A Week Where Relief Rallies and Structural Risks Moved Together

This week did not move in one direction. Markets recovered from the shock of the US-Iran conflict, but the deeper pressure never fully disappeared. The Strait of Hormuz remained unstable even after the ceasefire framework. Oil stayed sensitive. Inflation rose again because of energy. The labor market kept weakening. And while some investors pushed back into risk assets, others stayed cautious.

At the same time, crypto had its own major shifts. Bitcoin ETF volumes stayed heavy, Bhutan kept cutting its Bitcoin holdings, Strategy added more BTC, Hyperliquid saw major oil-perps activity, Bittensor was hit by a decentralization dispute, World Liberty Financial faced both defense and scrutiny, and fresh narratives emerged around Ethereum, Ripple, XRP, Chainlink, Solana, and Telegram.

The Middle East Story Still Set the Tone

The ceasefire mattered, but Hormuz never fully normalized

A major part of the week centered on the two-week ceasefire framework linked to Pakistani mediation. The key points described in the proposal were a complete halt to military operations and airstrikes, the reopening of the Strait of Hormuz to protect global energy flows, and the start of direct diplomatic negotiations aimed at reaching a more sustainable solution.

But even with that framework in place, the Strait did not return to normal. One update described a near-complete paralysis in Hormuz despite the ceasefire. No oil or gas tankers had crossed the strait since the ceasefire announcement, and only four dry cargo ships had passed through.

Later, another report said Iran was struggling to fully reopen Hormuz because it could not locate all the sea mines it had deployed and lacked the ability to remove them all. That was one of the clearest signs this week that the Hormuz problem was no longer only political. It had also become operational.

Diplomacy kept moving, but the pressure remained high

By the end of the week, Iranian negotiators arrived in Pakistan ahead of peace talks with the United States scheduled for the weekend. That kept the diplomatic track alive.

At the same time, South Korea moved directly because of the Hormuz crisis. It said it would send a special envoy to Iran to secure safe passage for dozens of ships stranded in the strait, despite the ceasefire agreement between Washington and Tehran.

This showed how wide the Hormuz issue had become. It was not only about the US and Iran. It was also about global shipping, trade continuity, and the ability of outside countries to protect their own commercial exposure.

Trump’s warnings and Iran’s response kept the conflict alive in markets

Early in the week, Trump warned Iran that if it failed to respond by 8:00 PM Eastern Time the next day, it could face a return to the “Stone Age,” with the possible destruction of infrastructure in a single night.

Iran then presented a 10-point reply to the US peace plan. The main points included:

- Security guarantees against another attack on Iran

- A permanent end to the war and the full lifting of US sanctions

- A halt to Israeli attacks in Lebanon and fighting against Iran’s allies

- Reopening the Strait of Hormuz with a $2 million transit fee per ship

- Sharing those fees with Oman and using them for reconstruction

The same flow of updates said Trump was also considering special “toll” fees on passing ships and viewed the lack of a clear Iranian response as a possible sign of full-scale confrontation.

Another report, linked to a two-phase proposal led by Pakistan, said the plan called for the immediate reopening of the strait.

Additional geopolitical pressure kept building

This week also brought reports that Iran may require ships passing through Hormuz to pay passage fees, with the possibility of accepting Bitcoin or other currencies as payment.

At the same time, Trump said that any country providing military weapons to Iran would face a 50% tariff on all goods exported to the United States, with no exceptions or exemptions.

He also attacked NATO again, saying it had not existed when it was needed and would not be there if it was needed again, while sarcastically pointing to Greenland as a badly managed “big piece of ice.” A broader political commentary around this framed him as acting as if he were playing geopolitical Monopoly, moving from Venezuela to Iran, Cuba, and even Greenland in a much wider expansionist mood.

Oil, Inflation, and the Federal Reserve Stayed Tightly Linked

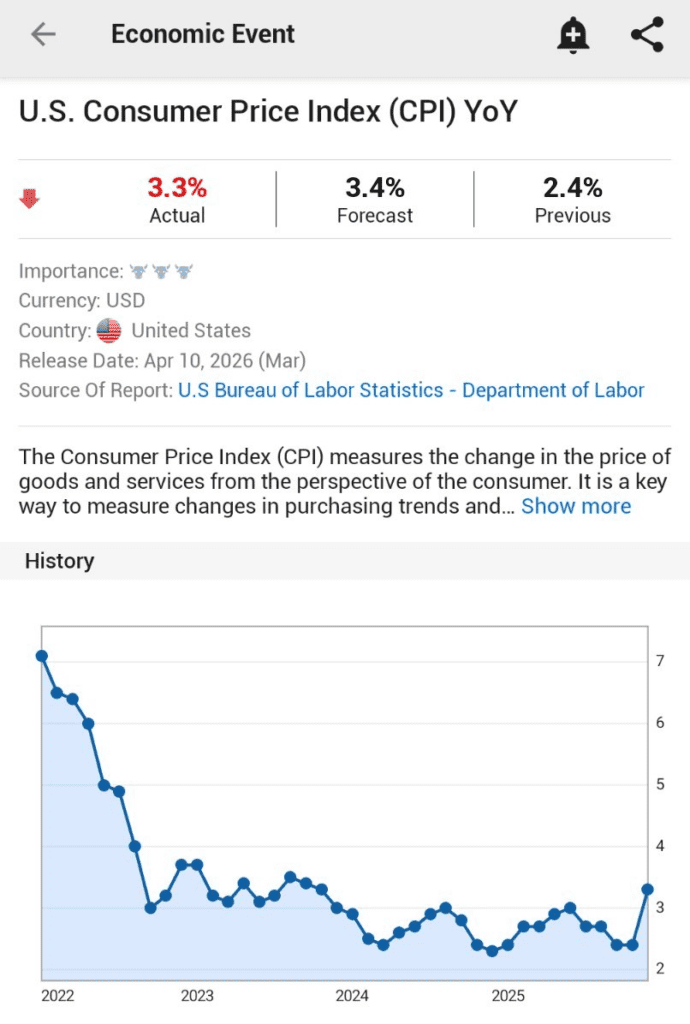

CPI rose because of energy, even if it came in below expectations

The biggest US macro release of the week was March CPI. Headline inflation rose to 3.3%, below expectations of 3.4%, while Core CPI rose to 2.6%, also below expectations of 2.7%.

At the monthly level, CPI jumped 0.9% MoM, with gas up 21.2%, while core inflation held at 0.2%. The jump was clearly tied to the global energy shock created by Middle East tensions.

This was described as the highest inflation level since mid-2024, even though the reading still came in slightly below consensus.

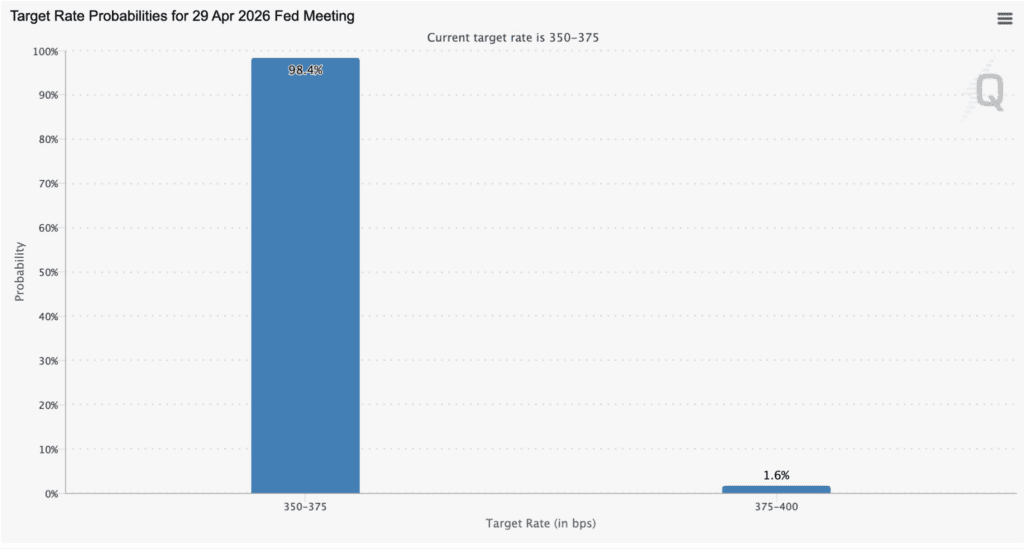

Rate-cut hopes kept fading

The practical market takeaway was not especially dovish. Markets began to rule out an interest-rate cut in 2026, as ongoing inflation pressure and rising oil prices kept the Federal Reserve under pressure.

That fed directly into the growing view that the Fed is likely holding rates. By the end of the week, markets were almost fully pricing no rate change in April. The logic was simple: inflation remained sticky, oil had spiked, and cuts were getting pushed further out. That meant liquidity looked set to remain tighter for now.

Money Supply, Dollar Debasement, and the Bigger Liquidity Picture

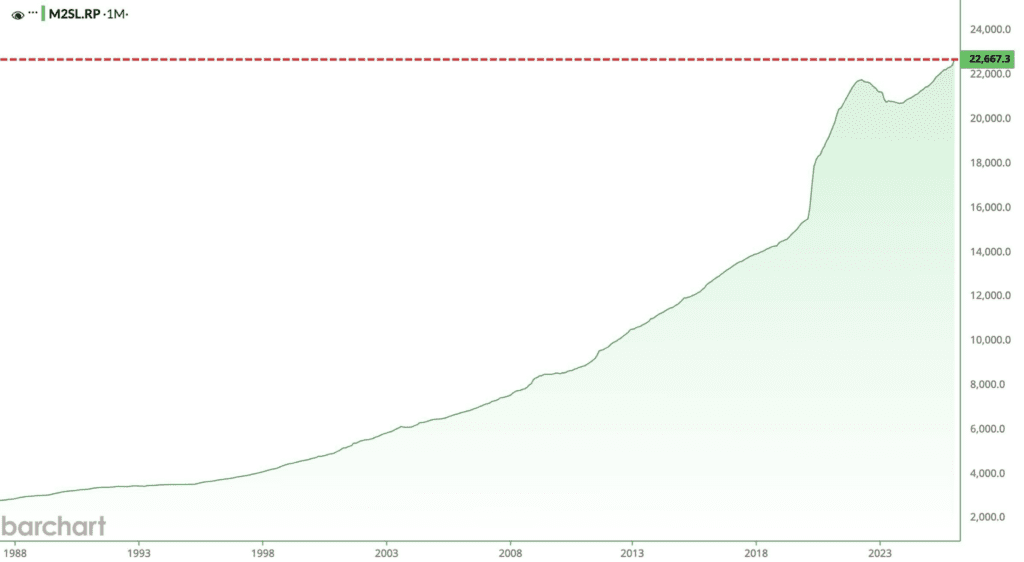

US M2 kept expanding to record highs

One of the most important macro signals this week was the continued rise in US M2 money supply.

February M2 was shown rising 4.8% year over year to a record $22.6 trillion, marking the 24th consecutive monthly increase. Money supply is now about $700 billion above the March 2022 peak. Since the 2020 pandemic, M2 has surged by $7.1 trillion, or roughly $1.2 trillion per year. Since 2000, money in circulation has grown at an average annual rate of 6.2%.

The US dollar is losing purchasing power at a historic pace.

Markets still looked through the noise

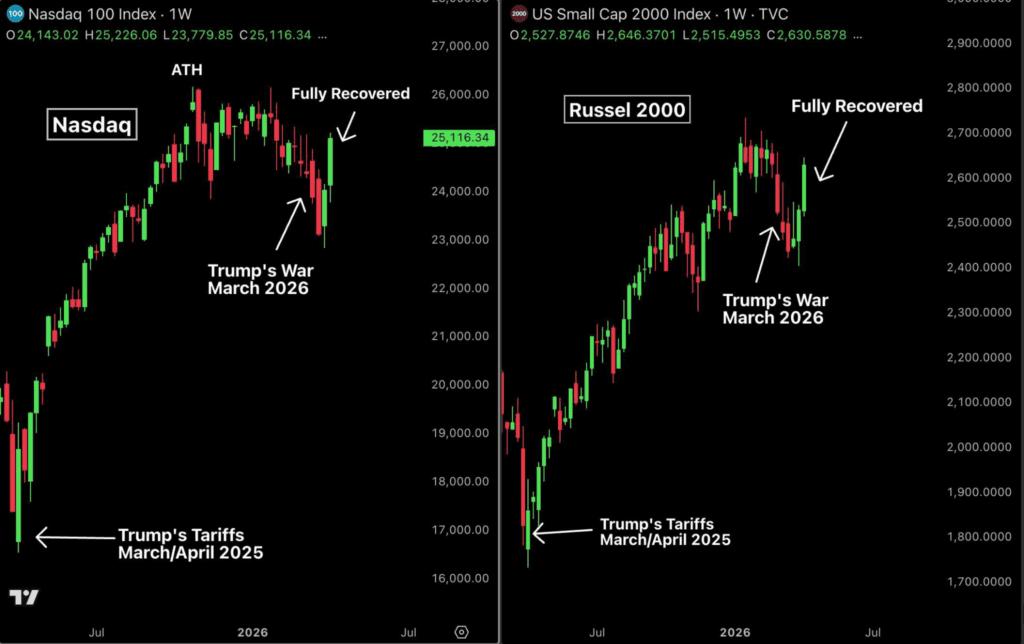

That backdrop helps explain why major US indexes were able to rally even while geopolitical headlines stayed unstable. By late in the week, both the Nasdaq and the Russell 2000 had fully erased all losses caused by the US-Iran war and were both up 9% from the March bottom.

One market view argued that if investors stepped away from the noise, the underlying picture still looked supportive:

- Global M2 supply at an all-time high

- ISM at a 40-month high, staying above 52 for three consecutive months

- Inflation described in that broader framing as near a 60-month low

- A new Fed chair on the way

The conclusion of that view was that if the US-Iran conflict resolves in the coming days or weeks, a stronger market rally could follow.

The Labor Market Looked Weaker Than Headline Moves Suggested

Long-term unemployment kept worsening

Beneath the market recovery, labor data continued to deteriorate. The number of Americans unemployed for more than 15 weeks rose to 3.3 million, the highest since September 2021, and up by 1.6 million since July 2022.

As a percentage of total employment, that measure reached 20.3%, the highest level since October 2021. Historically, going back to the 1950s, every time it has reached these levels, the US economy has effectively entered a recession.

The average duration of unemployment climbed to 25.3 weeks, a level exceeded only during the post-2021 pandemic period and the recovery after the 2008 crisis.

Other signs pointed the same way

The softer labor picture was reinforced by other data. Unemployment benefit claims rose to 219,000. Housing demand was described as declining, while interest rates moved back to around 6.4%.

The market is hanging by a thin thread: stocks closed higher, with the S&P 500 up 0.62% and the Nasdaq up 0.83%, but oil had returned near $98, gold was stable around $4,700, the ceasefire showed signs of cracking, and labor-market weakness remained visible.

Crypto Flows, Liquidity, and Structural Shifts

Spot Bitcoin ETFs kept pulling heavy trading volume

Spot Bitcoin ETFs remained active. Total spot Bitcoin ETF trading volume exceeded $2.4 billion on a particular day.

The issuer breakdown was:

- BlackRock: about $1.93 billion

- Fidelity: about $212.4 million

- Grayscale: about $121.1 million

- Bitwise: about $66 million

- ARK Invest: about $60 million

- Morgan Stanley: about $33.9 million

- VanEck: about $19.7 million

- Invesco: about $7.2 million

- Valkyrie: about $5 million

- Franklin Templeton: about $2.9 million

- WisdomTree: about $1.3 million

- Hashdex: a very small amount relative to the rest, with BlackRock’s dominance described as clear by a wide margin

BlackRock dominated the day’s spot Bitcoin ETF flow.

Hyperliquid became a major venue for oil-perps trading

Another important market-structure detail came from Hyperliquid. Over 24 hours, trading volume in oil perpetual contracts exceeded $4 billion on Hyperliquid.

Within that:

- WTI Oil exceeded $2.6 billion

- Brent Oil reached about $1.4 billion

That was a clear sign that macro volatility was not only hitting traditional markets. It was also driving large derivatives activity inside crypto-native venues.

A suspicious oil trade caught attention

Traders had placed $950 million betting on an oil price drop just hours before the ceasefire announcement. Massive trades in Brent and WTI were executed less than three hours before Trump announced the ceasefire with Iran.

Afterward, oil prices did in fact collapse by about 15%. The timing and size of those positions raised strong questions.

Bitcoin, Ethereum, XRP, and Other Major Crypto Narratives

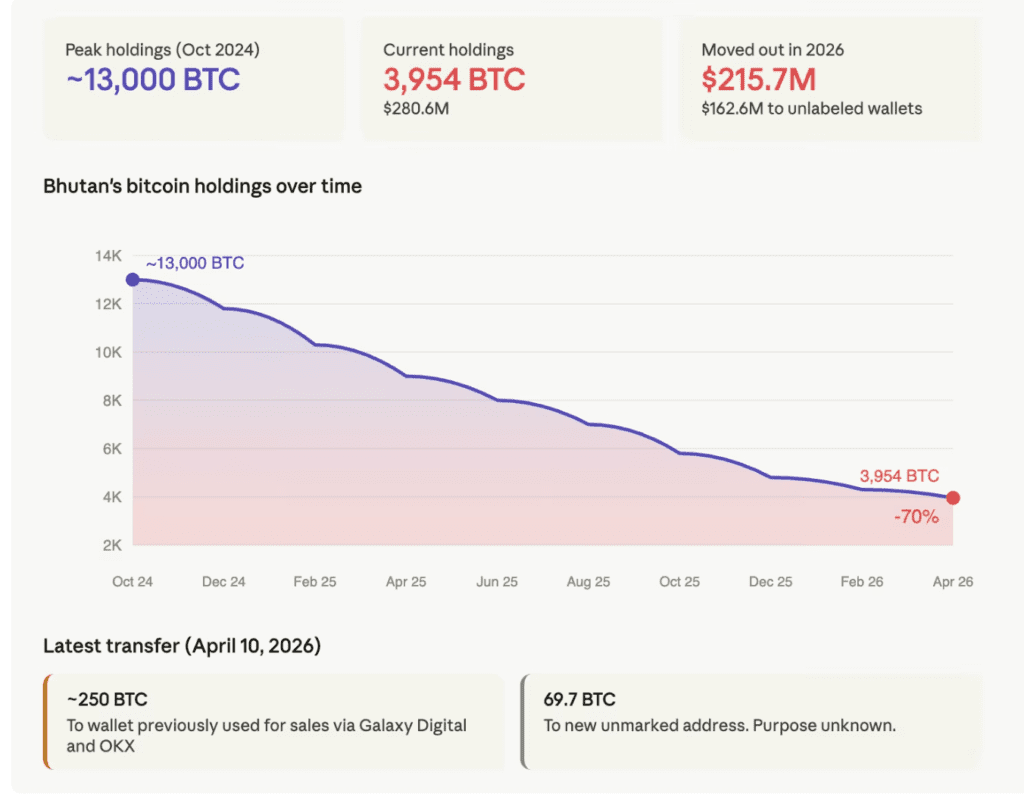

Bhutan and Strategy moved in opposite Bitcoin directions

A major sovereign Bitcoin story came from Bhutan. Over the last 18 months, it has sold 70% of its Bitcoin holdings. According to the data cited, the country’s stash fell from about 13,000 BTC in October 2024 to 3,954 BTC, worth around $280.6 million. This year alone, around $215.7 million in BTC was transferred out.

It has also been more than a year since Bhutan recorded a mining inflow above $100,000, raising the possibility that it may have halted its hydropower-backed Bitcoin mining operations.

Moving in the other direction, Strategy bought another 4,871 BTC worth about $329.9 million, at an average price of $67,718 per Bitcoin. That took total holdings as of April 5, 2026 to 766,970 BTC, acquired at a total cost of around $58.02 billion, with an average purchase price of $75,644.

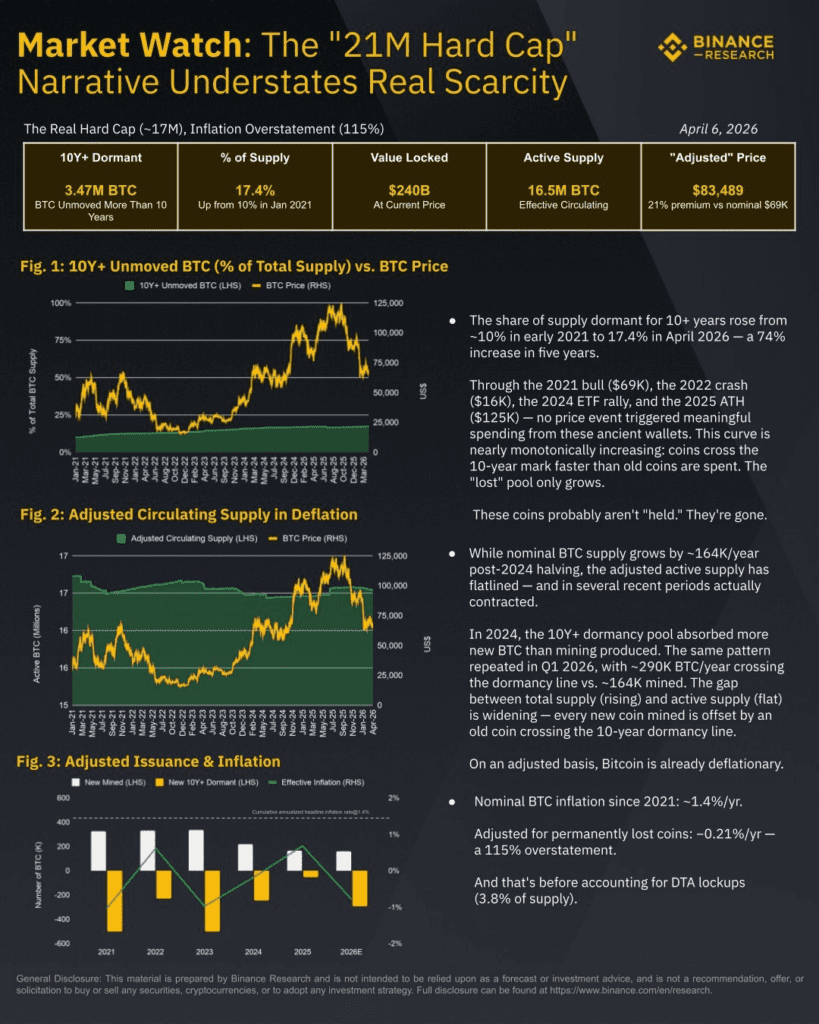

Bitcoin was also framed as deflationary

Bitcoin has already become a deflationary asset, with a net inflation rate of -0.21%.

The reasoning is that roughly 164,000 BTC are issued annually through mining, while about 290,000 BTC become dormant each year, reducing available supply.

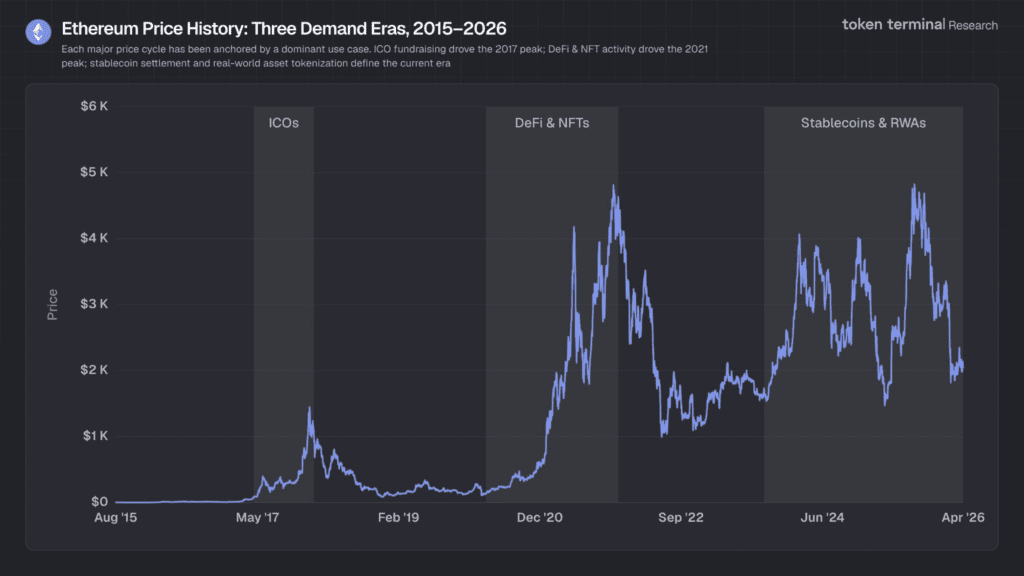

Ethereum’s demand story was described in three eras

One of the cleaner high-level crypto narratives this week focused on Ethereum. The demand story was divided into three periods:

- 2017: the ICO Era

- 2021: the DeFi and NFT Era

- Now: the Stablecoins and Real-World Assets (RWAs) Era

The point was that each cycle built on the one before it, but the current one is the most closely connected to the real economy.

Ripple again targeted SWIFT’s role

Another recurring theme returned through Ripple. The argument was laid out very directly: what Ripple is trying to do is take over SWIFT, replacing a global bank-transfer system that still often takes days with instant settlement at lower cost.

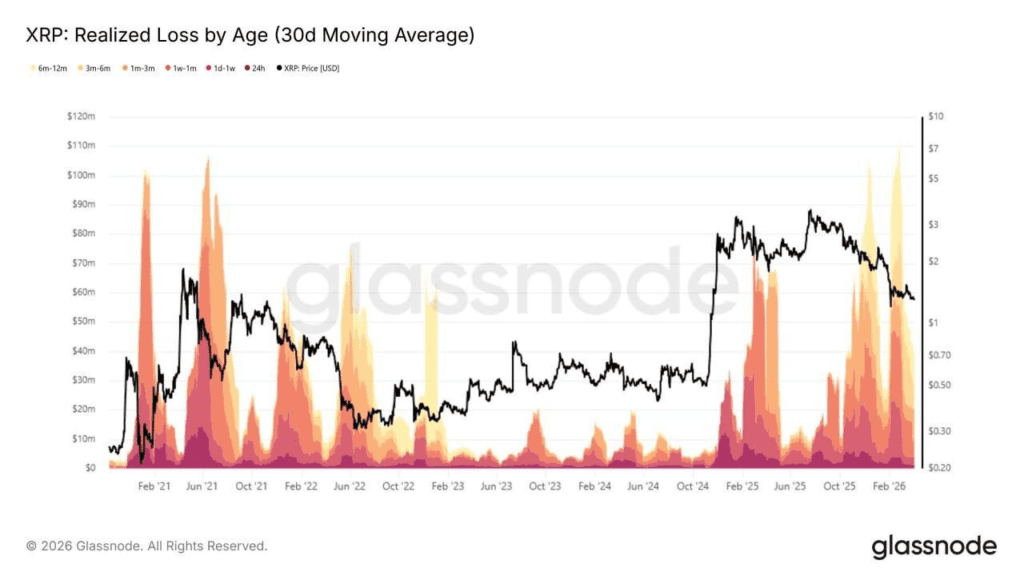

XRP holders stayed under pressure

For XRP, the signal was more negative. Data showed that more than 50% of circulating XRP is currently sitting in unrealized loss territory. That means most investors are holding below their purchase price, which suggests elevated psychological pressure in the market.

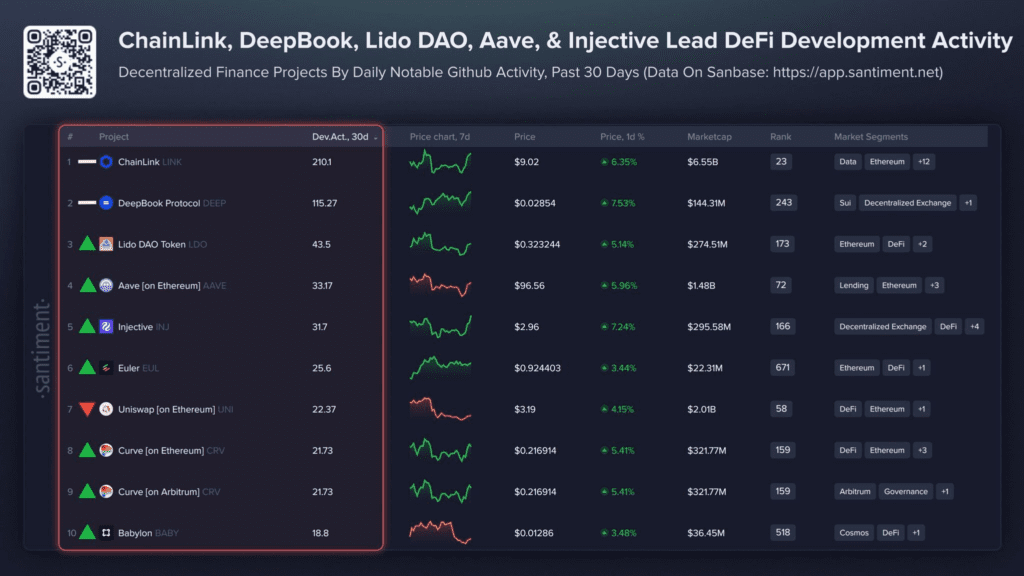

Chainlink led DeFi development activity

Development activity also stayed in focus. Chainlink was shown as the most active DeFi project in terms of development operations, topping the ranking ahead of:

- DeepBook on Sui

- Lido

- Aave

- Injective

This was framed as a sign of infrastructure strength and longer-term sustainability.

Project-Specific Crypto Developments

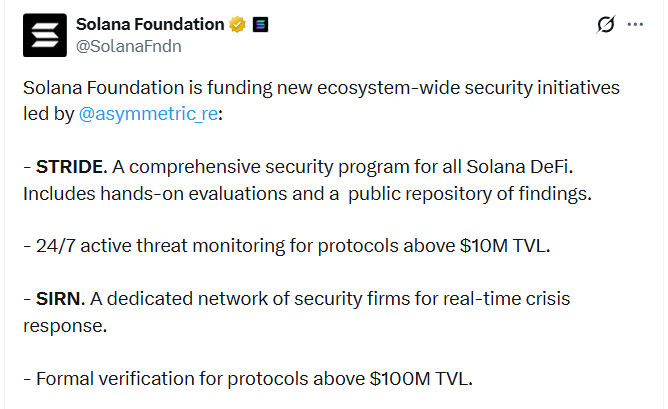

Solana responded to recent security pressure

The Solana Foundation launched new security initiatives with Asymmetric Research, aimed at the entire Solana ecosystem. The most prominent part was the STRIDE initiative, described as a structured program focused on monitoring and evaluating security in Solana projects.

This came after the recent Drift Protocol hack and alongside broader concern around Circle’s compliance failures, including more than $420 million in failures since 2022, 232 million USDC bridged during the Drift hack without being frozen, 3 million USDC in the SwapNet hack, 61 million USDC in the Cetus hack, and 57.5 million USDC linked to the Mango Markets attack.

World Liberty Financial was both expanding and being questioned

World Liberty Financial said it faces no liquidation risks and also pointed to more than $65 million in token buybacks, along with an upcoming governance proposal aimed at early token holders.

But it also faced criticism over a reported move in which 5 billion WLFI tokens were deposited on Dolomite as collateral to borrow $75 million in stablecoins, which were then sent to Coinbase Prime.

That reportedly pushed Dolomite’s USD1 lending pool to 100% utilization, preventing retail depositors from withdrawing funds. Critics said this created a way to extract liquidity without selling the thinly traded token into the market, while also exposing users to default risk if WLFI falls further.

At the same time, Aster DEX announced a strategic partnership with World Liberty Financial to bring RWA markets on-chain, using USD1 as the foundational layer for all RWA assets on the Aster network.

Bittensor was hit by a credibility problem

In Bittensor, Covenant AI, one of the leading developers of Subnets, announced it was leaving the network and called decentralization promises a “lie.” The result was an immediate 15% drop in TAO.

MARA made a move that traders watched closely

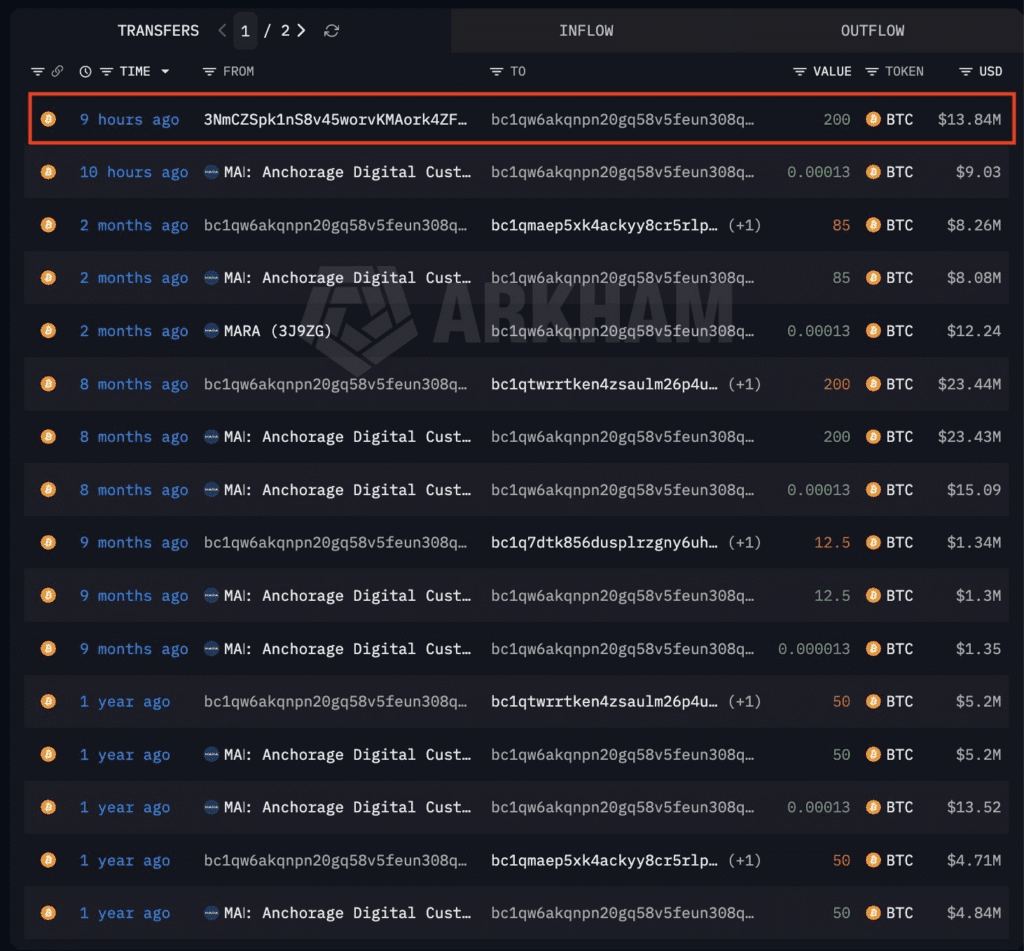

MARA Holdings moved 200 BTC, worth about $13.84 million, to a wallet believed to be linked to sales.

Not to overstate the case, the move could also mean:

- liquidity preparation or a partial sell-off

- internal wallet redistribution

- or routine operational movement

The key point was that a transfer to a sales-linked wallet may be an early signal, but it is not confirmation of an actual sale.

Regulation, Politics, and the Digital Economy

South Korea moved ahead on RWAs and stablecoins

South Korea also stood out for a separate reason this week. The ruling party decided to move forward with regulating tokenized real-world assets and stablecoins within the existing legal framework.

Provisions for digital assets linked to RWAs were included in the draft Basic Act on Digital Assets, pointing to a more integrated national digital-economy framework.

Telegram warned about censorship in Europe

Telegram founder Pavel Durov warned of rising censorship in Europe. He said European Union authorities were using concerns around private groups as a pretext for greater censorship and surveillance.

He linked that warning to initiatives such as Chat Control and the Digital Services Act, arguing that they could lead to stronger restrictions on privacy and a wider expansion of oversight over digital communications.

US politics added to the noise

In Washington, three US senators reportedly began investigating whether Donald Trump suggested that buying the $TRUMP meme coin could help secure access to him at a dinner event.

That added another layer to the overlap between politics, influence, and token speculation.

Traditional Finance and Broader Market Signals

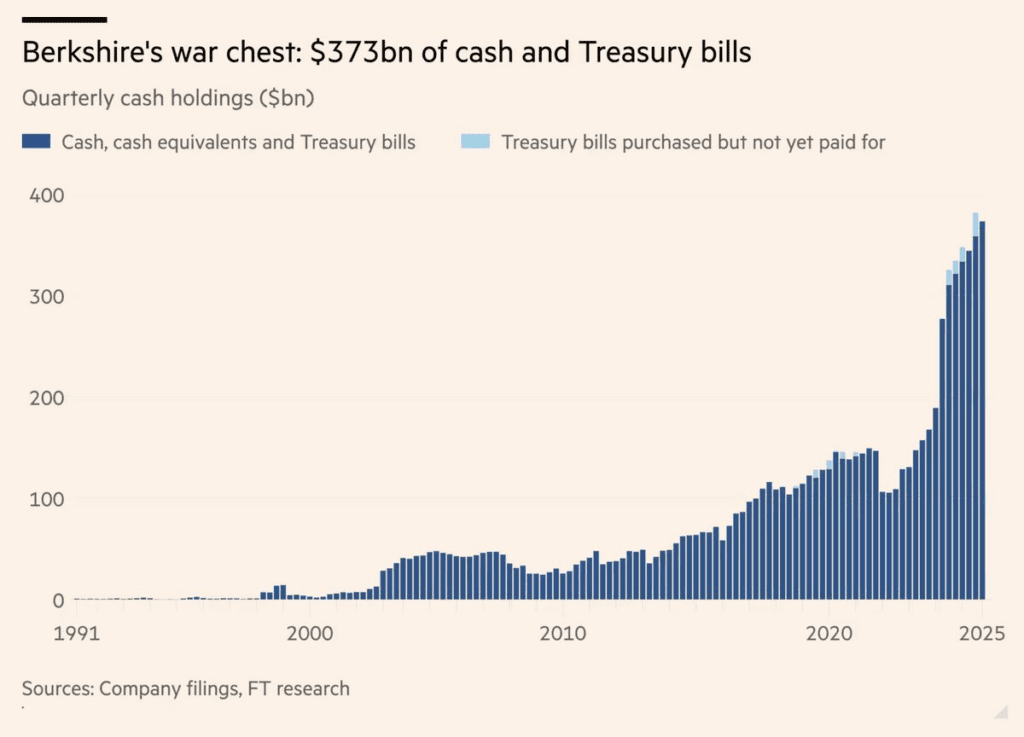

Buffett’s cash pile remained a warning sign

Berkshire Hathaway was said to be holding roughly $373 billion in cash, an extraordinary level that would theoretically be enough to buy around 480 companies in the S&P 500.

The interpretation was that Warren Buffett remains extremely cautious on current valuations, is waiting for better opportunities, and is holding liquidity in case of a larger market correction.

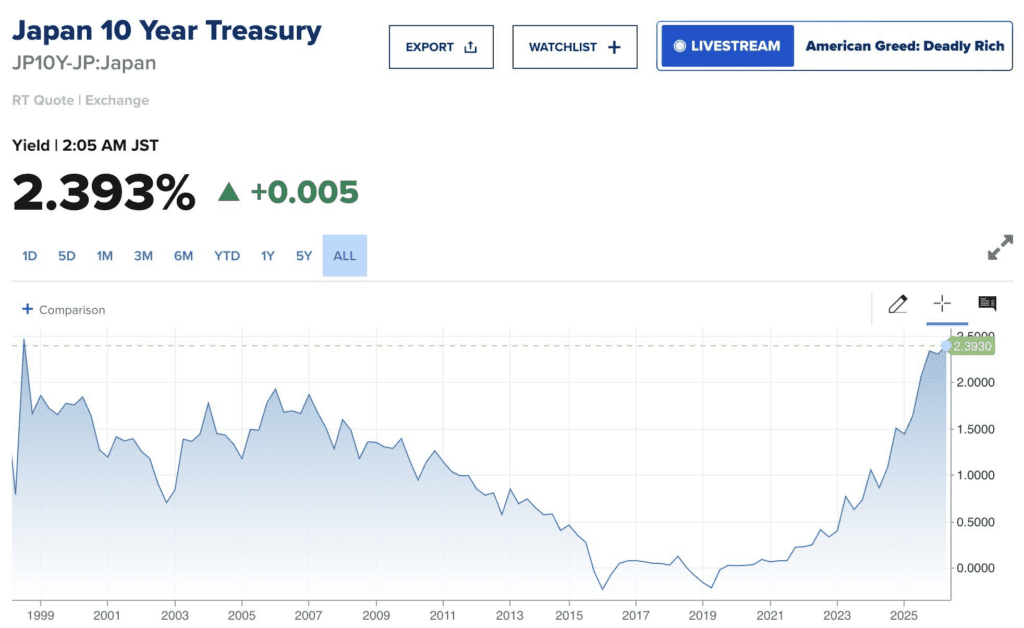

Japan became a new source of global stress

Another major macro story came from Japan. The 10-year Japanese government bond yield rose to 2.39%, its highest level in decades.

The argument attached to that move was that inflation is finally taking hold in Japan, forcing the Bank of Japan to abandon yield curve control. The global consequences described were serious:

- tighter global liquidity as Japan exits quantitative easing

- greater risk of Japanese capital repatriation

- more pressure on US Treasuries, stocks, and crypto

The point was simple: Japan was not on many radar screens, but it had become a real macro risk.

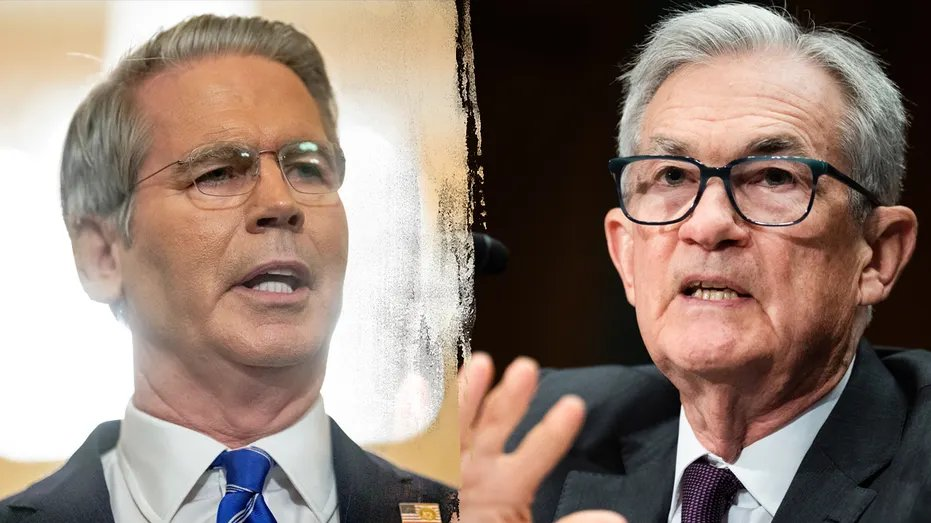

Wall Street was also forced to think about AI risk

Late in the week, the Treasury Secretary and Federal Reserve Chair Jerome Powell called Wall Street leaders into an urgent meeting over concern that a new Anthropic AI model could create higher cybersecurity risks.

This was a sign that AI is now being treated not only as a growth driver, but also as a possible source of financial-system vulnerability.

Jamie Dimon made the broader geopolitical case plainly

One of the week’s cleanest macro statements came from Jamie Dimon, who said it was far more important that the Iran conflict ends successfully than what markets do in the short term.

His message was that securing global energy flows and resolving deeper geopolitical threats matters more than short-term price action, and that markets may remain volatile until the crisis is truly resolved.

Final Take

This week was not just about one theme. It was about the overlap between war risk, inflation, weak labor data, liquidity expansion, and changing crypto structure.

The Strait of Hormuz stayed unstable even under a ceasefire. Inflation rose because of energy. Markets pushed rate cuts further out. US money supply kept climbing. Long-term unemployment worsened. Yet stocks recovered, Bitcoin ETFs remained active, Strategy kept buying BTC, and crypto liquidity concentrated even more around the biggest platforms.

At the same time, the week brought major project-level developments across Ethereum, Ripple, XRP, Solana, World Liberty Financial, Bittensor, Chainlink, Hyperliquid, and Telegram.

The broad lesson is clear: headline calm and structural calm are not the same thing. Markets may have recovered, but the deeper stresses behind them, geopolitical risk, inflation pressure, labor-market weakness, liquidity concentration, and regulatory tension, are still very much alive.

This article is for general information only and should not be considered financial advice. Markets can react quickly to geopolitical headlines, inflation data, and crypto-specific developments. Read our blog for more market coverage, and if you choose to act, trade responsibly on Millionero.