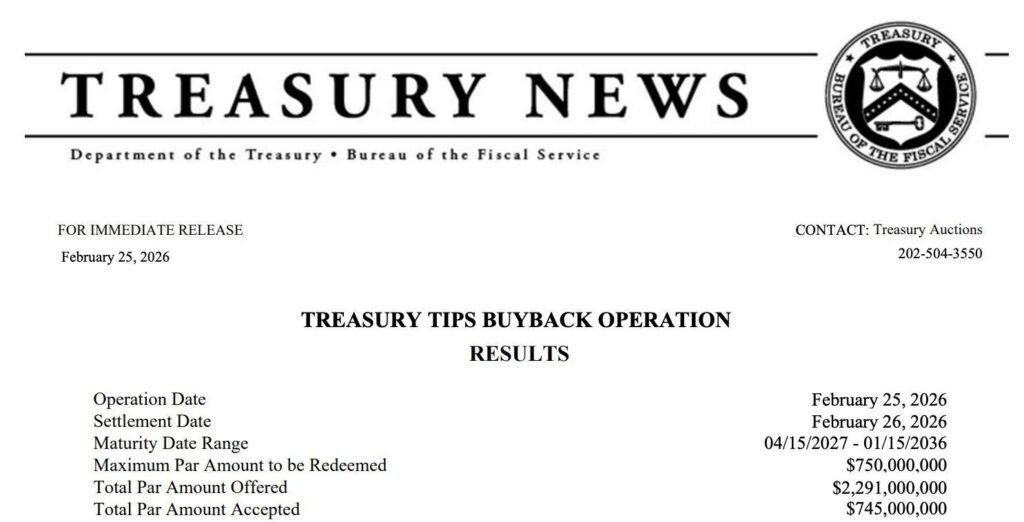

The Treasury buyback headline

Another item that floated through the feed: the U.S. Treasury conducted debt buybacks, one post cited a $745M operation, with total buybacks “this week” above $2.7B. (Mechanically, buybacks are about liquidity and debt management optics, but psychologically, people read them as “something is being managed.”)

“The biggest risk isn’t inflation, it’s an equity drawdown”

A Goldman-linked warning made the rounds: if stocks correct hard, the wealth effect flips, confidence drops, spending slows, and financial conditions tighten fast, and that pressure can spill into crypto too. This fits the week’s broader pattern: the market is not just watching inflation; it’s watching how crowded positioning reacts when the floor moves.

AI turned into a political battlefield, and defense became the center

This week didn’t just have an “AI boom” story. It had an AI power struggle story.

OpenAI funding + the defense angle

A widely shared breaking post claimed OpenAI announced a $110B investment round valuing it around $730B, with a breakdown listing SoftBank, NVIDIA, and Amazon as major participants. Bloomberg also reported OpenAI finalized a $110B funding at a $730B valuation.

Then came the sharper headline: OpenAI reached an agreement to deploy models on a U.S. defense classified network, with Sam Altman publicly framing it around safety and guardrails.

Anthropic: the public clash became policy

The biggest drama was the U.S. government ordering agencies to stop using Anthropic technology. Reports tied it to a dispute over whether AI should be usable for things like mass surveillance or autonomous weapons, which Anthropic opposed under its safety rules.

A separate thread tried to summarize the last two weeks as a chain reaction: IBM dropping, cybersecurity stocks selling off, “over $100B” erased across industries, Anthropic rejecting a “final offer,” and then the government ban. The tone was clear: the AI revolution is accelerating, and it’s now entangled with state power.

The follow-up twist: WSJ reporting Altman/OpenAI working on a deal framework to resolve the Anthropic–Pentagon standoff.

SpaceX IPO rumor fuel on top

As if the week needed more momentum headlines, Bloomberg reported SpaceX weighing a confidential IPO filing as soon as March.

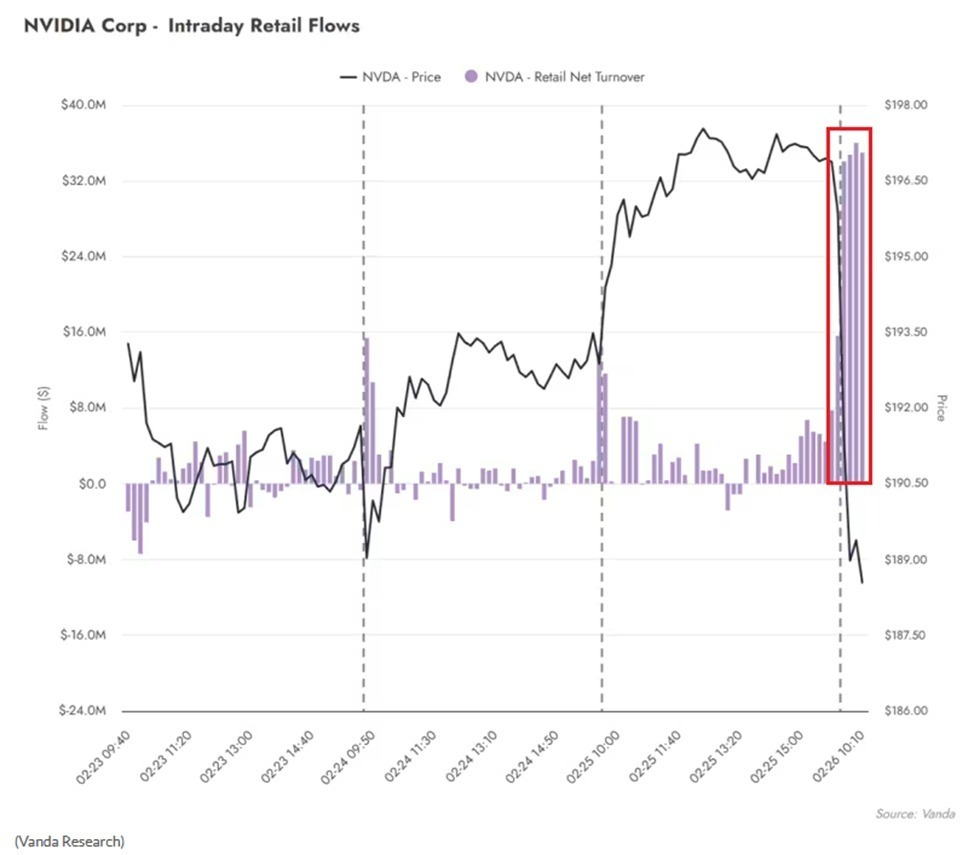

Meanwhile in equities: Nvidia and software positioning looked tense

Nvidia had “historic quarter” chatter, huge numbers, and retail buyers reportedly piling in, yet the stock still sold off on the day, a reminder that even good news can get punished when positioning is crowded.

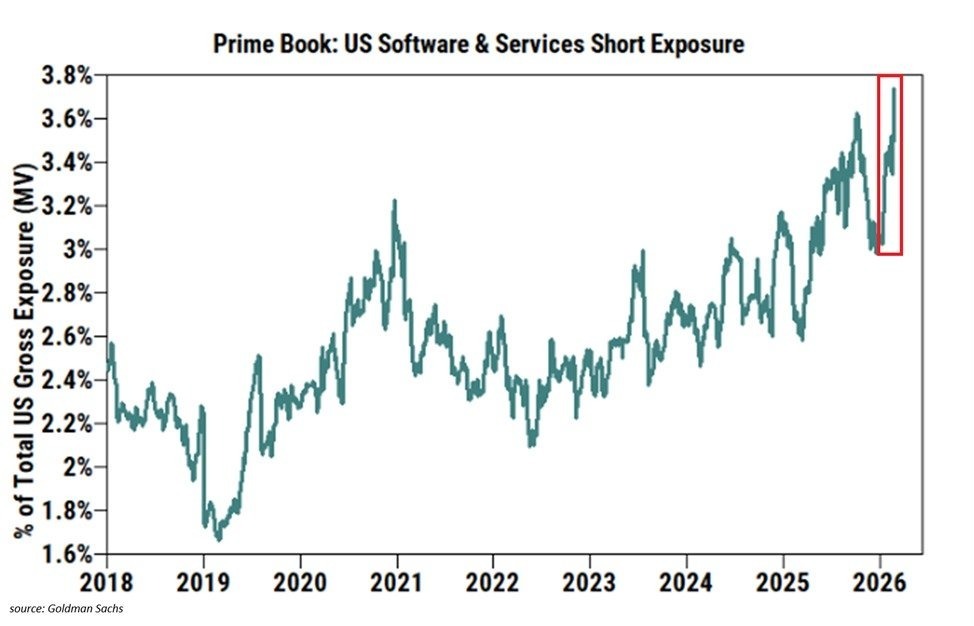

At the same time, a hedge-fund positioning post claimed funds have never been this bearish on U.S. software stocks, with short exposure at records, raising the question: if the narrative flips, does it squeeze?

Crypto regulation and the stablecoin fight got louder

While markets were busy reacting to war and inflation, the policy layer kept moving.

A post noted a U.S. Senate meeting around a digital-asset market structure bill, with Democrats discussing it as a March 1 deadline approached related to stablecoin yield rules.

And the stablecoin debate itself became a banking story: Bank of America’s CEO was cited warning that as much as $6T in bank deposits could migrate toward stablecoins if the rules enable yield-like behavior at scale.

Outside the U.S., the Bank of Korea was reported urging that won-denominated stablecoins should be issued primarily within the banking sector first, citing money laundering and financial stability concerns.

A separate policy idea also appeared: a proposed crypto tax change that would treat stablecoins more like cash for tax handling, and exempt small crypto transactions to make everyday usage less messy.

“Wall Street isn’t watching crypto, it’s moving on-chain”

This week had one of the clearest “TradFi → on-chain” clusters in a while.

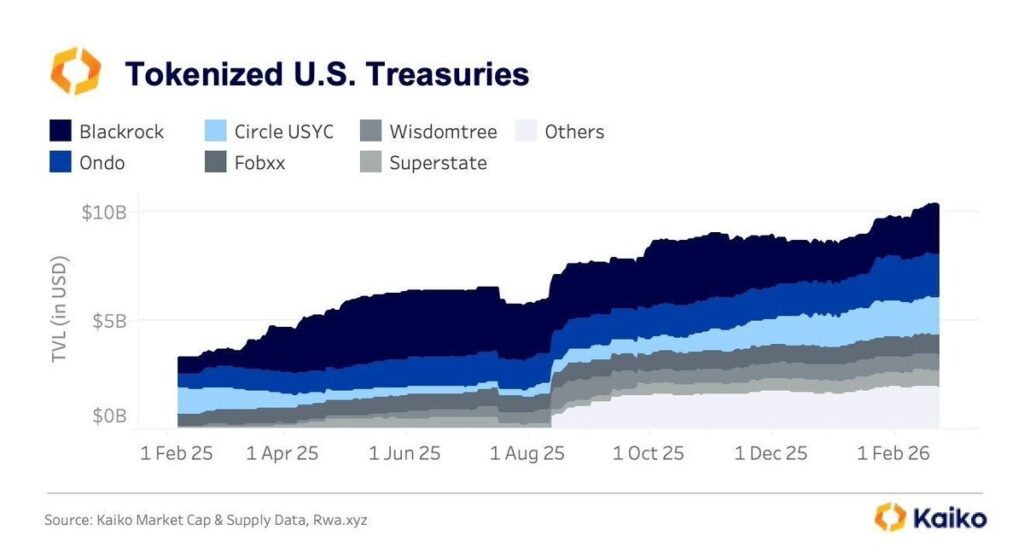

Tokenized Treasurys crossed a psychological line

Tokenized Treasury products were said to have crossed $10B in total value, a milestone that keeps coming up because it’s simple: the most conservative asset in finance is being wrapped into 24/7 digital rails.

WisdomTree: 24/7 trading with instant settlement

WisdomTree announced a plan to launch 24/7 trading and instant settlement for tokenized money market fund shares, with SEC exemptive relief framed as a “first of its kind” step toward true secondary liquidity for registered tokenized fund shares.

BlackRock + Uniswap, Apollo + Morpho, ParaFi + Jupiter

The institution-to-DeFi bridge had multiple touchpoints:

- BlackRock’s tokenized Treasury fund BUIDL was reported as becoming tradable via Uniswap-linked rails, alongside BlackRock purchasing some UNI.

- Apollo was reported signing a cooperation agreement that allows it to acquire up to 90M MORPHO over 48 months, the kind of slow, controlled accumulation that screams “strategic positioning,” not “tourism.”

- Jupiter was mentioned as getting a $35M investment from ParaFi via direct token purchase (JUP), another example of “buy the asset, not just the story.

Put together, the signal is not “institutions are coming” (old line). The signal is: institutions are choosing specific rails, tokenized cash management, on-chain lending infrastructure, and deep liquidity venues.

Crypto market internals: pain, cleanup, and trust problems

Under all the headlines, the crypto internals read like a market trying to detox.

- Futures leverage was described as coming down after a long period of being too high, with forced liquidations acting like a brutal reset.

- Options positioning was described as “flipped,” with the warning that a strong move either direction could accelerate due to hedging mechanics.

- Strategy (MicroStrategy) was described as the most shorted stock globally, with large BTC-linked unrealized losses cited, creating a setup where volatility can feed on itself (downward pressure or a squeeze if it reverses).

- Several “bottom-ish” stress signals were repeated: weekly RSI near extreme oversold territory, realized profit/loss ratio under 1, and a USDT liquidity-stress pattern that some said last appeared near major lows.

- At the same time, a more constructive note appeared: spot demand was said to be rising again for the first time since late November, a hint that “real buyers” might be returning, not just derivatives churn.

And then there’s trust:

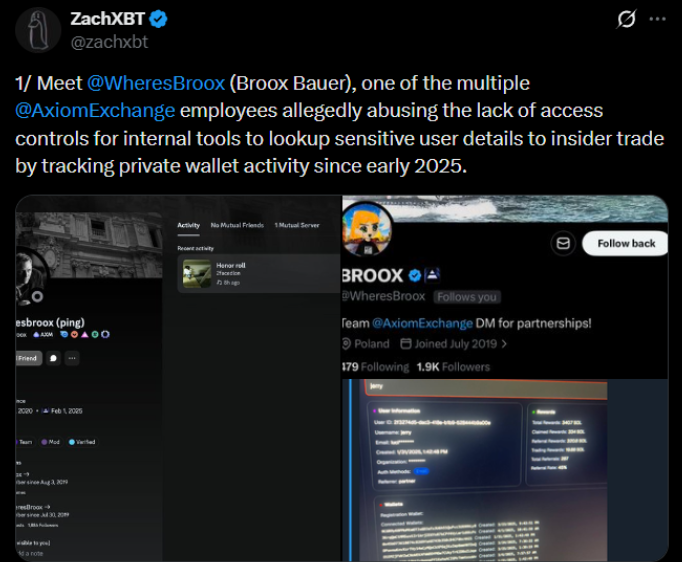

- ZachXBT publicly named AxiomExchange in an alleged insider-trading / front-running investigation tied to listings, with the platform issuing a shocked-denial style response.

- Another viral narrative claimed Jane Street deleted posts amid manipulation rumors, including a “10am selling pressure” story that supposedly stopped after a lawsuit.

Even if you treat these as unproven narratives, they still matter, because markets trade belief when transparency is weak.

Closing thought

This week had a very specific feel: the world is more levered than it wants to admit, inflation is still sticky enough to constrain the “easy money” fantasy, and now geopolitics is back in the front seat. At the same time, the on-chain world keeps getting “normalized” through tokenized Treasurys, 24/7 settlement experiments, and institutions buying exposure to infrastructure, not memes.This article is not financial advice.

Please do your own research before making any investment decision. You can also DYOR on blog.millionero.com. When you’re ready, you can trade Spot and Perpetuals on Millionero.