Aave is the closest thing DeFi has to a blue chip. For years it’s been the lending protocol people trusted when they didn’t trust anything else, the default answer when someone asked where to park on-chain capital without losing sleep.

This week, that trust got tested harder than it ever has.

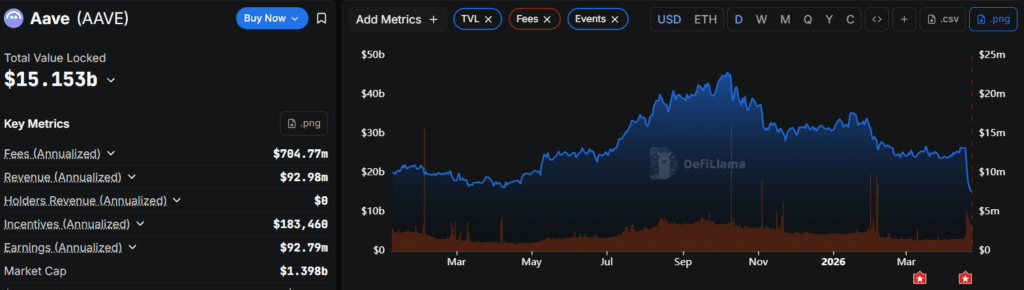

Roughly $15 billion walked out the door in 72 hours. The WETH pool hit 100% utilization. AAVE dropped about 20%. Bloomberg called it a “crisis of confidence.” Jefferies warned banks might pause their blockchain plans. The obituaries started writing themselves before the weekend was over.

They’re early.

Here’s the honest read on what happened, why the freeze was the right call, and why a protocol getting hit this hard is not the same as a protocol being broken.

The Attack Didn’t Start Where the Money Left

A Bridge, Not a Lender

The damage didn’t start at Aave. It started at a bridge.

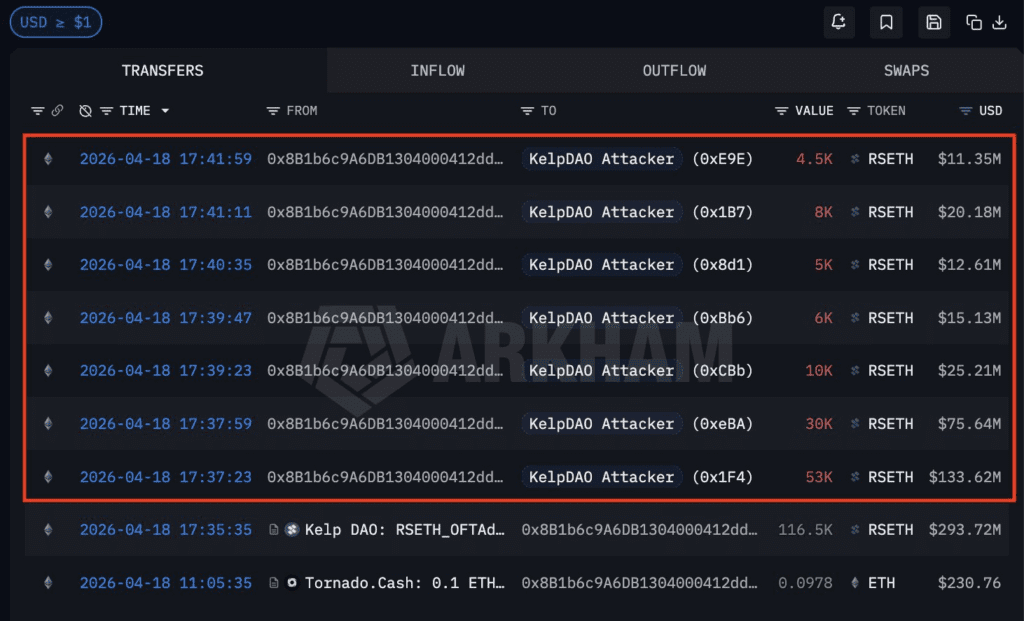

Lazarus-linked attackers exploited KelpDAO’s cross-chain messaging layer and minted roughly 116,500 rsETH, about $293 million, with nothing backing it. They took that synthetic collateral to Aave V3, deposited it, and borrowed real WETH against it. When the dust settled, Aave was staring at somewhere between $123.7M and $230.1M in bad debt, depending on how the losses get socialized.

Why the Distinction Matters

The bridge broke. Aave just happened to be the biggest place the fake collateral could be spent. That distinction isn’t a technicality. It’s the whole story.

If you blame the lender for accepting collateral that a trusted bridge told it was real, you’re blaming the bank for cashing a forged check that the Treasury itself signed off on. The verification happened upstream. Aave was downstream of a system that failed quietly, in a place almost nobody was looking.

The Freeze Was the Right Call, Even If It Felt Like the Wrong One

What the Guardian Actually Did

The moment Aave’s Guardian module recognized the attack, it moved:

- Suspended rsETH borrowing across V3 and V4

- Set the rsETH collateral factor effectively to zero

- Paused WETH borrowing and tightened collateral requirements

Why It Triggered the Run

That’s what triggered the run. Depositors saw a freeze, remembered every CeFi collapse they’ve lived through, and sprinted for the exits. Fair reaction. Wrong conclusion.

A freeze is not a bank run. A freeze is the system refusing to let a thief keep stealing. If Aave had done nothing, the bad debt wouldn’t have capped at $230M. It would have kept climbing for as long as the attacker could find WETH to borrow. The “decentralization” that lets someone drain a protocol unopposed is not a feature. It’s a design flaw pretending to be a principle.

The Precedent Nobody Argued With

Arbitrum’s Security Council made the same call last week, freezing roughly $71M tied to the same exploit. Nobody called that a betrayal of decentralization. Nobody wrote thinkpieces about admin keys. The market quietly applauded and moved on. The logic is identical here. Either intervention is acceptable when funds are actively being stolen or it isn’t, and the market has already chosen its side on that question.

The Money Didn’t Flee. It Rotated.

Read the Flows, Not the Headlines

This is the part the mainstream coverage keeps flattening. The outflow wasn’t a flight from DeFi. It was a rotation inside it.

- Aave TVL: fell roughly from $48.5B to $30.7B in three and a half days

- WETH, USDC, USDT pools: 100% utilized, fully borrowed, no withdrawals possible without fresh deposits

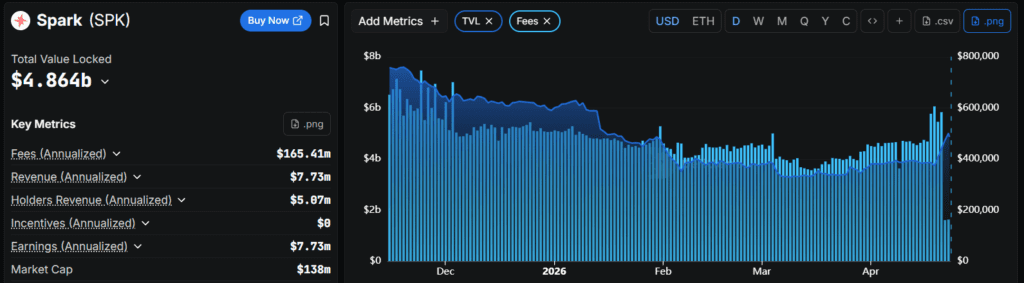

- SparkLend (MakerDAO’s lending arm): TVL jumped from $1.9B to $3.2B

- Compound, Uniswap, Curve: basically flat. No contagion.

- AAVE token: down ~18 to 20% in a day

- SPK (Spark’s token): up ~26% in 24 hours

Where the Capital Ran To

Read that carefully. Money left Aave and moved into Spark, which runs tighter collateral rules, 72% LTV versus Aave’s 93% on rsETH. That’s not a crisis of confidence in decentralized lending. That’s decentralized lending working. Capital rotated toward the venue with stricter risk parameters, which is exactly what a functioning market is supposed to do after it learns a painful lesson about leverage.

If this were a systemic break, Compound and Curve would be bleeding too. They aren’t. The rest of the neighborhood is quiet. Only one house caught fire, and the money from that house walked three doors down and rang the doorbell.

DeFi Has Been to This Funeral Before

The Original Test

Here’s the part the doom coverage keeps skipping.

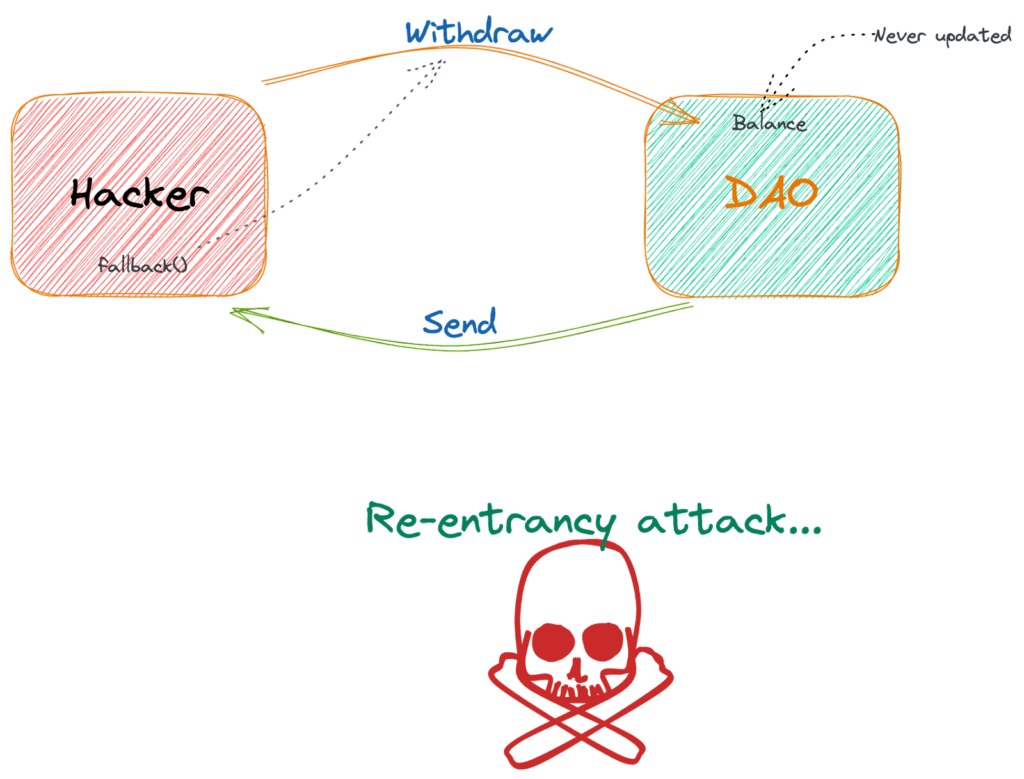

In 2016, The DAO was drained of $60 million, about 14% of all the ETH in circulation at the time. The response was a hard fork that rolled back the theft, split the community, and created the Ethereum/Ethereum Classic divide that still exists. It was messy, controversial, and in the purist reading, a clean violation of “code is law.”

It was also the right call. Ethereum didn’t die from it. It became the settlement layer for basically everything that followed. Including Aave.

The Pattern Since

The pattern holds up under pressure. Wormhole lost $320M in 2022 and kept operating. Ronin lost $625M the same year and rebuilt. Euler got drained for $197M in 2023 and recovered nearly all of it. Each time, the obituary got written early. Each time, the protocol outlived the headlines.

Why Aave Isn’t Even the Worst Case

Aave isn’t in the worst position on that list. Its contracts weren’t compromised. The attack exploited an external bridge’s verifier setup, not a line of Aave’s code. The protocol has a ~$181M Umbrella insurance fund ready to absorb losses, outside partners offering to top it up, and an incident report already published with LlamaRisk laying out the loss scenarios transparently.

That last part matters. You don’t get transparency like that from a protocol that’s hiding a wound.

What Actually Shifts After This

A few things will move, and they’re worth naming clearly.

Aggressive LTVs on Liquid Staking Are Done

93% LTV on liquid-staking tokens is probably finished as a product category. Aave enabled it through E-Mode. Maker capped the equivalent at 72%. Maker was right. Expect Aave’s next risk parameters to look a lot more like Spark’s.

Single-Verifier Bridges Won’t Survive the Quarter

LayerZero’s 1-of-1 default sat in front of too many integrations. Curve, Ethena, BitGo and others halted their LayerZero bridges within hours. The industry has seen enough. One verifier is not a security model. It’s a single point of failure wearing a lanyard.

The Admin Key Debate Is Back, Honestly This Time

Aave’s freeze worked. It also reminded everyone there’s a hand on the brake. Users who want pure trustlessness have to reckon with the fact that pure trustlessness would have let the attacker keep borrowing. That’s an uncomfortable conversation the ecosystem has been avoiding. It can’t avoid it anymore.

None of these are existential. They’re the normal way a maturing system absorbs a hit and tightens up.

If You’re an Aave Depositor Reading This

What You Were Actually Reacting To

Nobody’s going to tell you pulling funds this week was wrong. Caution is free. But understand what you were actually reacting to.

- Your deposits weren’t stolen

- Aave’s contracts weren’t hacked

- The insurance fund exists for exactly this

- The worst-case loss is smaller than the reserve

- Capital is rotating inside DeFi, not fleeing it

The Institutional Pause Is a Feature, Not a Bug

The Jefferies note Bloomberg ran with, the one warning banks might “pause and reassess” their blockchain plans, is probably right. And it’s probably healthy. Institutions should want better bridge security before they put serious size on-chain. A market that slows down to check the locks before the next wave of capital arrives is a market that plans to be here in ten years.

The Verdict

Aave getting hit doesn’t mean Aave is broken. It means the bridge was.

The protocol responded in minutes. The insurance fund exists for exactly this. The incident report is public. The capital that left is sitting in another DeFi lender, not in a bank. And every major exploit in crypto history, from The DAO forward, has ended the same way. The protocol that took the punch tightens its parameters. The ecosystem routes around the broken piece. Six months later, the headlines have moved on.

This one will too.

The real question isn’t whether Aave survives. It’s whether you’re paying attention to what the survival actually teaches. The weak link is almost never the lender. It’s the thing standing behind the lender that nobody was looking at.

This time it was a bridge. Next time it’ll be something else. The protocols that survive are the ones that freeze fast, report honestly, and pay from reserves they built in advance. Aave just did all three.

This article is for informational purposes only and does not constitute financial advice. Please DYOR. You can also DYOR on blog.millionero.com. When ready, trade spot and perps on Millionero.