This past week felt like several market stories happening at the same time. The war around Iran kept pushing oil higher and fear across global markets. The Federal Reserve held rates steady, but inflation worries stayed alive. US stocks fell hard, then suddenly bounced on shifting comments from President Trump. At the same time, Bitcoin stayed strong, tokenization moved closer to the political center in Washington, and crypto regulation took a major step forward.

All of that happened in just a few days.

Geopolitics Took Control of the Market Narrative

The Iran conflict remained the biggest macro driver

The biggest force behind markets this week was still the war involving Iran and the growing risk around the Strait of Hormuz. One of the sharpest political comments came from Trump when he said the United States does not use the strait and does not need it. That raised a very obvious question for many traders and observers: if America does not depend on Hormuz in the same way that Europe and Asia do, why is the world being pushed into paying such a heavy price for a conflict around it?

The pressure became even more visible because Washington’s allies did not rush to help secure the route. Germany officially refused to join any mission there, and Italy also made clear that it would not be part of a war against Iran.

Mixed diplomatic signals added even more uncertainty

Iran also kept shaping the message around the strait. Tehran repeated that Hormuz is open to all countries except the United States and Israel. That sounds like a narrow diplomatic line, but the market implication is much larger. It means the conflict is not only military. It is also about who gets access, who carries the cost, and how much pressure can be applied without fully shutting global trade.

At the same time, Israel said it killed Iranian security chief Ali Larijani in airstrikes, while Iran’s foreign minister attacked Macron for not condemning the war earlier. Qatar reportedly gave Iranian military and security diplomats 24 hours to leave, while China said it would keep working toward a ceasefire. Trump, meanwhile, seemed to change tone during the week and started sounding more open to de-escalation.

The message from the region was mixed: more danger on one side, but also small signs that some governments wanted to stop things from getting worse.

Oil Repriced the Inflation Story

Energy markets reacted like the risk was real

Oil showed exactly how serious the market thinks this is. Brent moved above $114 a barrel after strikes hit refineries and gas facilities in the Middle East. In just a short period, oil moved from around $100 to $106 and then to $114, which fed directly into inflation fears.

China started preparing for that risk by signaling it may release up to 1 million barrels per day from its 1.4 billion barrel strategic reserves for 4 to 6 weeks. That could ease some pressure, but it would not fully replace a route that handles around 20% of global oil supply.

Gold buying showed how governments are positioning

At the same time, China kept buying gold for a 16th straight month, taking its reserves to a new record of 2,309 tons worth more than $371 billion. That says a lot about how large states are reading this moment: they are still protecting themselves against a more unstable world.

US Stocks Cracked, Then Reversed

Equities spent most of the week under pressure

The equity market spent most of the week under clear pressure. On March 20 alone, about $1.05 trillion was erased from the US stock market as the major indexes hit six-month lows. The S&P 500 fell 1.57%, the Nasdaq lost 2.11%, the Dow dropped 1.22%, and the Russell 2000 fell 3%.

By the next day, the damage looked even worse in bigger-picture terms: the S&P 500 recorded its lowest close of 2026, and about $3.2 trillion in market value had been wiped out since the Iran war began. Fear was also visible in volatility markets, with the VIX heading toward a third straight weekly close above 25, something that had happened only twice since the end of 2022.

That kind of fear level often comes before a very sharp move, either up or down.

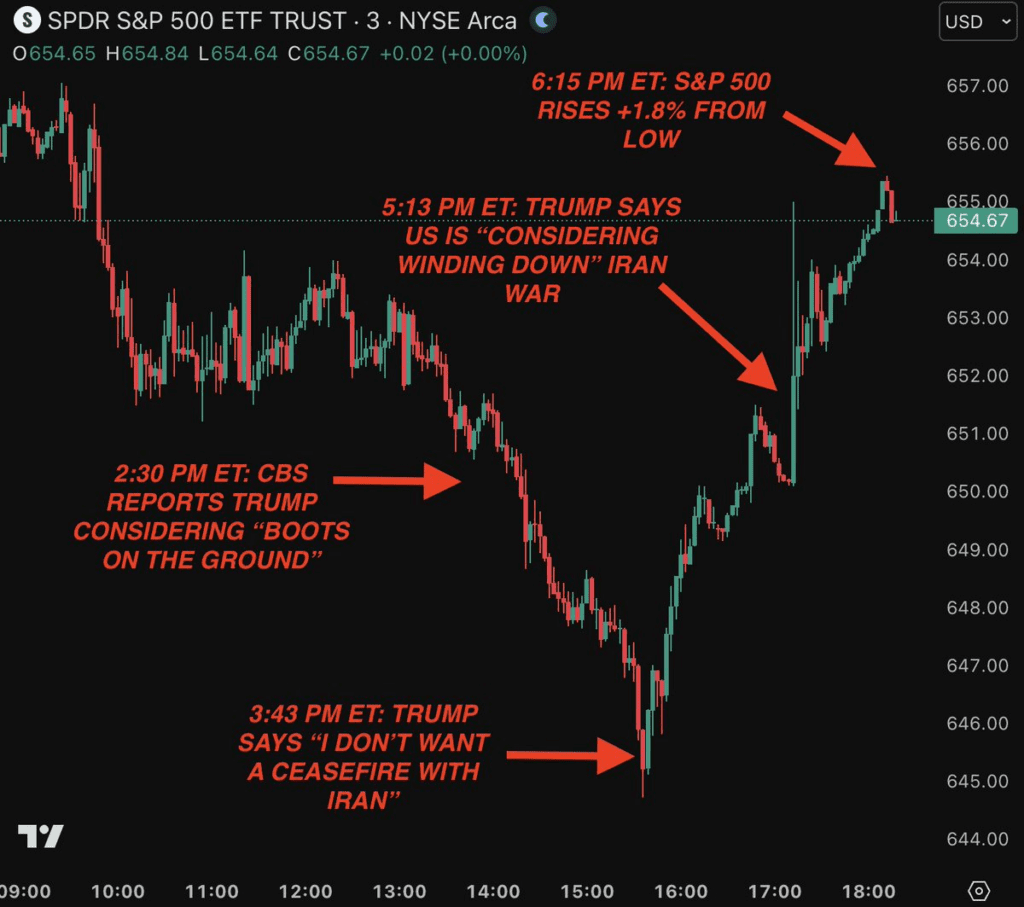

Then politics changed the tone late in the session

Then came one of the strangest parts of the week. On Friday, markets started moving before the headlines caught up. At 6:30 PM UTC, CBS reported that Trump was considering boots on the ground in Iran. At 7:43 PM UTC, he said he did not want a ceasefire, and the S&P 500 hit a new 2026 low.

But about 90 minutes later, at 9:13 PM UTC, Trump said the US was considering winding down the war. In between those comments, the market had already started rising on no major public news. By 10:15 PM UTC, the S&P 500 had rallied 1.8% from its low, adding about $900 billion in market value.

The Nasdaq 100 ETF, QQQ, had also surged, with aggressive long-call options activity showing up into the close. That made the whole move feel less like a clean reaction and more like a market trying to price political tone shifts before they were fully clear.

The Fed Held Steady, but Inflation Risk Stayed Alive

No rate change, but no real relief either

As expected, the Federal Reserve kept rates unchanged at 3.75%. The hold itself was not the story. The more important part was the message around inflation and energy. Powell warned that higher energy prices caused by the war could push inflation upward, but at the same time, the majority of Fed members still do not expect rate hikes from here.

That is a difficult combination. It means the Fed sees inflation risk, but it also sees limits to how much tightening the economy can take.

The data was already running hot

The problem is that the data did not help. February PPI came in hotter than expected, rising 0.7% month over month versus 0.3% expected, and 3.4% year over year versus 2.9% expected. Core PPI also came in above forecasts at 0.5% monthly and 3.9% yearly.

In other words, inflation pressure was already stronger than expected even before oil made its latest jump. That is why Powell’s comments mattered. Traders are trying to figure out whether the Fed can stay patient if war keeps feeding energy costs.

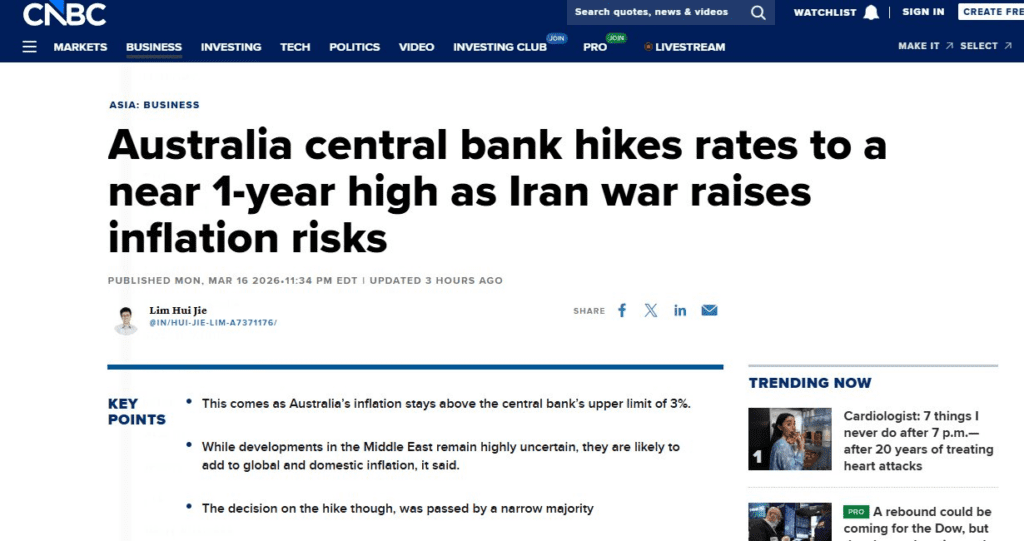

It is not just a US issue either. Australia’s central bank raised rates to the highest level in nearly a year, driven by inflation concerns tied to the Iran war.

Bitcoin Continued to Show Relative Strength

Crypto held up better than many traditional assets

One of the clearest themes this week was that Bitcoin held up much better than many traditional assets. Since February 28, when the war began in the notes provided, Nasdaq was down about 1%, the S&P 500 about 3%, gold around 2% to 4%, and silver about 8% to 12%, while Bitcoin was up roughly 12% to 18% and oil was up 60% to 70%.

That does not mean Bitcoin became a perfect safe haven overnight, but it does show that in this phase of the market, it has been trading with surprising strength.

ETF inflows and spot demand supported the move

That strength was visible in the daily flow too. Bitcoin stayed above $74,000 despite rate pressure, helped by about $199 million of ETF inflows and strong spot demand.

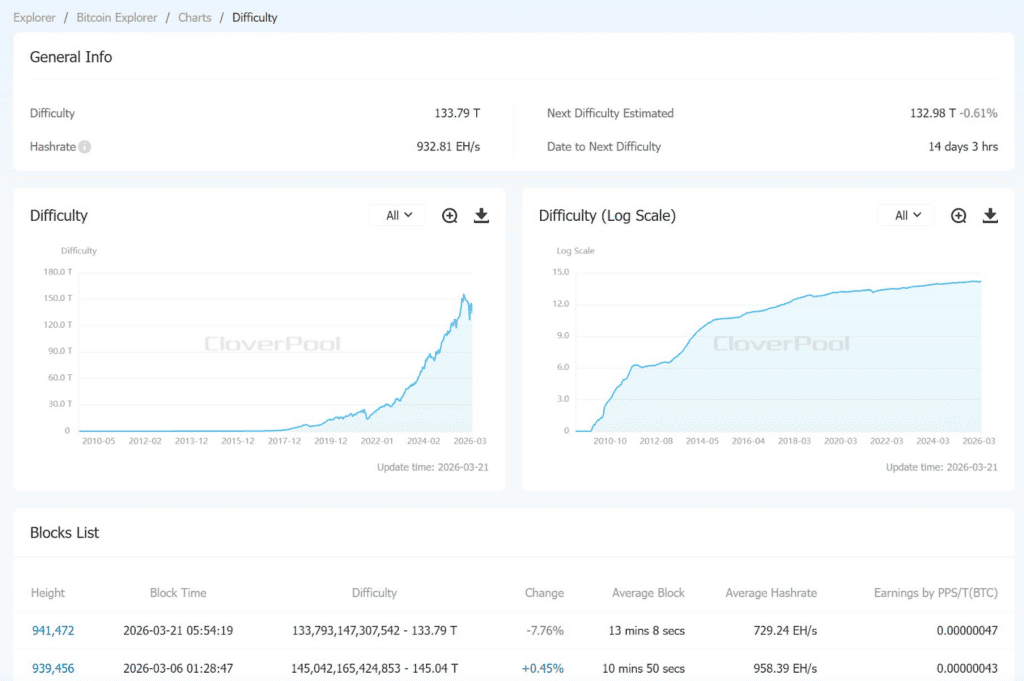

On the network side, Bitcoin mining difficulty dropped to 133.79T at block 941,472, down 7.76%, the second-largest decline of 2026 so far, while hashrate stood around 933.51 EH/s.

Another decline may still come next adjustment. Usually, lower difficulty signals some stress in mining economics, but for the market it can also mean miners are being forced to adapt while price remains firm.

Large holders and public companies kept moving

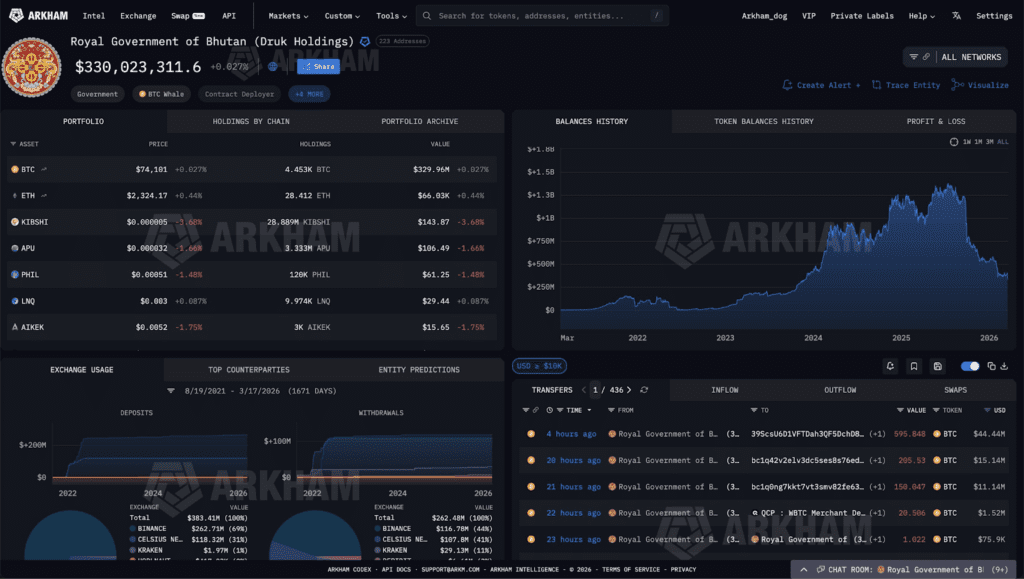

There were also important signals from large holders and corporate players. Bhutan moved $44.4 million in Bitcoin in a matter of hours, bringing 48-hour transfers to $72.3 million, which raised questions about whether it has stopped mining or is simply selling reserves into strength.

Strategy kept pushing harder, buying 22,337 BTC for $1.5 billion at an average price of $70,194. It also pushed deeper into the fixed-income world through STRC, a preferred product tied to Bitcoin that offers an 11.5% annual dividend, effectively trying to connect Bitcoin exposure to the huge global fixed-income market.

In Asia, Japan’s Metaplanet committed another $26 million into Bitcoin infrastructure, while Hong Kong moved ahead by naming its first stablecoin issuers.

The 2022 comparison is still there, but the structure looks different

At the same time, some traders kept warning that Bitcoin still looks similar to its 2022 path. That comparison matters because 2022 ended badly. But the counterargument this week was also strong: today’s backdrop is not the same. Institutions are accumulating, stablecoin liquidity is much larger, and insider selling pressure is much lower than it was during the LUNA and FTX collapse era.

So the chart may rhyme with 2022, but the market structure behind it does not look identical.

Tokenization and Regulation Kept Moving Forward

Washington is treating tokenization more seriously

This week was also important for market structure. A US House Financial Services Committee hearing on tokenization was set for March 25, with the focus on putting stocks and bonds on blockchain and discussing efficiency, liquidity, and transparency.

That matters because tokenization is no longer just a crypto-native idea. It is becoming a real policy topic in Washington, tied directly to broader legislation like the CLARITY Act. Senator Kevin Cramer also called for faster movement on that act, arguing that the US should not let the digital asset industry move overseas.

Traditional finance is exploring blockchain rails

That shift can also be seen in the private sector. Notes from this week said Nasdaq and Intercontinental Exchange, the owner of the NYSE, are exploring moving traditional equities onto blockchain rails.

If that happens over time, it would be one of the biggest changes in market infrastructure in decades. The pitch is simple: 24/7 trading, instant settlement instead of waiting two days, and broader global access.

Commodity treatment for major tokens would be a major legal shift

Regulation also took a major turn in crypto classification. The notes described a joint SEC and CFTC interpretation identifying 16 tokens as digital commodities rather than securities, including BTC, ETH, SOL, XRP, ADA, AVAX, DOT, LINK, DOGE, SHIB, APT, BCH, HBAR, LTC, XLM, and XTZ.

LINK was highlighted again specifically as receiving formal digital commodity treatment. If that framework holds, it would mark one of the clearest legal shifts the sector has seen in years.

Prediction Markets and AI Added Another Layer

Not all digital market growth looked healthy

Away from price action, the week also exposed some cracks in new digital market designs. A group of Democratic senators introduced the BETS OFF Act, which would ban government insiders from trading on prediction markets and would specifically target markets tied to war, assassinations, and terrorism.

The timing followed a disturbing episode in which a journalist covering an Iranian missile strike reportedly received death threats from Polymarket bettors who wanted a report changed to settle roughly $17 million in bets. Polymarket said it condemned the harassment and banned the accounts involved, but the bigger issue is obvious: when large sums of money depend on real-world news, the incentive to pressure reporting can become dangerous.

AI growth stayed massive on both Web2 and on-chain rails

Technology and AI also stayed in the frame. Nvidia CEO Jensen Huang said AI chip revenue could reach $1 trillion through 2027, a forecast that shows how large the AI buildout is becoming.

In crypto-AI, Virtuals Protocol was said to have generated more than $479 million in AI-driven GDP on Base with 23,500 active wallets, showing that the idea of on-chain agent economies is still expanding.

And in the middle of all of this, the broader political backdrop kept producing surreal headlines, including Kim Jong Un reportedly winning North Korea’s parliamentary elections with 99.93% of the vote, while Trump said the US had asked Beijing to delay a Xi summit by about a month because the administration was too busy with the Iran war.

Final Take

Markets are still unstable, but the deeper shifts are getting clearer

This was a week where markets were pulled by war risk, inflation risk, political messaging, and structural change all at once. Oil moved like the world was being repriced around a chokepoint. Stocks traded like fear was in control until one sentence changed the tone. Bitcoin kept acting stronger than many expected. And tokenization kept moving from theory into serious political and market discussion.

The result is a market that still looks unstable on the surface, but underneath that chaos, some very long-term shifts are getting harder to ignore.

This article is for informational purposes only and should not be considered financial advice. Always do your own research before making any investment decisions. For more market updates, visit the Millionero blog, and if you are ready to trade, explore the market on Millionero.