What Changed Over the Weekend

The weekend was dominated by two connected stories: a fast-moving shift in the US-Iran war timeline and a new jump in energy risk. At the same time, crypto and macro markets gave a mixed but important signal. Bitcoin stayed stuck in a slow range near $69,000, spot crypto trading activity looked weak, Ethereum accumulation continued in the background, and several market-sensitive US data releases moved into focus for the days ahead.

The biggest headline was the report that the United States and Iran were discussing a 45-day ceasefire deal that could lead to a permanent end to the war. Regional mediators were said to be pushing a two-phase plan as the Tuesday 8:00 PM ET deadline approached. That was not a small update. It came after repeated deadline changes over the last 17 days, with the timeline shifting again and again:

- March 21: 48-hour deadline

- March 23: 5-day extension

- March 26: 10-day extension

- April 4: 48-hour deadline

- April 5: Postponed to April 7

This was described as the fifth deadline change in 17 days. The pattern around these deadlines has become part of the market story. Each time a deadline gets close, an extension appears and markets calm down. Then, after markets recover, the message shifts again and the threat of continued strikes returns. That uncertainty is now one of the main reasons volatility remains high.

The Iran Deadline Kept Moving Again

Negotiations were still active behind the scenes

Over the weekend, there were also reports that the President’s advisers were directly texting Iranian Foreign Minister Araghchi in an effort to keep negotiations alive. The talks were also said to be moving through Pakistani, Egyptian, and Turkish mediators. That mattered because it showed the diplomatic track was still open, even while public threats were getting stronger.

At the same time, the so-called “48 hour deadline” was extended again, this time to roughly 82 hours. The earlier deadline, set on Saturday, was due to expire on Monday at 10:05 AM ET. Then the public message changed to “Tuesday, 8:00 P.M. Eastern Time!” In effect, the deadline for possible US strikes on Iranian power plants shifted again.

Markets still had to price the threat of escalation

Even with negotiations still active, the market opened the week by reacting to escalation risk. US stock index futures fell as the President described Tuesday as “Power Plant and Bridge Day” in Iran. At the open:

- S&P 500 futures fell 0.7%

- Nasdaq 100 futures fell 0.8%

- Dow Jones futures fell 0.7%

- WTI Crude rose 3.0%

- Natural Gas rose 1.0%

- Gold fell 0.9%

At that point, the deadline was said to be about 50 hours away. Bitcoin, by contrast, was still sitting near $69,000 in the same slow range as before. That contrast was important. Traditional markets reacted immediately to war risk, but Bitcoin had not yet broken out of its holding pattern.

Oil Became the Main Macro Pressure Point

Crude moved above $114 as futures reopened

The strongest direct market move over the weekend came in energy. US oil prices surged above $114 per barrel as US market futures reopened after the three-day weekend. That move came as traders priced in a larger threat to supply, not just another round of rhetoric.

The escalation risk expanded further after a key adviser to Mojtaba Khamenei, described as Iran’s new Supreme Leader, threatened to close the Bab al-Mandab Strait, which connects the Red Sea to the Gulf of Aden. The warning was blunt: if Washington repeated what was described as past mistakes, global energy and trade flows could be disrupted with a single signal.

Supply risk grew beyond one chokepoint

That threat mattered because the numbers were large. Roughly 7 million barrels of daily oil supply move through Bab al-Mandab, and about 22% of global seaborne container trade passes through the strait each year. When that risk is added to the already critical Strait of Hormuz, the market is now looking at the possibility that as much as 25 million barrels per day of oil supply could go offline.

There was another important detail here as well. Iran was said to have rejected a US proposal to reopen the Strait of Hormuz in exchange for a temporary ceasefire. That left the oil market with a harder problem. Instead of a quick reduction in risk, traders had to think about a setup where oil could move toward $120+ per barrel.

Crypto Markets Enter the Week With Weak Volume but Selective Buying

Bitcoin stayed flat while broader crypto activity slowed sharply

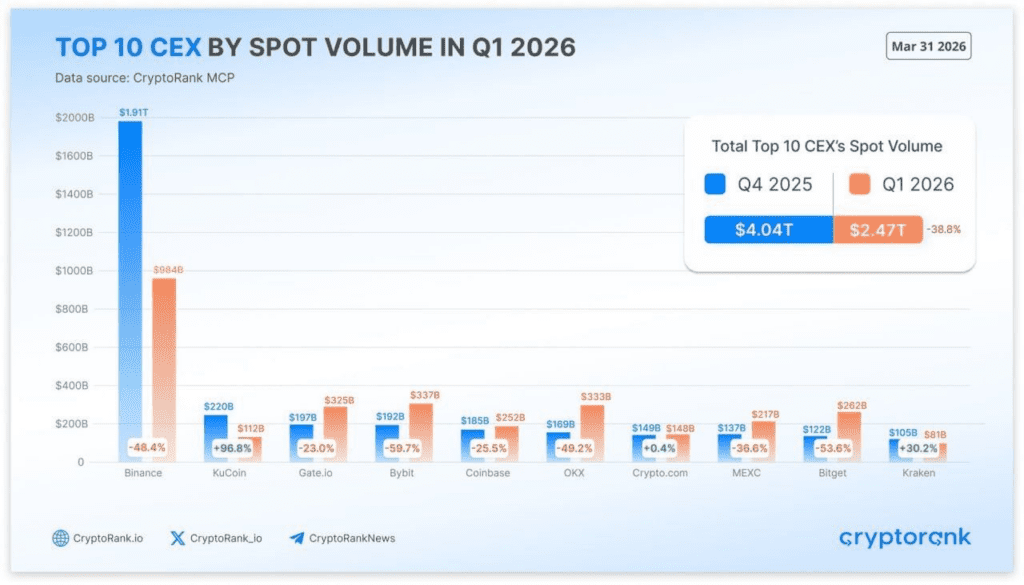

Even before the new week’s events began, crypto markets were already showing signs of caution. Spot trading volume across the top 10 exchanges fell 39% in Q1 2026, dropping from $4.04 trillion to $2.47 trillion. That was described as the lowest level in a long time and reflected a climate of fear and uncertainty.

That helps explain why Bitcoin could remain near $69,000 without a stronger directional move. The market is not empty, but participation looks weaker, and that often leaves price action slower until a larger catalyst arrives.

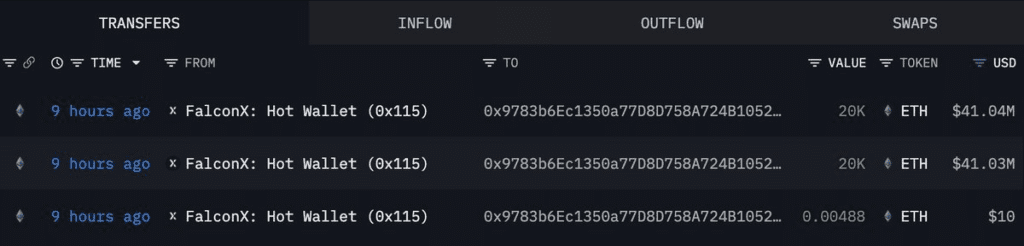

Ethereum saw a major weekend accumulation move

While broad activity looked soft, one large buyer kept moving. Bitmine bought around 40,000 ETH worth $82.07 million from FalconX in a fresh purchase over the weekend. The move was described as another step in Tom Lee’s continued accumulation, done without hesitation despite the market fog.

That gave the weekend a split tone inside crypto. Broad volumes remained weak, but selective institutional-style buying was still happening in size.

Compliance and Market Structure Stayed in Focus

Circle faced new scrutiny over frozen funds and compliance timing

One of the most serious crypto-specific developments over the weekend was a report alleging major compliance failures at Circle since 2022, totaling more than $420 million.

The figures listed in the report were highly specific:

- 232 million USDC bridged during the Drift Protocol hack without being frozen

- 3 million USDC in the SwapNet hack

- 61 million USDC in the Cetus hack

- 57.5 million USDC linked to the Mango Markets attack

- 45 million USDC in the Nomad Bridge hack

The broader issue was not just the dollar amount. It was the question of whether stolen funds can be frozen in time, and whether delays in doing so weaken Circle’s regulatory credibility at a sensitive moment. The claims were also presented alongside a link to a full report, which kept the issue alive going into the new week.

Gold and the Labor Market Added Another Layer to the Outlook

Gold kept its support even after a pullback

Outside crypto, UBS said the case for gold still looks strong despite the recent pullback, with a year-end target of $5,900 per ounce. That call mattered because it showed that even after recent price softness, some major institutions still see strong support for defensive assets.

Powell’s warning raised concern about the jobs engine

A much more immediate concern came from Jerome Powell, who said that what worries policymakers is that net private sector job creation has reached zero. That is a direct and serious warning. It suggests the private side of the US labor market may have stalled, or at least slowed enough to raise concern at the top of the Federal Reserve.

That one comment linked directly to this week’s upcoming data. If private job creation is no longer adding net growth, then markets will pay even closer attention to inflation reports, consumer data, and anything in the Fed minutes that helps explain how officials are weighing weak labor conditions against still-important inflation risks.

The Key US Events This Week

Markets are entering a very sensitive week

This week’s calendar is heavy even without the geopolitical pressure. With oil rising, war headlines moving markets, and labor market concerns growing, every major US release now matters more.

The key events listed for the week are:

- Markets React to Trump’s “48 Hour Warning” – 6 PM ET Today

- March ISM Non-Manufacturing data – Monday

- Trump’s “Iran Power Plant and Bridge Day” – Tuesday

- Fed Meeting Minutes – Wednesday

- February PCE Inflation data – Thursday

- US Q4 2025 GDP data – Thursday

- March CPI Inflation data – Friday

- April MI Inflation Expectations data – Friday

- April MI Consumer Sentiment data – Friday

The expectation going into all of this is extreme volatility.

Why Wednesday’s Fed Minutes matter

The Fed Meeting Minutes matter because markets want to see how deeply officials are worried about the balance between inflation and labor market weakness. If the minutes show stronger concern about growth and jobs, traders may start thinking more seriously about a softer rate path later on. If they show that inflation is still the main concern, then the Federal Reserve may have less room to turn supportive even if labor conditions weaken.

Why Thursday’s PCE and GDP data matter

The February PCE Inflation data is especially important because PCE is one of the Federal Reserve’s most watched inflation gauges. A softer number would help the case that inflation is moving in the right direction. A firmer number would make it harder for the Fed to move toward rate cuts, especially if oil stays elevated.

The US Q4 2025 GDP data matters for a different reason. It shows how much underlying growth strength the economy had going into this period of higher geopolitical stress. Strong GDP can give the Fed more room to stay patient. Weak GDP, combined with slower job creation, would make the overall picture look more fragile.

Why Friday’s CPI and Michigan data could be decisive

Friday may be the most important day of the week. The March CPI Inflation data will give the market a direct read on consumer inflation. If CPI runs hot while oil is rising and conflict risk remains high, concerns about sticky inflation will likely return quickly.

At the same time, the April MI Inflation Expectations data will show what households think inflation will do next. That matters because inflation expectations can shape future pricing behavior. The April MI Consumer Sentiment reading will then add another piece by showing how consumers are feeling under the pressure of higher uncertainty, weaker hiring concerns, and rising energy costs.

Taken together, these releases will help markets answer a basic question: is the US economy moving toward a softer growth and labor environment that could pull the Fed in a more supportive direction, or is inflation still strong enough to keep rate decisions tight for longer?

Crypto Unlocks This Week

Aptos (APT)

Date: April 12

Unlock Value: 9.5M USD

% of Circulating supply: 0.68%

Number of Tokens: 11.31M APT

Babylon (BABY)

Date: April 11

Unlock Value: 7.8M USD

% of Circulating supply: 37.77%

Number of Tokens: 612M BABY

Linea (LINEA)

Date: April 10

Unlock Value: 4.5M USD

% of Circulating supply: 5.32%

Number of Tokens: 138M LINEA

RedStone (RED)

Date: April 7

Unlock Value: 4.2M USD

% of Circulating supply: 13.89%

Number of Tokens: 40.85M RED

Movement (MOVE)

Date: April 9

Unlock Value: 2.9M USD

% of Circulating supply: 4.92%

Number of Tokens: 164M MOVE

io.net (IO)

Date: April 11

Unlock Value: 1.3M USD

% of Circulating supply: 0.68%

Number of Tokens: 11.31M IO

Final View Going Into the Week

The weekend did not give markets a clean answer. It gave them a tighter knot. There are still reports of ceasefire talks, but the Iran deadline keeps moving. Oil has already moved above $114, and the threat to supply through Hormuz and Bab al-Mandab remains serious. Crypto volume is weak, but selective large buying in Ethereum continues. Circle is facing fresh compliance questions. Gold still has strong support from a major bank. And Powell has put a spotlight on a labor market warning that markets cannot ignore.

That leaves the week ahead with a clear structure. First, markets have to digest what happened over the weekend. Then they have to process a full run of US events, from ISM Non-Manufacturing to Fed Minutes, PCE, GDP, CPI, and the Michigan data. In a week like this, inflation, labor, Fed expectations, war risk, and energy prices are not separate stories. They are all part of the same one.

This article is for general information only and should not be considered financial advice. Markets can change quickly, especially when geopolitics, inflation, and Fed expectations are all moving at once. Read our blogfor the full market view, and if you choose to act, trade responsibly on Millionero.