This week brought a mix of institutional expansion, macro tension, infrastructure stress, and fast-moving changes across crypto markets. BTC stayed at the center of attention, but the wider picture also included Ethereum flows, Solana and Sui positioning, TON’s sharp move, tokenized equities, DeFi security, and new policy signals from the United States, Japan, Australia, and China.

Bitcoin, Ethereum, and the Broader Market

Bitcoin flows, price action, and profit pressure

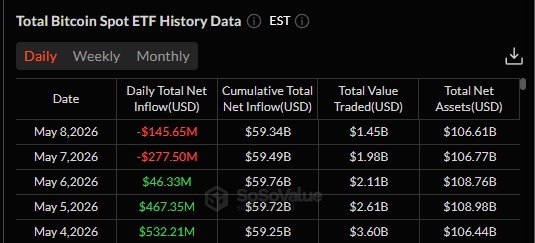

BTC ETFs recorded a cumulative net inflow of $622.75 million this week. During the same period, Bitcoin posted a weekly low of $78,100, a weekly high of $82,800, and was sitting at $80,200 at the time of the update.

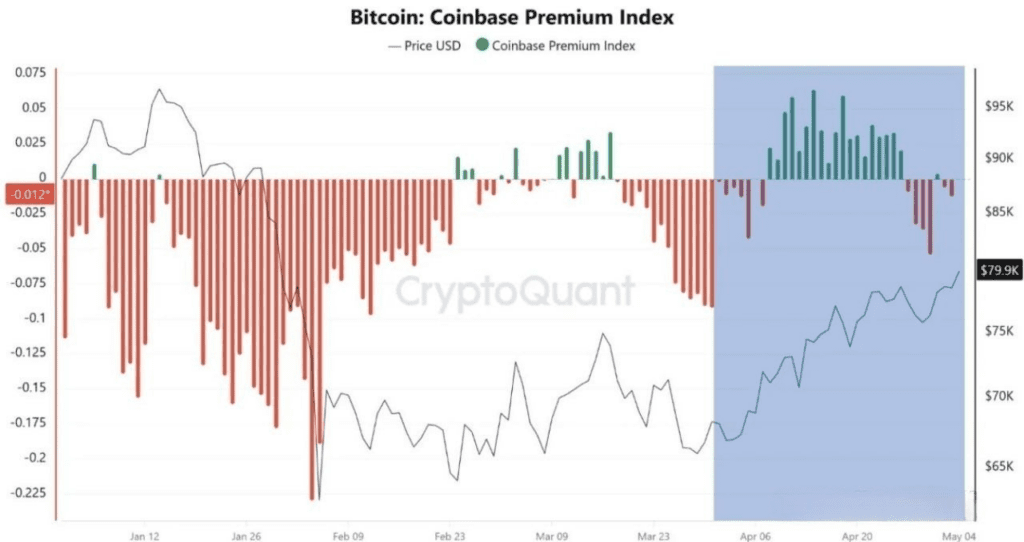

At the same time, CryptoQuant data showed that actual demand for Bitcoin was active during April, while Ethereum’s move higher appeared to come more from lower selling pressure than from strong demand. That suggested a shift in liquidity inside the market rather than a full recovery.

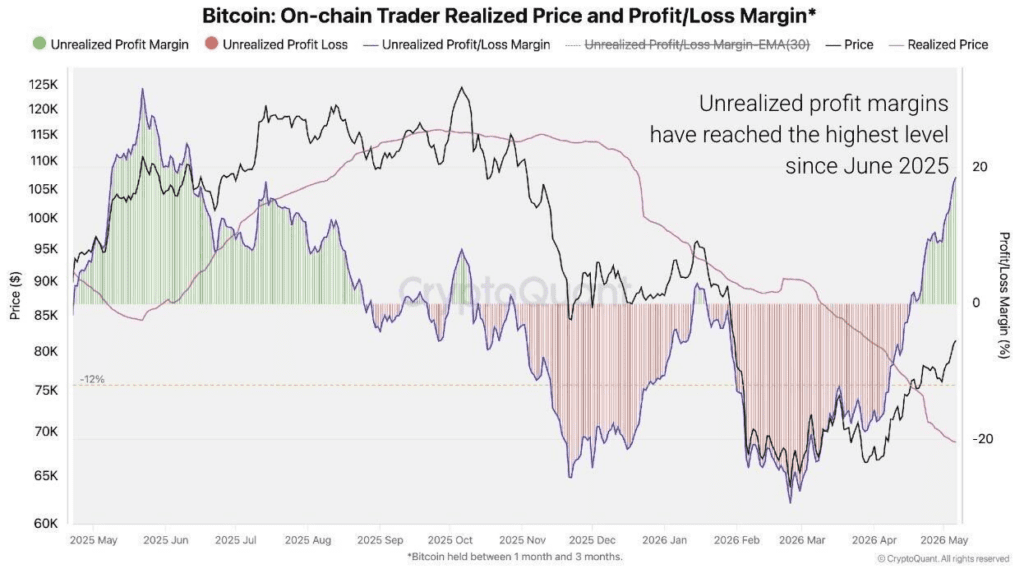

CryptoQuant data also showed that Bitcoin traders were sitting on their highest unrealized profits since June 2025. The same update noted that this profit ratio has historically come before selling pressure, leaving the market between two possibilities: either profit-taking starts and a correction follows, or the rally keeps going.

Ethereum selling, Ethereum buying, and mixed positioning

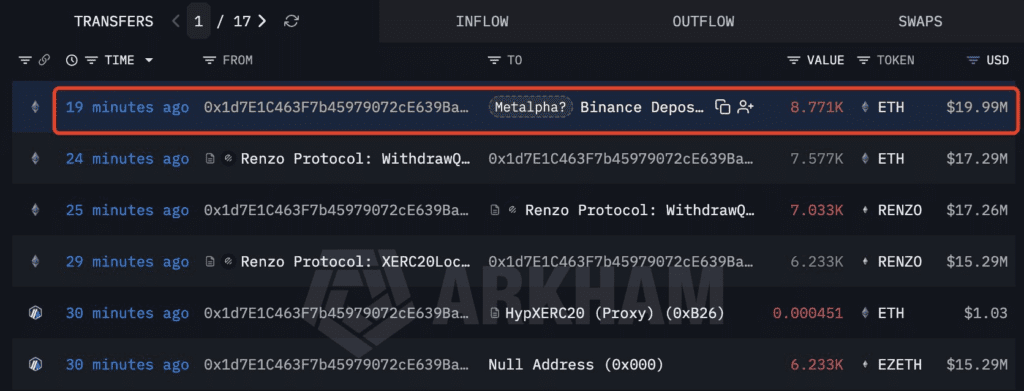

Ethereum flows pointed in both directions this week. On the selling side, another wallet linked to Metalpha deposited 8,771 ETH, worth nearly $20 million, to Exchanges. Moves of that size kept attention on the risk of continued selling pressure.

On the buying side, two new accounts withdrew a combined $94.6 million in Ether from Kraken. The pattern reportedly resembled earlier buying activity linked to BitMNR, which raised fresh questions over whether Tom Lee was still accumulating Ethereum.

Solana, Sui, and TON compete for attention

Solana remained part of the institutional conversation. The shift of institutions toward Solana had already started, with the chief executive of Bitwise saying that Goldman Sachs, Morgan Stanley, and Citadel had begun building investment positions in Solana during 2026.

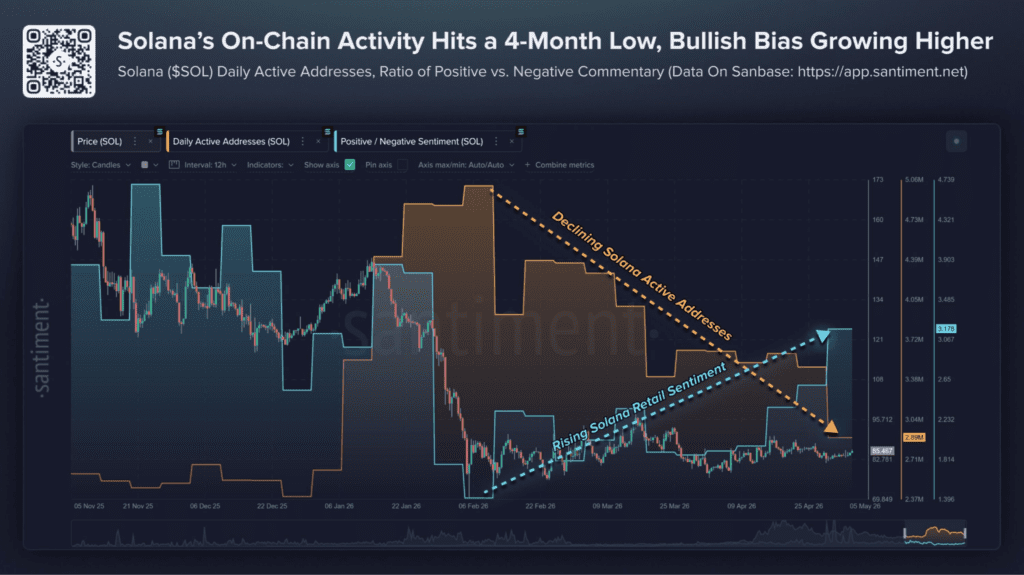

Even so, on-chain activity on Solana weakened. Weekly active addresses fell to 2.89 million, down from 5.01 million in February, while social sentiment reached its highest level since January, according to Santiment.

Sui took a more aggressive product approach. The network said stablecoin swaps would be available with zero fees, regardless of amount or usage volume, in a sign that sui:native was entering competition more directly.

A separate discussion around Sui focused on user acquisition. The argument was that the network is not targeting Ethereum or Solana users first, but rather the much larger group of people still outside crypto, including the billions already active on platforms such as Instagram and TikTok. Social-media logins instead of complex wallets were presented as the main path, along with zero-knowledge technology that can hide user activity from platforms like Facebook.

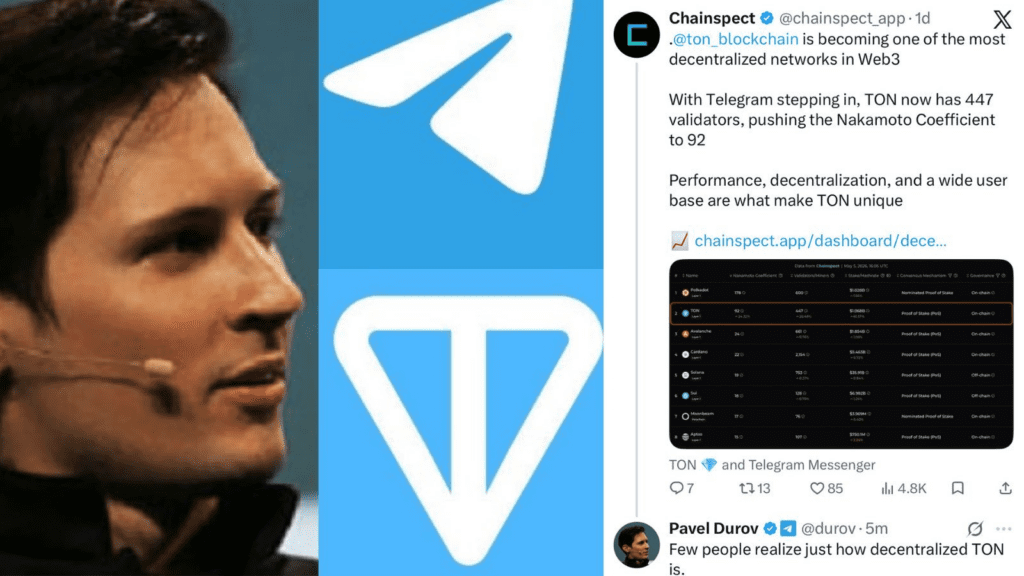

TON had one of the sharpest moves of the week. Its market cap was reported to have doubled in four days, rising from $3.6 billion to $7.3 billion, a 100% increase. The move was tied to Telegram’s growing dominance over the ecosystem.

That theme was reinforced again when Pavel Durov said that few people realize the extent of decentralization that the TON network enjoys, as the TON ecosystem continued to expand inside Telegram through more blockchain-based services and applications.

Institutional Adoption and Financial Infrastructure

ETFs, ETPs, and the next stage of market access

Institutional access to crypto widened further this week. Japan Exchange Group (JPX) said it was preparing to launch Bitcoin and crypto ETFs, according to Bloomberg. In parallel, Japan was also reported to be moving government bonds to blockchain infrastructure, with plans for 24-hour trading and stablecoin settlement that could begin this year.

In Europe, BlackRock’s iShares Bitcoin ETP (IB1T) passed $1.1 billion in assets under management and was reported to hold about 14,200 BTC. The product is listed on Euronext Paris, Euronext Amsterdam, and Xetra, extending the reach of institutional Bitcoin products in the region.

Another market view came from Bloomberg analyst Eric Balchunas, who said Bitcoin ETFs are reshaping the relationship between crypto and traditional finance. His argument was that the market still underestimates the efficiency and distribution power of the traditional financial system for the average user.

Banks, custody, and portfolio positioning

Wall Street’s re-entry into crypto also became more visible. Bloomberg reporting said major financial institutions had started hiring dozens of people in digital-assets roles. The point was that the next adoption wave may not be only ETF liquidity, but also banks building specialized crypto teams before a stronger return in demand.

BNY Mellon, with more than $59 trillion in assets under custody, was reported to be planning digital-asset custody services in Abu Dhabi, starting with Bitcoin and Ethereum.

At the portfolio level, Morgan Stanley digital-assets strategist Amy Oldenburg recommended allocating 2% to 4% of portfolios to Bitcoin. She also said Bitcoin could eventually enter U.S. bank balance sheets, though more slowly than many expect because of regulation. The obstacles she listed included Federal Reserve guidelines, Basel rules, and legal differences across countries. She added that adoption is still slow among advisors because of limited awareness and education.

At Consensus 2026, Eric Trump said JPMorgan had mocked Bitcoin just 18 months ago, but now allows BTC holdings to be used as collateral for mortgages. His point was that institutional attitudes can change very quickly.

CME, round-the-clock trading, and changing market structure

CME Group said it intends to launch Bitcoin futures contracts on June 1, pending approval from the CFTC. The product was described as the first regulated financial derivative designed to measure Bitcoin volatility, giving institutions a more advanced tool for trading and risk management.

Another CME change may be even more structural. CME announced that its crypto futures and options would be available for trading 24/7 starting May 29. That was framed as the possible end of the long-running BTC CME gap trade narrative.

Tokenized equities and tokenized shares move forward

Tokenized company stocks continued to grow quickly. Total value locked in the sector was reported to have risen from nearly zero to more than $1.25 billion in less than a year. Ondo Global Markets alone was said to account for more than $920 million, with one figure also putting it at $900 million+. The broader case for tokenized stocks was presented through ideas like global access and productive collateral.

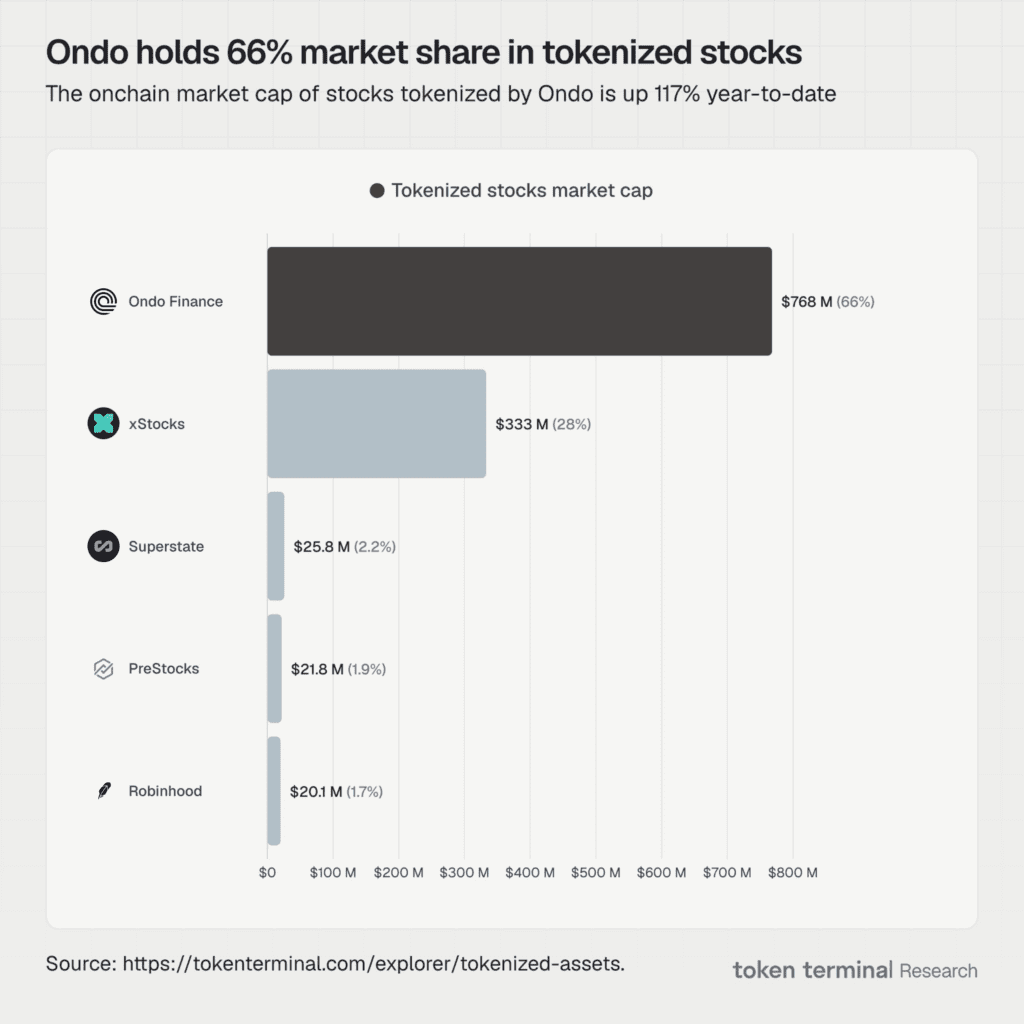

This theme came up again in another update that said Ondo Finance controls 66% of the tokenized equities market, that the sector has now passed $1 billion, and that growth since the start of the year has reached 117%. That same discussion argued that SEC regulatory support is helping create room for expansion.

A separate product launch added to that trend. Securitize was reported to be preparing tokenized stocks on Solana in partnership with Jump Trading and Jupiter Exchange. Under that structure, Jump would provide institutional liquidity through PropAMM, while Jupiter would handle user and institutional access through its trading interface.

Tokenized shares were also pushed forward through $STRC, described as a tokenized Strategy company share made available via Ethereum, BNB Chain, and Solana through Ondo Finance. One update described the product as offering an 11.5% monthly return.

That launch connected directly to the week’s wider discussion around Strategy. Saylor said Strategy may need to sell part of its Bitcoin to cover STRC dividend distributions. The figures attached to that point were significant: $8.5 billion in total STRC funding, an 11.5% annual yield paid monthly, around $82 million in monthly distributions, and $2.2 billion in current liquidity. The update also said the roughly $82 million raised the previous week was used to cover distributions rather than buy more Bitcoin, showing that some cash flow had started shifting from buying Bitcoin to servicing financial obligations.

Payments and stablecoins

Traditional payments also moved closer to blockchain rails. Western Union launched its USDPT stablecoin on Solana, in what was described as another step toward linking traditional payments with blockchain infrastructure.

The venture side also stayed active. Andreessen Horowitz launched a $2.2 billion crypto fund focused on projects that combine crypto, artificial intelligence, and traditional finance. The move came during a period in which AI companies had already attracted more than $240 billion in inflows during the first quarter of 2026, reinforcing the idea that the next large bet may be the merger of AI with new financial infrastructure.

Regulation, Policy, and Geopolitics

U.S. policy and legal direction

In Washington, the Regulatory Clarity Act was described as moving closer to approval before the end of summer. Coinbase’s chief legal officer, Paul Grewal, said he was very confident the bill would pass in the coming months. He also urged banks to accept the agreement, warning that refusing it could leave them facing less flexible legislation such as the GENIUS Act.

At the agency level, SEC chair nominee Paul Atkins said the SEC is working with the CFTC to deliver long-awaited regulatory clarity for digital assets in the United States. The stated goal was to support innovation in the sector.

AI policy and cybersecurity risk

Outside crypto, artificial intelligence became part of the policy picture. The Australian Securities and Investments Commission (ASIC) called on the financial sector to take urgent cybersecurity measures against threats posed by advanced AI models. The warning explicitly included models such as Mythos from Anthropic, reflecting concern that AI systems are becoming more capable of carrying out attacks and breaching systems.

The United States and China were also reported to be studying formal talks on AI, with the stated aim of preventing technological competition from turning into a wider global crisis. According to The Wall Street Journal, AI is expected to be one of the main issues in the upcoming Trump–Xi Jinping summit in Beijing next week.

Oil, Iran, and the politics around price moves

Geopolitics fed directly into markets all week. The U.S. Department of Justice was reported to be investigating $2.6 billion in oil deals executed just before major statements by Donald Trump regarding the war with Iran. The trades reportedly bet on a drop in oil prices only minutes before market-moving political announcements, raising questions about whether undisclosed information had been exploited for outsized profits.

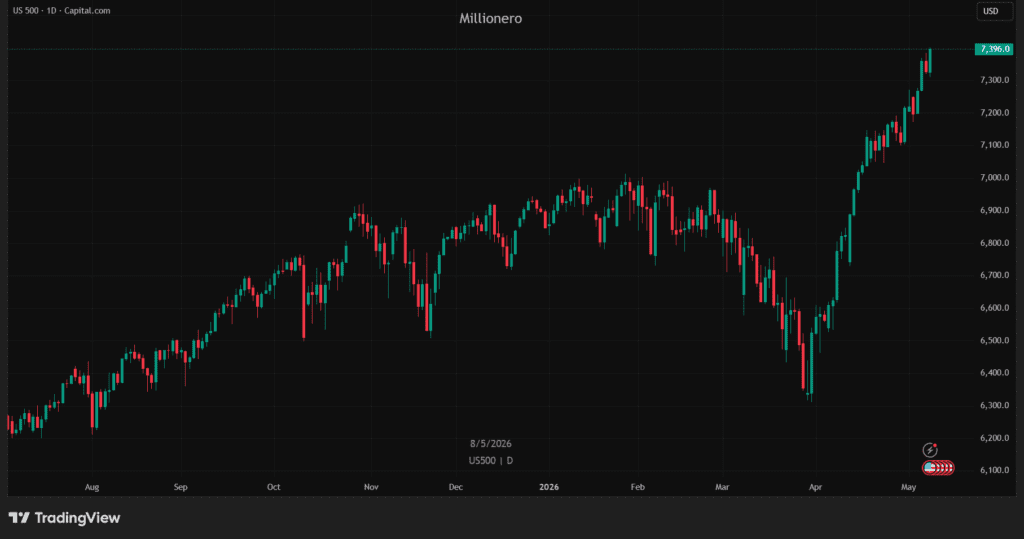

At the same time, expectations around a possible Iran–United States deal helped lift broader risk sentiment. The S&P 500 was said to have reached a new peak of $7,396 on hopes that such a deal would go through.

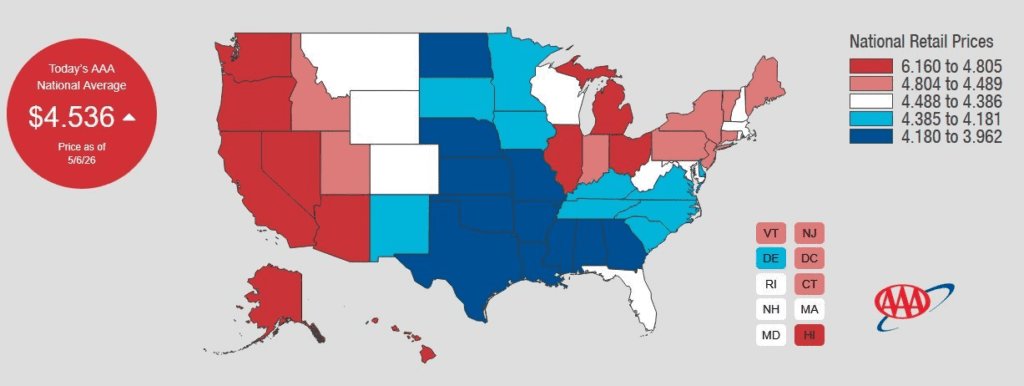

That same regional tension also showed up in energy commentary. The average gasoline price in the United States was reported at $4.53, its highest level in nearly four years and just 50 cents below the 2022 record. Inventories were described as the lowest seasonal levels in 12 years, while summer demand was rising quickly. The conclusion was that prices could keep climbing, which would add pressure on Trump to secure a deal and a faster de-escalation. In a related report, Iranian media claimed that a U.S. warship had been hit by two missiles, while U.S. Central Command firmly denied that any American ship had been targeted.

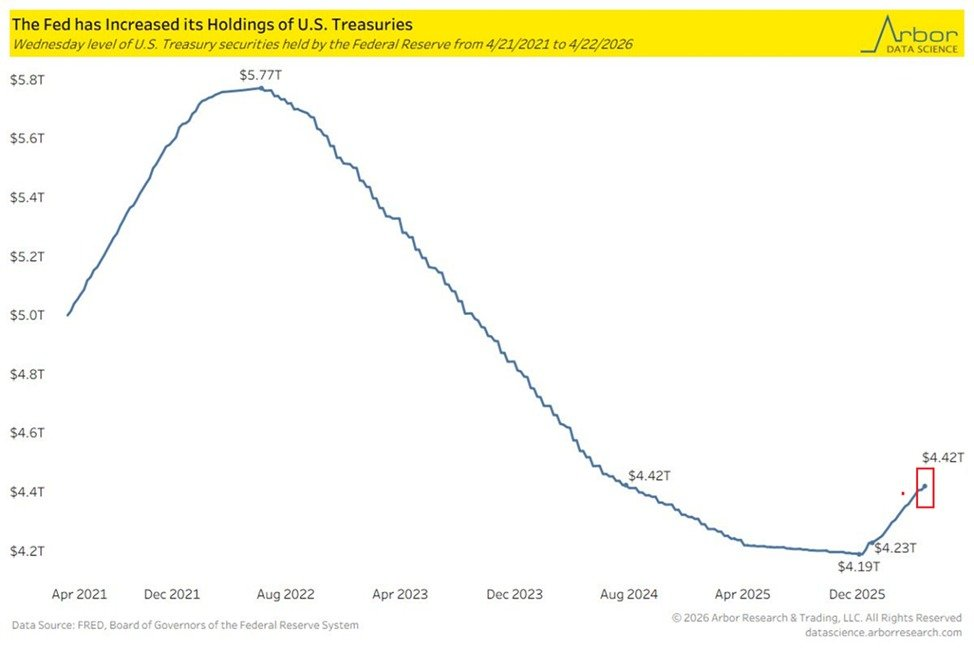

Liquidity conditions also drew attention. The Federal Reserve’s holdings of Treasury bonds were reported at $4.4 trillion, their highest level since July 2024, while total Fed assets were said to have reached $6.7 trillion. The move was presented as another sign that liquidity is returning and that expansion is reappearing in the broader balance sheet.

Japan and the yen

Japan also remained under pressure on the currency side. The Bank of Japan was described as doing everything it could to support the yen, but still struggling to push the exchange rate below 155 per dollar. The argument was that intervention and reserve use may only be buying time, and that the real turning point would require a consistent cycle of rate hikes.

Latin America and Bitcoin mining

In Latin America, Colombian President Gustavo Petro called on Colombia to follow Venezuela and Paraguay in attracting Bitcoin mining investment.

DeFi, Security, and On-Chain Infrastructure

KelpDAO fallout and the wider hack landscape

Security remained a major theme. KelpDAO decided to move rsETH to Chainlink CCIP after concluding that LayerZero’s infrastructure was the main reason behind the April breach. That attack was said to have caused losses of more than $300 million across DeFi.

The broader context made the move easier to understand. One recap described April 2026 as a brutal month for crypto, with 25 hacks in 29 days and more than $629 million stolen. The latest case in that running tally was the Sweat Economy hack, where $3.46 million—equal to 65% of supply—was reportedly withdrawn in just 30 seconds. The pace worked out to roughly one hack every 27 hours, with the warning that the month was not even over yet.

Aave, Pendle, and fixed-yield structure in DeFi

The KelpDAO case also spilled into legal protection efforts. An emergency request linked to Aave sought to prevent the seizure of roughly $71 million in ETH that had been set aside to compensate victims of the KelpDAO hack. The purpose was to protect those funds from being redirected elsewhere.

Another major DeFi development came from Pendle, where PT usage was activated as collateral on Aave. The change was presented as the first way to build leveraged fixed-yield positions in a more complete form: buy PT with a fixed yield of around 25% to 30%, use it as collateral, borrow against it, and re-enter the trade. The setup was described as the closest thing to zero-coupon bonds on the blockchain.

The wider case for that market was also laid out clearly. Traditional finance has a fixed-income market above $30 trillion, while DeFi has lacked mature fixed-yield infrastructure. This week’s figures added support to the story: about $50 million in RWA inflows, TVL at an all-time high, and a market cap of roughly $271 million, still 78% below its peak. With products such as BUIDL and OUSG, the argument was that a stronger yield-trading market is becoming necessary. If DeFi fixed income reaches even $10 billion, current pricing may still be far from fair value.

Exchange and cloud infrastructure stress

Infrastructure risk surfaced in a more traditional way as well. Coinbase experienced service disruptions because of high temperatures inside an AWS US-EAST-1 data center. The company said trading would first resume in cancel-only mode before full operations returned. The episode underlined how vulnerable even the largest crypto platforms remain to failures in the underlying technology stack.

The Week in Context

Taken together, the week showed a market moving on several tracks at once. Bitcoin kept drawing capital through ETFs and institutional products, but profit pressure and macro risk never disappeared. Ethereum showed both whale selling and whale accumulation. Solana, Sui, and TON each pushed a different growth story. Tokenized equities, tokenized shares, and stablecoins moved further into mainstream finance. At the same time, AI policy, oil politics, Japan’s currency fight, DeFi hacks, and exchange infrastructure failures all reminded the market that adoption is still happening inside a very unstable global environment.

Read more market breakdowns on the Millionero Blog, and if you want to explore the market yourself, you can trade on Millionero. This is not financial advice.